Unpacking Canada’s Harmonized Sales Tax

The Harmonized Sales Tax (HST) represents a pivotal component of Canada’s taxation landscape, a system designed to streamline the collection of consumption taxes in several provinces. Far from a simple sales tax, HST combines federal and provincial levies into a single, unified framework. Understanding HST is crucial for businesses operating within Canada, consumers making purchases, and anyone engaging with the Canadian economy, as it impacts everything from daily necessities to large-scale investments. Its implementation marked a significant shift in fiscal policy, aiming to reduce administrative burdens for businesses while ensuring a consistent tax application across participating jurisdictions.

The Genesis and Evolution of HST

Before the introduction of HST, Canada operated with a dual system: the federal Goods and Services Tax (GST) and individual provincial sales taxes (PST), which varied significantly from province to province. This created complexities for inter-provincial trade and compliance, as businesses had to navigate different rules, rates, and reporting mechanisms. The concept of harmonizing these taxes emerged as a solution to these inefficiencies. The goal was to create a more integrated and transparent consumption tax system, fostering economic growth by simplifying the tax structure for businesses and encouraging investment. The transition to HST wasn’t uniform across the country, nor was it without its initial challenges and public discourse regarding its impact on consumer prices.

Provinces Adopting the HST Model

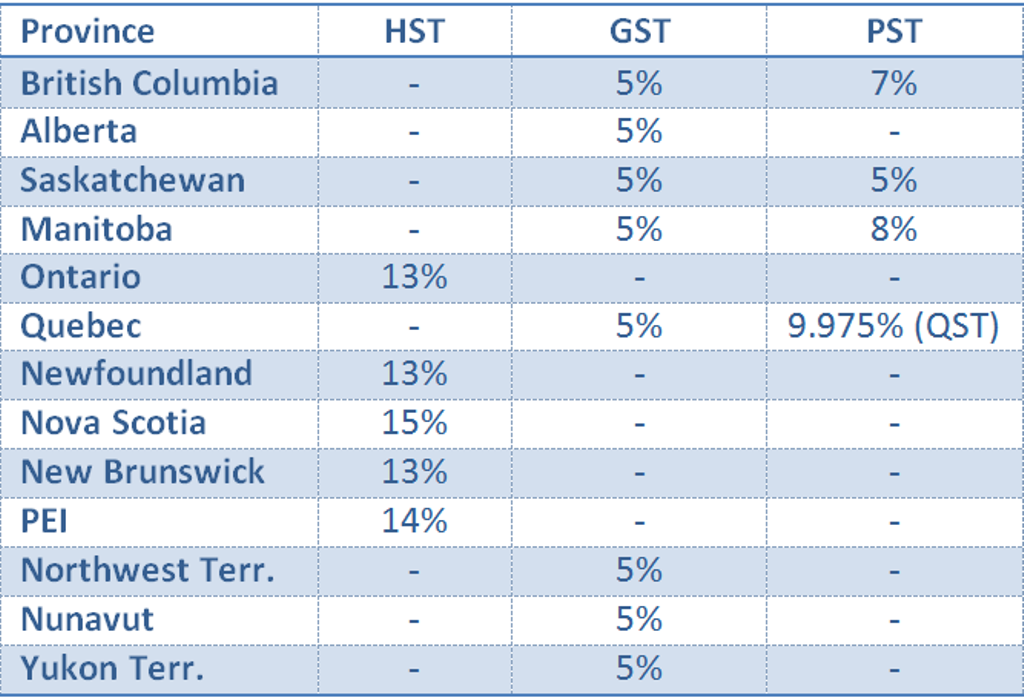

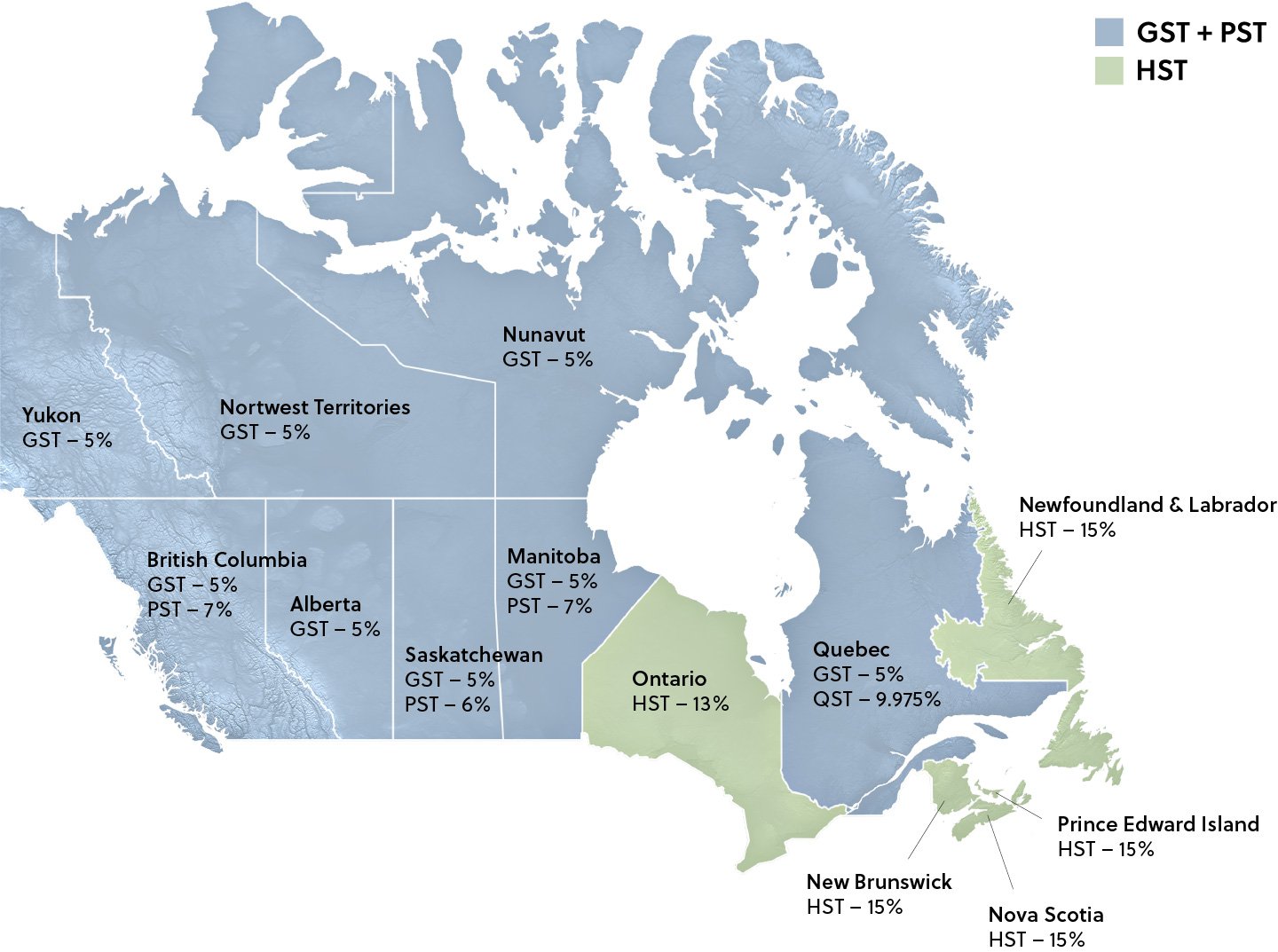

Currently, five Canadian provinces operate under the HST system:

- Ontario: Adopted HST in 2010.

- New Brunswick: One of the original HST provinces since 1997.

- Newfoundland and Labrador: Also an original HST province since 1997.

- Nova Scotia: Another original HST province since 1997.

- Prince Edward Island (PEI): Joined the HST framework in 2013.

In these provinces, businesses collect a single, combined tax at the point of sale. Other provinces and territories continue to use either only the federal GST (like Alberta, Yukon, Northwest Territories, and Nunavut) or a combination of GST and their own provincial sales tax (like British Columbia, Saskatchewan, and Manitoba). This regional variation necessitates a clear understanding of where and how HST applies. The specific HST rate also varies by province, reflecting the combined federal and provincial rates.

