The Cornerstone of Financial Stability

Capital adequacy stands as a fundamental pillar within the global financial architecture, representing a critical measure of a financial institution’s health and resilience. At its core, capital adequacy refers to the sufficient amount of capital a bank or financial institution must hold to absorb potential losses and protect its depositors and the broader financial system. It serves as a safeguard against unforeseen economic downturns, market shocks, and operational failures, ensuring that institutions can continue to operate and meet their obligations even under stressful conditions. This concept is not merely an accounting requirement; it is a dynamic regulatory principle designed to foster stability and trust in the banking sector.

Defining Capital Adequacy

Capital adequacy is typically expressed through a ratio known as the Capital Adequacy Ratio (CAR), also referred to as the Capital-to-Risk-Weighted Assets Ratio (CRAR). This ratio compares a bank’s capital to its risk-weighted assets (RWAs). The higher the ratio, the more capital a bank holds relative to its risk exposures, indicating a stronger financial position. Regulators set minimum CAR requirements, ensuring that banks do not take on excessive risk without adequate financial backing. This capital acts as a buffer, cushioning the impact of potential losses from loan defaults, investment depreciation, or other financial shocks. Without sufficient capital, banks risk insolvency, which can trigger a domino effect across the financial system, leading to widespread economic disruption.

Why It Matters: Mitigating Risk

The primary importance of capital adequacy lies in its role in mitigating systemic risk. Banks are interconnected entities, and the failure of one institution can quickly spread to others, potentially leading to a financial crisis. By requiring banks to maintain adequate capital, regulators aim to prevent such contagion. Capital adequacy requirements serve several critical functions:

- Protection of Depositors: Ensures that banks have enough reserves to return depositors’ money, even if significant losses occur.

- Maintenance of Market Confidence: A strong capital base signals to investors, creditors, and other market participants that a bank is sound and capable of weathering financial storms, thereby reducing uncertainty and promoting stability.

- Limiting Excessive Risk-Taking: Capital acts as a constraint on a bank’s ability to engage in overly risky lending or investment activities, as higher risk activities generally require more capital to be held against them.

- Fostering Financial System Stability: By making individual banks more resilient, capital adequacy contributes to the overall stability of the financial system, preventing crises that can have severe economic consequences.

Regulatory Frameworks and Evolution

The concept of capital adequacy has evolved significantly over time, particularly in response to financial crises that highlighted weaknesses in banking regulations. The most influential framework governing capital adequacy globally is the Basel Accords, developed by the Basel Committee on Banking Supervision (BCBS). These accords provide a standardized approach to calculating capital requirements, fostering a level playing field and promoting international financial stability.

Basel Accords: A Global Standard

The Basel Accords—specifically Basel I, Basel II, and Basel III—represent progressive enhancements to banking regulation:

- Basel I (1988): Introduced the first international standard for capital adequacy, primarily focusing on credit risk. It established a minimum CAR of 8% for internationally active banks, classifying assets into broad risk categories (e.g., 0% for government bonds, 100% for corporate loans). While a landmark achievement, its simplicity was a limitation, as it didn’t fully capture operational and market risks.

- Basel II (2004): A more sophisticated framework built on “three pillars”: minimum capital requirements (expanded to include market and operational risks, with more granular risk weighting), supervisory review of capital adequacy, and market discipline through enhanced disclosures. Basel II allowed banks to use their internal risk models, leading to more risk-sensitive capital calculations but also increasing complexity.

- Basel III (post-2008 financial crisis): Introduced in response to the global financial crisis, Basel III significantly strengthened capital requirements. It increased the quantity and quality of capital, introduced new capital buffers (e.g., capital conservation buffer, counter-cyclical buffer), and focused on improving liquidity and leverage ratios. Its aim was to make banks more resilient during periods of stress and reduce the likelihood of future financial crises.

