The Technological Backbone of Global Finance: Understanding SWIFT and BIC

In an increasingly interconnected global economy, the seamless and secure transfer of funds across international borders is paramount. At the heart of this intricate system lies the SWIFT/BIC code, a critical piece of technological infrastructure that facilitates billions of transactions daily. Far from being a mere alphanumeric string, the SWIFT/BIC code represents a sophisticated standard that underpins the reliability, speed, and security of global financial communications, serving as an indispensable component of modern financial technology and innovation. It is the standardized identifier for financial institutions worldwide, ensuring that international payments reach their intended recipients without ambiguity.

Origins and Evolution of a Standardized System

Before the advent of SWIFT, international wire transfers were a cumbersome, error-prone, and slow process. Banks relied on a patchwork of proprietary telex messages, bilateral agreements, and manual reconciliation, leading to delays, increased costs, and frequent mistakes. This inefficiency highlighted a pressing need for a universal, standardized system capable of streamlining cross-border financial communication.

The Society for Worldwide Interbank Financial Telecommunication (SWIFT) was established in 1973 by a consortium of 239 banks from 15 countries. Its primary objective was to replace the fragmented communication methods with a shared, standardized data processing system and a worldwide communication network. The innovation lay in creating a common language and a secure platform for financial messages, moving beyond the proprietary systems that hindered global commerce. Initially focused on interbank messaging, SWIFT quickly expanded its services, becoming the standard for virtually all international financial transactions. Its evolution reflects a continuous drive towards greater efficiency, security, and global reach, adapting its technological framework to meet the escalating demands of international trade and finance.

The SWIFT Network: A Secure Messaging Platform

The SWIFT network itself is not a system that holds or transfers funds; rather, it is a highly secure and reliable messaging system that transmits instructions for transfers between financial institutions. Think of it as a sophisticated, private global email system exclusively for financial transactions, meticulously designed to ensure the integrity and confidentiality of sensitive financial data. When a bank initiates an international transfer, it sends a standardized message (e.g., an MT 103 for customer payments) over the SWIFT network to the recipient bank. This message contains all the necessary details for the transfer, including the amount, currencies, beneficiary information, and critically, the BIC codes of both the sending and receiving institutions.

The technological ingenuity of SWIFT lies in its standardized message formats, known as SWIFT messages. These formats ensure that all participating financial institutions understand the information conveyed, regardless of their internal systems or geographical location. This standardization drastically reduces errors and processing times, enabling automated processing (straight-through processing or STP) for a significant portion of international payments. The network operates 24/7, offering high availability and robust security protocols, including encryption, authentication, and continuous monitoring, to protect against cyber threats and unauthorized access. This secure messaging architecture is a cornerstone of global financial stability, providing a trusted environment for trillions of dollars in transactions annually.

Deconstructing the BIC: Structure and Significance

The BIC (Bank Identifier Code), often interchangeably referred to as the SWIFT code, is the globally recognized identifier for financial and non-financial institutions on the SWIFT network. It is a unique address that pinpoints a specific bank or branch, much like an IP address identifies a specific computer on a network. Its precise structure and mandatory usage are central to the operational efficiency and accuracy of international money transfers, making it a critical piece of data technology. Without this standardized identification system, the complexity and potential for error in cross-border payments would be overwhelmingly high, underscoring its role as a fundamental innovation in global banking.