How HST Operates: A Blended Consumption Tax

At its core, HST is an ad valorem tax, meaning it’s levied as a percentage of the value of goods and services. It is collected by businesses registered for GST/HST and subsequently remitted to the Canada Revenue Agency (CRA). The crucial element distinguishing HST from separate GST and PST systems is its integration: it is one tax with one rate, applied universally to most taxable supplies in HST-participating provinces. This eliminates the need for businesses to calculate and remit two separate taxes, streamlining their financial operations significantly.

The Federal GST Component

The federal portion of the HST is equivalent to the Goods and Services Tax (GST), which is a 5% tax applied across all of Canada. This federal tax is a broad-based consumption tax applicable to most goods and services sold or provided in Canada. When a province harmonizes its PST with the GST, this 5% federal rate forms the base upon which the provincial component is added. This ensures that the federal government’s revenue stream from consumption remains consistent across all provinces, whether they have HST or not.

The Provincial Sales Tax (PST) Component

The provincial component of the HST replaces the former provincial sales tax in harmonized provinces. This provincial rate varies among the HST provinces. For example, Ontario’s HST rate is 13%, comprising the 5% federal GST and an 8% provincial component. Nova Scotia has a 15% HST (5% federal + 10% provincial). This provincial portion directly contributes to the provincial government’s revenue, funding essential public services. The decision for a province to join the HST framework often involves complex negotiations with the federal government, including compensation packages to offset potential initial revenue losses or adjustment costs.

Calculation and Application in Practice

When a consumer purchases a taxable good or service in an HST province, the HST is calculated on the selling price. For instance, if an item costs $100 in Ontario (HST 13%), the consumer pays $100 + ($100 * 0.13) = $113. The vendor collects the $13 HST. This simplicity is a significant benefit for both businesses and consumers, as it presents a clear, single tax amount. The ‘harmonized’ aspect also extends to the types of goods and services taxed, generally aligning with what was previously subject to GST, which expanded the tax base for the provincial component compared to many former PST systems.

