The modern actuary stands at the fascinating intersection of advanced mathematics, statistical science, economics, and cutting-edge technology. Far from the stereotype of a numbers cruncher confined to a spreadsheet, today’s actuaries are dynamic professionals who leverage sophisticated analytical tools and innovative methodologies to measure, manage, and mitigate financial risks. Their work is fundamentally about forecasting the future consequences of financial decisions, particularly in industries where uncertainty is a core component, such as insurance, pensions, and investments. In essence, an actuary translates complex data into actionable insights, helping organizations navigate uncertainty and make sound financial choices that protect against unforeseen events.

The Core of Actuarial Science: Bridging Risk and Data

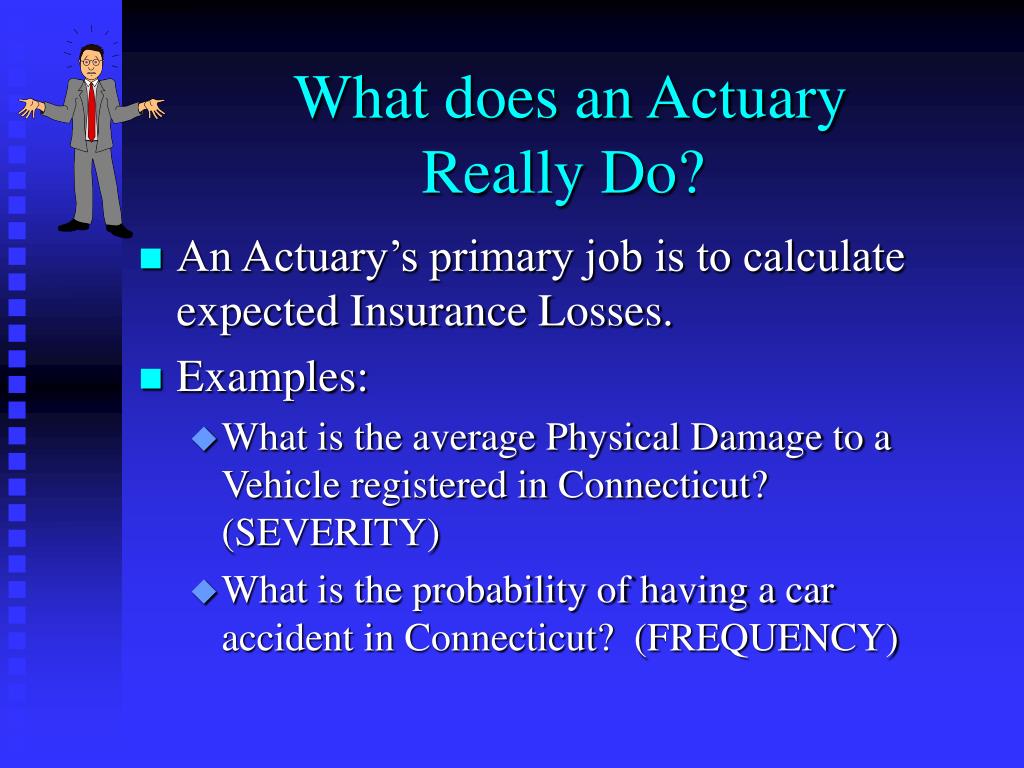

At its heart, actuarial science is the discipline of applying mathematical and statistical methods to assess risk in financial and insurance industries. This involves deep dives into vast datasets, identifying patterns, and constructing models that predict future events and their financial implications. The role requires a unique blend of analytical rigor and practical application, transforming raw data into strategic foresight.

Statistical Modeling and Predictive Analytics

Actuaries are masters of statistical modeling. They design and implement complex models to quantify the probability of various events, such as mortality rates, accident frequency, natural disasters, or investment performance fluctuations. These models are not static; they are continuously refined and validated against new data, incorporating advanced statistical techniques like regression analysis, time series analysis, and stochastic modeling. Predictive analytics is a cornerstone of this work, enabling actuaries to move beyond historical trends and anticipate future outcomes with a higher degree of precision. For instance, in life insurance, actuaries model human lifespans to determine appropriate premium rates and reserve levels. In property and casualty insurance, they predict the likelihood and severity of claims from events ranging from car accidents to catastrophic storms. The precision and robustness of these models directly impact the financial stability and competitiveness of the organizations they serve, underscoring the critical innovative thinking required to constantly improve these predictive capabilities.