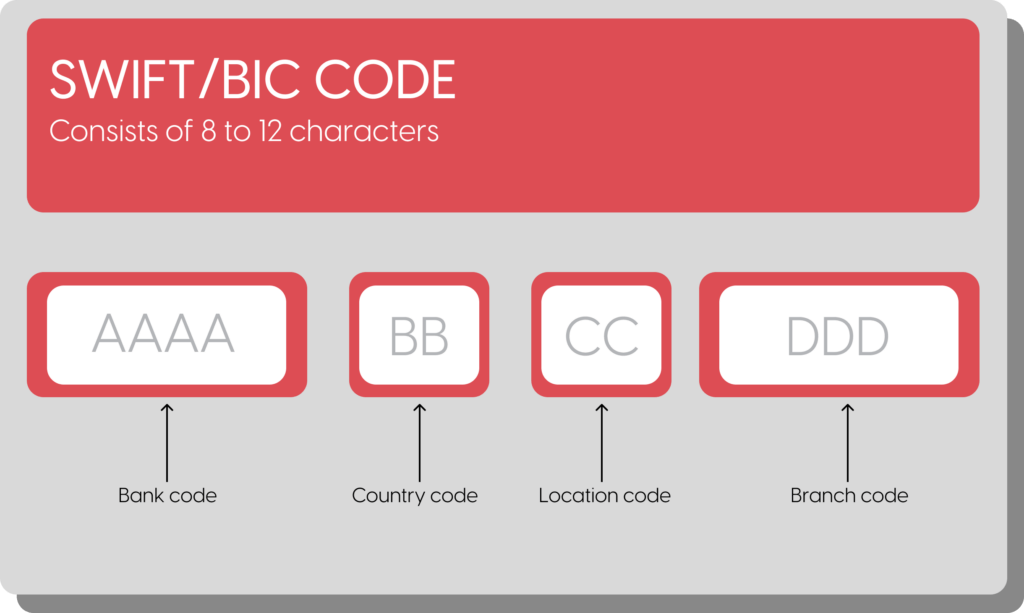

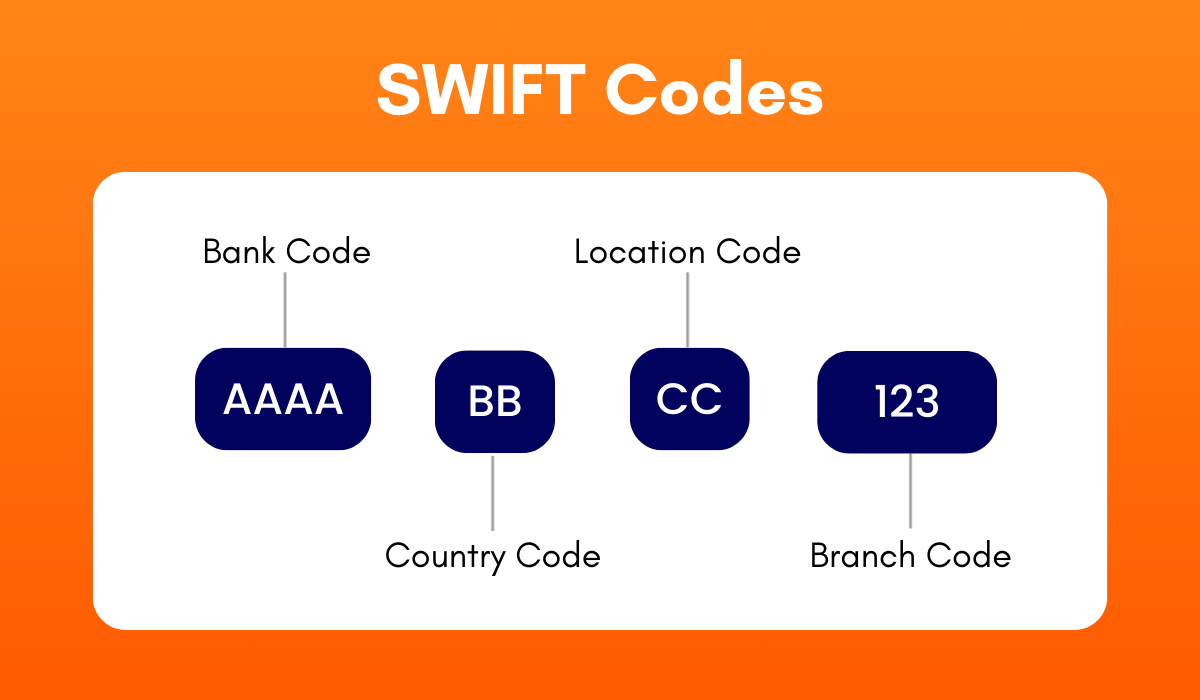

Decoding the BIC Format: Bank, Country, Location, Branch

A BIC typically consists of 8 or 11 characters, following a rigidly defined alphanumeric structure. Each segment of the code conveys specific information, allowing for precise identification:

- Bank Code (A-Z, 4 characters): This segment identifies the financial institution uniquely. For example, “CHAS” might represent JP Morgan Chase, or “DEUT” for Deutsche Bank. This code is often an abbreviated version of the bank’s name, making it somewhat intuitive yet globally unique.