Who is Responsible for HST: Registrants and Consumers

The burden of HST ultimately falls on the end consumer, but the responsibility for collecting and remitting the tax lies with businesses. This makes businesses crucial intermediaries in the Canadian tax system.

HST Registrants and Their Obligations

Businesses that sell taxable goods and services in Canada and have annual worldwide revenues from taxable supplies exceeding $30,000 (the small supplier threshold) are generally required to register for GST/HST. Once registered, they become “HST registrants” and are legally obligated to:

- Charge HST on their taxable sales.

- Collect the HST from their customers.

- File regular HST returns with the CRA.

- Remit the net HST collected (HST collected minus eligible Input Tax Credits) to the CRA.

Failure to register when required, or failure to collect and remit HST, can result in penalties and interest charges.

Input Tax Credits (ITCs) for Businesses

A key feature of the GST/HST system, and a major benefit for registered businesses, is the ability to claim Input Tax Credits (ITCs). ITCs allow businesses to recover the GST/HST they paid on goods and services purchased for use in their commercial activities. This mechanism ensures that HST is ultimately a tax on final consumption and not on the intermediate steps of production and distribution. For example, if a registered business in Ontario buys office supplies for $200 and pays $26 in HST, they can claim an ITC for that $26. This $26 is then deducted from the HST they collected from their customers before remitting the balance to the CRA. This prevents “tax on tax” and keeps businesses competitive.

Navigating Exemptions, Zero-Rated Supplies, and Rebates

While HST is broadly applied, not all goods and services are subject to it, and certain conditions can lead to tax recovery for consumers. Distinguishing between different categories of supply is essential.

Key Distinctions: Taxable, Zero-Rated, and Exempt Supplies

- Taxable Supplies: These are goods and services on which HST must be charged. The vast majority of commercial activities fall into this category.

- Zero-Rated Supplies: These are taxable supplies, but the HST rate applied is 0%. Businesses that sell zero-rated goods or services (e.g., basic groceries, most prescription drugs, certain medical devices, exports) do not charge HST to their customers, but they can still claim ITCs for the HST they paid on inputs related to these sales. This effectively means they receive a full refund of any HST they incur in producing these supplies.

- Exempt Supplies: These are goods and services that are not subject to HST, and businesses selling them cannot claim ITCs for HST paid on related expenses. Common examples include certain financial services, residential rent, childcare services, and specific health and educational services. The distinction from zero-rated is critical: no HST is charged, but no ITCs can be claimed.

Common Scenarios for HST Rebates

Beyond ITCs for businesses, certain individuals and organizations may be eligible for HST rebates. These are provisions designed to reduce the tax burden in specific circumstances:

- New Housing Rebate: Individuals who purchase a newly constructed or substantially renovated home may be eligible for a rebate on a portion of the HST paid, provided certain conditions regarding the purchase price and occupancy are met.

- Public Service Bodies Rebate: Non-profit organizations, charities, and public sector entities often qualify for rebates on a portion of the HST paid on their purchases, recognizing their role in providing services to the community.

- Rebate for Goods and Services Provided to Non-Residents: In some cases, non-residents of Canada may claim a rebate for HST paid on certain eligible goods and services consumed while visiting Canada.

Understanding these nuances is vital for accurate tax planning and compliance for both individuals and organizations.

The Broader Impact of HST on the Canadian Economy

The implementation and ongoing operation of HST have had far-reaching effects on the Canadian economic landscape, influencing everything from investment decisions to consumer spending habits.

Streamlining for Businesses and Economic Efficiency

For businesses, particularly those operating across provincial borders, HST introduced a significant simplification. A single tax system for federal and provincial consumption taxes in harmonized provinces means:

- Reduced administrative overhead in calculating, collecting, and remitting taxes.

- Easier compliance, as businesses deal with one set of rules and one tax agency (CRA).

- Elimination of the “tax on tax” effect often associated with cascading PST systems, where PST was applied to a price that already included GST. This reduced input costs for many businesses, fostering greater efficiency and competitiveness.

These efficiencies are often cited as a key driver for economic growth, as they lower the cost of doing business and encourage investment.

Consumer Implications and Transparency

For consumers, the impact of HST has been mixed and often debated. While HST provides transparency by clearly stating the combined tax on receipts, initial transitions often led to price increases for services that were previously only subject to GST (or a lower PST rate). However, for goods that previously had a separate PST, the total tax burden might have remained similar or even decreased in some cases due to the elimination of the “tax on tax” effect. Provincial governments often implemented tax credits or rebates during the transition to mitigate the impact on lower-income households. Ultimately, HST aims to be a more efficient and neutral tax from an economic perspective, impacting consumer behavior by taxing consumption rather than income or investment. It remains a cornerstone of Canada’s fiscal policy, balancing revenue generation with economic considerations.