Key Ratios: CAR and Tiered Capital

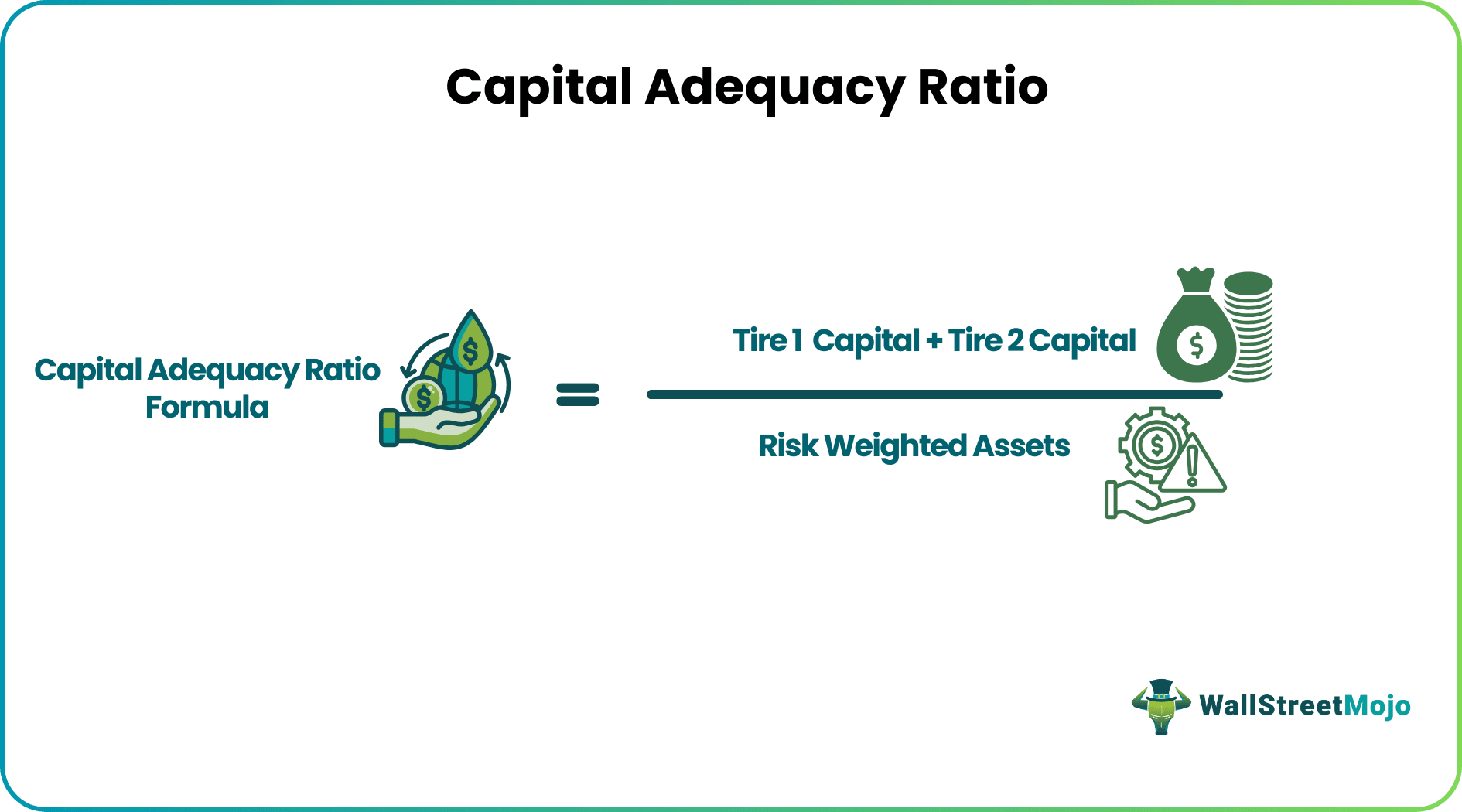

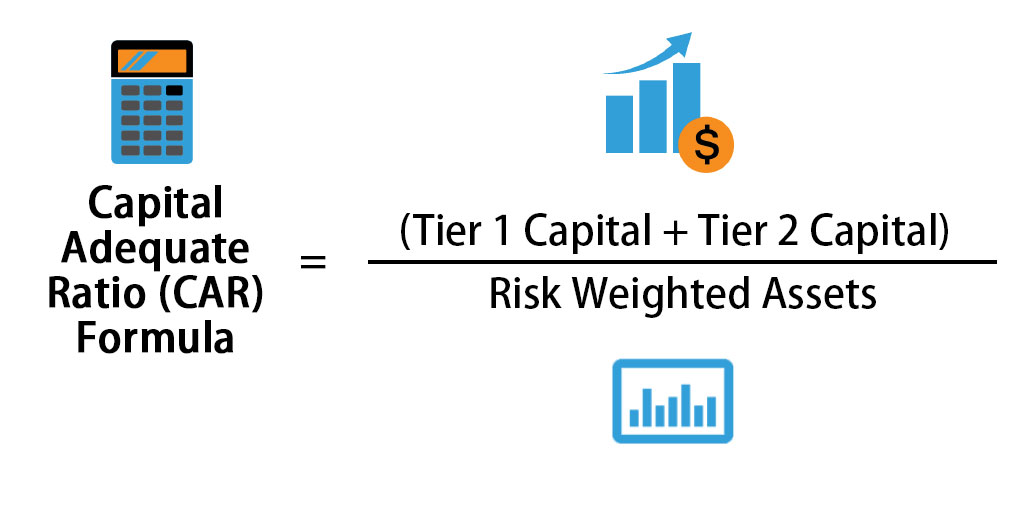

The Capital Adequacy Ratio (CAR) is the central metric for assessing a bank’s capital health. It is calculated as:

CAR = (Tier 1 Capital + Tier 2 Capital) / Risk-Weighted Assets

This formula highlights the two main components of regulatory capital:

- Tier 1 Capital: Often referred to as “core capital,” this is the highest quality capital, consisting primarily of common equity and retained earnings. It is permanent and readily available to absorb losses. Regulators consider Tier 1 capital the most reliable indicator of a bank’s financial strength.

- Tier 2 Capital: Known as “supplementary capital,” this includes other forms of capital that absorb losses in the event of liquidation, such as revaluation reserves, undisclosed reserves, hybrid capital instruments, and subordinated debt. While important, it is considered less permanent than Tier 1 capital.

Risk-Weighted Assets (RWAs) are a crucial element in the CAR calculation. Instead of simply summing a bank’s assets, RWAs assign different risk weights to various assets based on their perceived credit, market, and operational risks. For example, a cash holding might have a 0% risk weight, while a subprime mortgage loan might have a much higher risk weight. This ensures that banks holding riskier assets are required to hold more capital.

Components of Capital

Understanding the distinct components of capital is essential for appreciating the nuances of capital adequacy. The Basel framework categorizes capital into tiers to reflect varying degrees of loss-absorbing capacity and permanence.

Tier 1 Capital: Core Strength