The Role of Data Science

The explosion of big data has profoundly reshaped the actuarial profession, elevating the importance of data science skills. Actuaries now routinely work with massive, disparate datasets, extracting meaningful insights that were previously unattainable. This involves advanced data mining techniques, machine learning algorithms, and artificial intelligence to identify subtle correlations and drivers of risk. For example, actuaries might use machine learning to detect fraud patterns in insurance claims or to personalize risk assessments for individual policyholders based on a multitude of behavioral and demographic factors. They are responsible not only for building these data-driven models but also for ensuring their ethical use, understanding their limitations, and communicating their complex outputs clearly to non-technical stakeholders. The ability to clean, transform, analyze, and interpret large volumes of data is now as crucial as traditional mathematical aptitude, placing actuaries firmly within the realm of data-driven innovation.

Leveraging Technology for Future Insights

The actuarial toolkit is increasingly digital and dynamic. Actuaries are early adopters of new computational methods and software, always seeking to enhance the accuracy, efficiency, and scope of their analyses. This technological embrace is essential for managing the growing complexity of financial products and regulatory environments.

Advanced Software and Programming Languages

Modern actuaries are proficient in a variety of powerful software platforms and programming languages. Beyond advanced spreadsheet applications, they regularly utilize statistical software packages like R and Python, which offer extensive libraries for data manipulation, statistical analysis, and machine learning. Database management systems, actuarial specific software (e.g., for reserving, pricing, or capital modeling), and visualization tools are also integral to their daily operations. The ability to code allows actuaries to build custom models, automate repetitive tasks, and process vast amounts of data more efficiently than ever before. This proficiency transforms them from mere users of technology into creators of bespoke analytical solutions, driving innovation within their respective fields. They often develop sophisticated simulations, stress tests, and scenario analyses that would be impossible without these technological capabilities, pushing the boundaries of traditional risk assessment.

Automation and Efficiency in Actuarial Processes

Technological advancements have also enabled significant automation in actuarial workflows. Repetitive data collection, reconciliation, and report generation tasks are increasingly automated, freeing actuaries to focus on higher-value activities like model development, strategic analysis, and communicating insights. Robotic Process Automation (RPA) and other automation tools are being integrated to streamline compliance reporting, premium calculations, and claims processing. This push for efficiency not only reduces operational costs but also improves the accuracy and speed of actuarial output, allowing businesses to respond more rapidly to market changes and regulatory demands. The actuary’s role evolves from manual calculation to designing and overseeing automated systems, requiring a strong understanding of information systems and process optimization, a clear example of embracing innovation to enhance productivity and precision.

Innovation in Risk Management and Financial Forecasting

The landscape of risk is constantly evolving, driven by global connectivity, technological disruption, and shifting environmental and societal factors. Actuaries are at the forefront of identifying and quantifying these new risks, developing novel approaches to manage them effectively.

Adapting to Emerging Risks and Market Dynamics

From cyber risk and climate change to pandemics and geopolitical instability, actuaries are continually challenged to develop innovative frameworks for assessing previously unquantified exposures. This requires creative problem-solving and the ability to extrapolate from limited data, often combining qualitative judgments with quantitative models. They collaborate with subject matter experts across various disciplines to build holistic risk assessments. For example, actuaries are instrumental in designing new insurance products to cover cyber-attacks or developing climate-risk models that project the financial impact of rising sea levels or extreme weather events on property portfolios. Their ability to innovate in the face of unprecedented challenges is vital for ensuring the long-term resilience of financial institutions and the broader economy. This proactive approach to identifying and mitigating future risks is a hallmark of actuarial innovation.

Development of New Actuarial Methodologies

The profession isn’t just applying existing methods; it’s actively developing new ones. Actuaries contribute to academic research, publish papers, and participate in professional bodies that set industry standards and push methodological boundaries. This includes the development of more granular pricing models, advanced reserving techniques under new accounting standards (e.g., IFRS 17), and sophisticated enterprise risk management (ERM) frameworks that integrate financial, operational, and strategic risks across an entire organization. They are also exploring the application of non-traditional data sources and advanced analytical techniques from fields like behavioral economics to enhance their predictive power. This constant pursuit of better, more accurate, and more comprehensive methodologies is a testament to the innovative spirit embedded within actuarial science.