- Country Code (A-Z, 2 characters): This follows the ISO 3166-1 alpha-2 standard, indicating the country where the bank is located. For instance, “US” for the United States, “GB” for Great Britain, or “DE” for Germany. This ensures geographical clarity, essential for routing international transactions.

- Location Code (0-9, A-Z, 2 characters): This part specifies the city or geographical location of the bank’s head office or a particular branch. These characters can be alphanumeric, adding another layer of specificity. A common pattern is for “0” to indicate a test BIC, and “1” to indicate a passive participant in the network.

- Branch Code (0-9, A-Z, 3 characters, optional): This three-character segment is optional. If an 8-character BIC is used, it typically refers to the primary or head office of the bank. When an 11-character BIC is provided, this segment precisely identifies a specific branch within the bank. For example, “XXX” often denotes the primary office when a branch code isn’t explicitly needed for the transaction, or a specific branch code like “LPN” could indicate a London branch.

This structured format is a testament to the meticulous design required for a global financial messaging system. It allows for automated validation and routing, significantly reducing the manual intervention and potential for human error that characterized older systems. The precision afforded by the BIC is a prime example of how robust data standards drive technological innovation in complex environments.

Beyond Identification: Ensuring Transactional Integrity

The significance of the BIC extends beyond mere identification. It plays a crucial role in ensuring transactional integrity, a concept vital for maintaining trust and stability in global finance. By uniquely identifying the involved financial institutions, the BIC helps prevent misdirection of funds, reduces the risk of fraud, and supports regulatory compliance efforts.

When an international payment is initiated, the correctness of the BIC is as critical as the account number itself. An incorrect BIC can lead to significant delays, the payment being returned to the sender, or in rare cases, funds being sent to an unintended recipient (though modern banking systems have multiple layers of verification). The integrity it provides allows for straight-through processing (STP), where payments are processed automatically without manual intervention, saving time and resources for both banks and their customers. Furthermore, the BIC is integral to anti-money laundering (AML) and counter-terrorist financing (CTF) efforts, as it helps regulators and financial institutions track the flow of funds and identify suspicious activities across the global network. This dual function—enabling efficiency and bolstering security—highlights the BIC’s sophisticated role as a foundational piece of financial technology.

Driving Efficiency and Innovation in Cross-Border Payments

The technological underpinnings of SWIFT and BIC codes have been instrumental in revolutionizing the efficiency and reliability of cross-border payments. What was once a slow, costly, and opaque process has been transformed into a relatively swift, transparent, and secure mechanism, thanks to the continuous innovation and standardization driven by the SWIFT ecosystem. This evolution showcases how fundamental tech infrastructure can drive significant economic impact and foster further advancements in financial services.

Automating International Transfers

One of the most profound impacts of SWIFT and BIC has been the enablement of extensive automation in international money transfers. Before their widespread adoption, the complexities of different banking systems, currencies, and regulatory environments necessitated extensive manual checks and interventions. The standardized message formats and unique identifiers introduced by SWIFT allowed for the development of sophisticated automated systems capable of processing payments with minimal human involvement.

This “straight-through processing” (STP) has dramatically reduced the time taken for international transactions, often from days to hours, and in some cases, minutes. Automation also significantly lowers operational costs for banks, as fewer human resources are required to manage and verify transactions. For businesses and individuals, this translates into faster access to funds, improved cash flow management, and greater predictability in international commerce. The underlying technology that supports this automation includes advanced routing algorithms, real-time message validation, and robust data integration capabilities, making the SWIFT network a high-tech data conduit. This continuous drive for automation remains a key area of innovation within the financial technology sector, with SWIFT constantly exploring enhancements to its platform and services.