Tier 1 capital represents a bank’s core financial strength and is the highest quality of capital. It comprises the most permanent and readily available funds to absorb losses, allowing a bank to continue functioning even in severe financial distress. Key elements of Tier 1 capital include:

- Common Equity Tier 1 (CET1): This is the purest form of Tier 1 capital and includes common shares issued by the bank, retained earnings, accumulated other comprehensive income, and other disclosed reserves. CET1 is crucial because it can absorb losses without triggering the bank’s liquidation. Basel III significantly increased the focus on CET1, making it the dominant component of regulatory capital.

- Additional Tier 1 (AT1): This includes other instruments that are perpetual and subordinate to depositors and general creditors, such as perpetual non-cumulative preferred stock. These instruments can absorb losses through conversion to equity or write-down mechanisms.

Tier 2 Capital: Supplementary Support

Tier 2 capital complements Tier 1 capital and provides an additional layer of protection, particularly in the event of a bank’s liquidation. While it also absorbs losses, it is considered less permanent and less readily available than Tier 1 capital. Components of Tier 2 capital include:

- Subordinated Debt: Debt instruments that rank below other claims in the event of liquidation, meaning their holders are paid only after senior creditors.

- Hybrid Capital Instruments: Securities that possess characteristics of both debt and equity.

- Revaluation Reserves: Reserves arising from the revaluation of assets, though these are typically subject to various adjustments and haircuts to reflect their true loss-absorbing capacity.

- General Loan Loss Provisions: Allowances made by banks for potential future loan defaults, limited to a certain percentage.