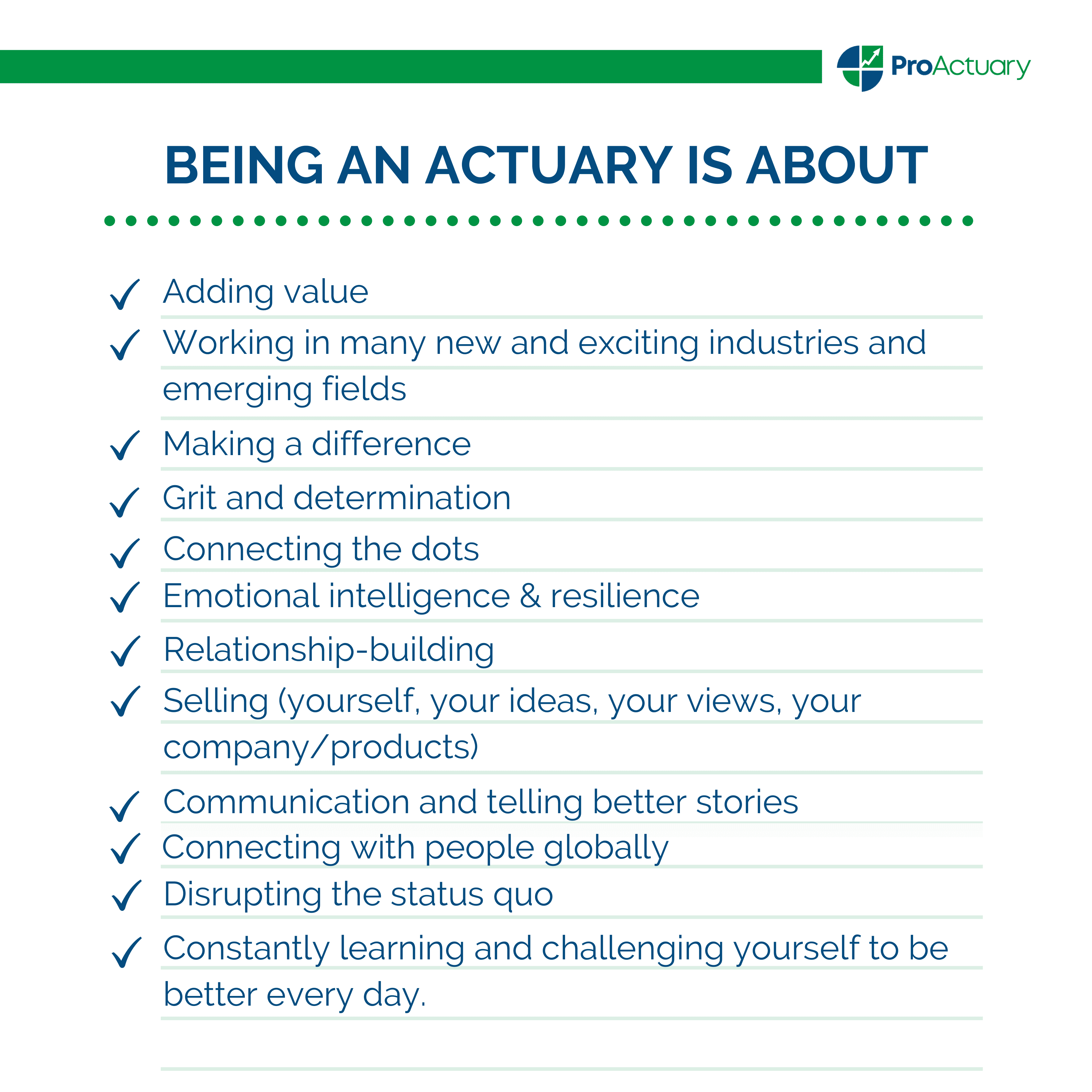

The Actuary as a Strategic Innovator

Beyond the technical analysis, actuaries serve as crucial strategic advisors. Their unique blend of analytical rigor and business acumen positions them to translate complex statistical findings into clear, actionable business strategies. They don’t just present numbers; they articulate the strategic implications of those numbers.

Communicating Complex Data and Insights

A key part of an actuary’s innovative contribution is their ability to communicate highly technical concepts and the implications of complex models to a diverse audience, including executives, regulators, and sales teams. This requires strong presentation skills, the ability to create compelling data visualizations, and a deep understanding of the business context. Actuaries act as translators, bridging the gap between intricate quantitative analysis and practical business decisions. They explain risk exposures, model assumptions, and recommended strategies in a way that empowers stakeholders to make informed choices, fostering a culture of data-driven innovation throughout the organization. Their capacity to simplify the complex ensures that technological and analytical advancements are effectively integrated into an organization’s strategic thinking and execution.