Role in Financial Security and Compliance

Beyond efficiency, SWIFT and BIC codes play an indispensable role in upholding financial security and compliance standards globally. The network’s design incorporates rigorous security measures, making it one of the most resilient and secure financial messaging systems in the world. End-to-end encryption, multi-factor authentication, and sophisticated fraud detection systems are continuously updated to counteract evolving cyber threats.

Furthermore, the standardized nature of SWIFT messages and the clear identification provided by BIC codes are critical for meeting global regulatory requirements, particularly those related to Anti-Money Laundering (AML) and Counter-Terrorist Financing (CTF). Financial institutions are mandated to conduct due diligence on their customers and monitor transactions for suspicious activities. The structured data within SWIFT messages, including sender, recipient, amount, and purpose of payment, provides the necessary audit trail for compliance officers and regulatory bodies to trace funds effectively. This technological framework not only facilitates legitimate trade but also acts as a powerful deterrent against illicit financial activities, reinforcing global financial integrity. The commitment to maintaining a secure and compliant network is a cornerstone of SWIFT’s innovation strategy, ensuring the trust and confidence of its vast network of users.

The Future Landscape: Adaptations and Emerging Technologies

The financial technology landscape is in constant flux, driven by rapid advancements in digital capabilities and evolving customer expectations. While SWIFT and BIC codes have been foundational for decades, the system is not static. It is continually adapting and integrating new technologies to remain at the forefront of global payment innovation, demonstrating a proactive approach to maintain its relevance in a highly competitive and dynamic sector. This forward-looking approach ensures that the established infrastructure can interface with, and benefit from, emerging digital solutions.

API Integration and Enhanced User Experience

One significant area of innovation for SWIFT is the increasing adoption of Application Programming Interfaces (APIs). Traditionally, interacting with the SWIFT network involved complex, proprietary interfaces and specialized software. However, the modern digital economy demands more flexible, real-time connectivity. SWIFT’s initiatives like SWIFT gpi (global payment innovation) have already brought significant improvements in speed, transparency, and traceability of cross-border payments. Building on this, the development of SWIFT APIs allows financial institutions and even corporate treasuries to integrate SWIFT capabilities directly into their own applications and workflows.

This API-driven approach facilitates greater automation, enables real-time payment tracking, and offers a more seamless and intuitive user experience. For instance, a corporate client could potentially initiate and track international payments directly from their enterprise resource planning (ERP) system, receiving instant updates on payment status. This reduces reliance on manual processes, minimizes errors, and empowers users with greater control and visibility over their international transactions. The shift towards API-based connectivity is a clear indicator of SWIFT’s commitment to modernizing its offerings and fostering an open, integrated financial ecosystem that leverages contemporary software development paradigms.

Complementary Technologies and the Path Forward

While blockchain and distributed ledger technologies (DLTs) have garnered significant attention as potential disruptors in cross-border payments, SWIFT views these as complementary rather than outright replacements. SWIFT has actively explored how DLTs can enhance its existing services, for example, through proof-of-concept projects aimed at improving reconciliation processes and optimizing liquidity management. The strategic focus is on leveraging the strengths of new technologies to build upon the robust, established infrastructure of SWIFT, rather than starting from scratch.

Furthermore, SWIFT continues to invest in technologies like Artificial Intelligence (AI) and machine learning (ML) to enhance its security protocols, improve fraud detection capabilities, and optimize network performance. These technologies can analyze vast amounts of transaction data to identify anomalies and potential threats with greater accuracy and speed than traditional methods. The path forward for SWIFT involves a continuous cycle of innovation—standardizing new payment messages for emerging payment types, enhancing cybersecurity measures, and integrating with the broader fintech ecosystem through open standards and collaborative initiatives. The enduring relevance of SWIFT and BIC codes lies in their adaptability and their role as a critical, evolving component of the global financial technology landscape, continually innovating to meet the demands of a fast-paced, digitally driven world.