Risk-Weighted Assets (RWAs)

The denominator of the CAR, Risk-Weighted Assets, is pivotal. It adjusts a bank’s total assets for their inherent riskiness. This approach moves beyond simply looking at the absolute size of a bank’s balance sheet to assess its capital needs. Different asset classes are assigned risk weights (e.g., 0% for government bonds, 20% for interbank loans, 100% for corporate loans) based on their probability of default and loss severity. The calculation of RWAs can be complex, involving sophisticated models for credit risk, market risk (risk from changes in market prices), and operational risk (risk from failures in internal processes or systems). The accuracy of RWA calculation is critical, as it directly impacts the capital a bank is required to hold.

Implications for Banks and the Economy

The strict adherence to capital adequacy requirements has profound implications for individual banks, their operational strategies, and the broader economic landscape. These regulations shape how banks conduct business, manage risk, and contribute to economic growth.

Lending Capacity and Growth

Capital adequacy directly influences a bank’s capacity for lending. A bank must hold a certain amount of capital for every unit of risk-weighted assets it creates (e.g., by issuing loans). If a bank has low capital or is close to its minimum CAR, its ability to expand lending is constrained. This can have a ripple effect on the economy, as reduced bank lending can stifle business investment, consumer spending, and overall economic growth. Conversely, well-capitalized banks are better positioned to support economic expansion by providing credit, even during periods of uncertainty. However, excessively high capital requirements, while ensuring safety, can potentially increase the cost of credit and reduce its availability, posing a delicate balance for regulators.

Investor Confidence and Market Perception

A strong capital adequacy ratio is a key indicator of a bank’s financial health and stability, significantly impacting investor confidence. Investors, analysts, and rating agencies closely monitor these ratios when evaluating a bank’s prospects. Banks with robust capital buffers are generally perceived as safer investments, attracting more capital and enjoying lower borrowing costs. This positive perception can translate into higher stock valuations, easier access to funding, and enhanced reputation. Conversely, banks struggling to meet capital requirements face increased scrutiny, may see their credit ratings downgraded, and could experience a loss of investor trust, making it harder and more expensive to raise capital.

Preventing Systemic Crises

Perhaps the most critical implication of capital adequacy is its role in preventing systemic financial crises. The 2008 global financial crisis starkly illustrated how the interconnectedness of undercapitalized banks could lead to a rapid and devastating collapse of the entire financial system. By mandating sufficient capital, regulators aim to build a financial system where individual bank failures, while undesirable, do not automatically trigger widespread contagion. Capital buffers provide individual institutions with the resilience to absorb significant losses, reducing the likelihood that taxpayers will be called upon to bail out failing banks, as was common in past crises. This mechanism enhances the stability of the global financial system, protecting economies from severe downturns.

Challenges and Future Outlook

Despite its critical role, capital adequacy regulation faces continuous challenges, requiring ongoing adaptation and foresight from policymakers. The financial landscape is dynamic, with new risks constantly emerging, demanding a flexible yet robust regulatory approach.

Balancing Safety with Profitability

One of the perpetual challenges in capital adequacy regulation is finding the optimal balance between ensuring financial safety and allowing banks to operate profitably. Higher capital requirements, while making banks safer, can tie up a significant portion of their assets, potentially reducing their return on equity (ROE) and making banking less attractive to investors. Banks argue that excessive capital requirements can lead to higher lending costs, reduced credit availability, and a competitive disadvantage against less-regulated entities or shadow banking systems. Regulators, on the other hand, prioritize stability, recognizing that the long-term costs of a financial crisis far outweigh the short-term benefits of lower capital requirements. Striking this balance is a continuous negotiation, often influenced by economic cycles and market conditions.

Emerging Risks and Regulatory Adaptation

The financial industry is constantly evolving, presenting new risks that capital adequacy frameworks must address. The rise of digitalization, FinTech, and crypto assets introduces novel operational, cyber, and liquidity risks. Geopolitical tensions, climate change-related financial risks, and evolving global supply chains also pose significant challenges. Regulatory frameworks, such as Basel III, are periodically reviewed and updated to account for these emerging threats. For instance, discussions around capital requirements for banks’ exposures to crypto assets or the integration of climate-related financial risks into stress tests are ongoing. The future of capital adequacy will likely involve an even more granular assessment of diverse risk factors, potentially leveraging advanced data analytics and artificial intelligence to monitor and anticipate systemic vulnerabilities. The goal remains to maintain a resilient financial system capable of adapting to a rapidly changing global environment.