Understanding Custodial Accounts for Minors

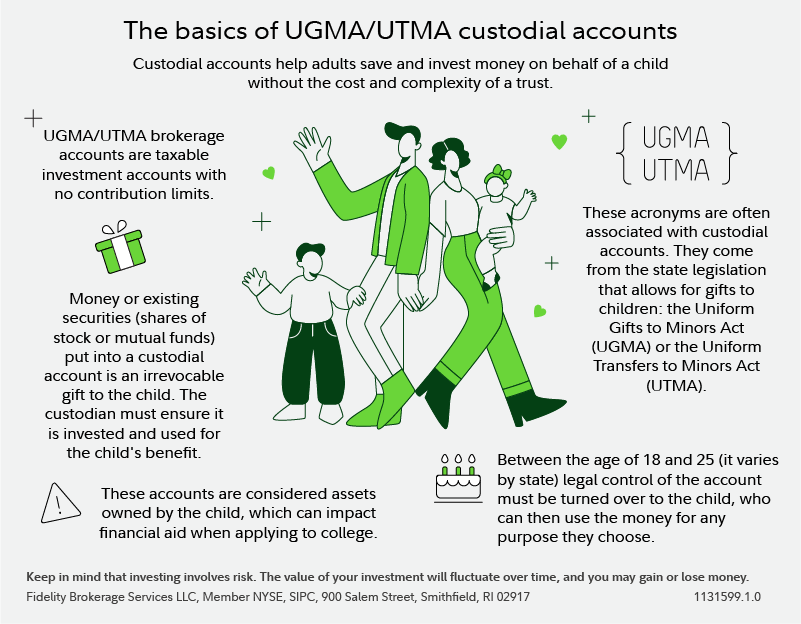

A Uniform Gifts to Minors Act (UGMA) account or a Uniform Transfers to Minors Act (UTMA) account represents a straightforward and widely utilized financial tool designed for adults to gift assets to minors without the necessity of establishing a formal trust. These custodial accounts are invaluable for parents, grandparents, or other benefactors looking to contribute to a child’s financial future, be it for education, a first home, or simply to instill early financial literacy. Unlike traditional trusts, UGMA/UTMA accounts are relatively simple to establish and maintain, making them accessible options for many families. They provide a legal framework for a custodian—typically the adult who opens the account—to manage the assets for the minor’s benefit until the minor reaches a specified age of majority, at which point the assets automatically transfer to their ownership.

The Core Purpose: Gifting to Minors

The fundamental objective of UGMA and UTMA accounts is to facilitate irrevocable gifts to minors. Historically, gifting significant assets to minors presented legal complexities, often requiring intricate trusts or court-appointed guardianships. The UGMA and subsequently the UTMA were enacted to simplify this process, providing a legal mechanism to transfer wealth to children in a structured manner. Donors can contribute cash, securities, or other forms of property, knowing that these contributions are legally binding gifts that belong to the child, even if managed by an adult. This setup allows for long-term financial planning for children, enabling the growth of investments over many years, potentially capitalizing on compounding returns. The gifts are considered final upon contribution, meaning the donor cannot revoke them or reclaim the assets, reinforcing the account’s primary function as a dedicated financial resource for the minor.

Key Players: Custodian and Beneficiary

Every UGMA/UTMA account involves two primary roles: the custodian and the beneficiary. The beneficiary is always the minor for whom the account is established. This child holds the legal right to the assets, though they do not have direct control until they reach the age of majority. The custodian, on the other hand, is an adult responsible for managing the account’s assets prudently and in the best interest of the minor beneficiary. This includes making investment decisions, handling distributions, and ensuring compliance with all legal and tax requirements. The custodian often is the donor themselves, a parent, or another trusted adult. It is crucial to understand that the custodian acts in a fiduciary capacity, meaning they have a legal and ethical obligation to manage the funds responsibly for the child. They cannot use the funds for their personal benefit, nor can they revoke the gift. Upon the minor reaching the age of majority (typically 18 or 21, depending on state law and the account type), the custodian’s role ceases, and full control of the assets is transferred directly to the now-adult beneficiary.

Assets Held Within UGMA/UTMA

One of the defining characteristics of UGMA and UTMA accounts is the range of assets they can hold, although there are distinctions between the two acts. UGMA accounts are generally more restrictive, typically limited to financial assets such as cash, stocks, bonds, mutual funds, and insurance policies. This makes them ideal for straightforward investment portfolios. UTMA accounts, however, offer a broader scope. They can hold virtually any type of property, including real estate, intellectual property, patents, royalties, and even collectibles, in addition to the financial assets permissible under UGMA. This expanded flexibility makes UTMA accounts a more versatile option for donors wishing to transfer a wider array of assets to a minor. Regardless of the specific act, the assets within these accounts are typically invested to grow over time, contributing to the minor’s long-term financial well-being.

Benefits and Advantages of UGMA/UTMA Accounts

UGMA/UTMA accounts offer several compelling advantages, making them a popular choice for intergenerational wealth transfer. Their primary draw lies in their simplicity, tax efficiency, and the potential to provide a substantial financial head start for young beneficiaries. These benefits contribute to their widespread use as a foundational element in a child’s financial planning strategy.

Tax Efficiency: The “Kiddie Tax” Rule

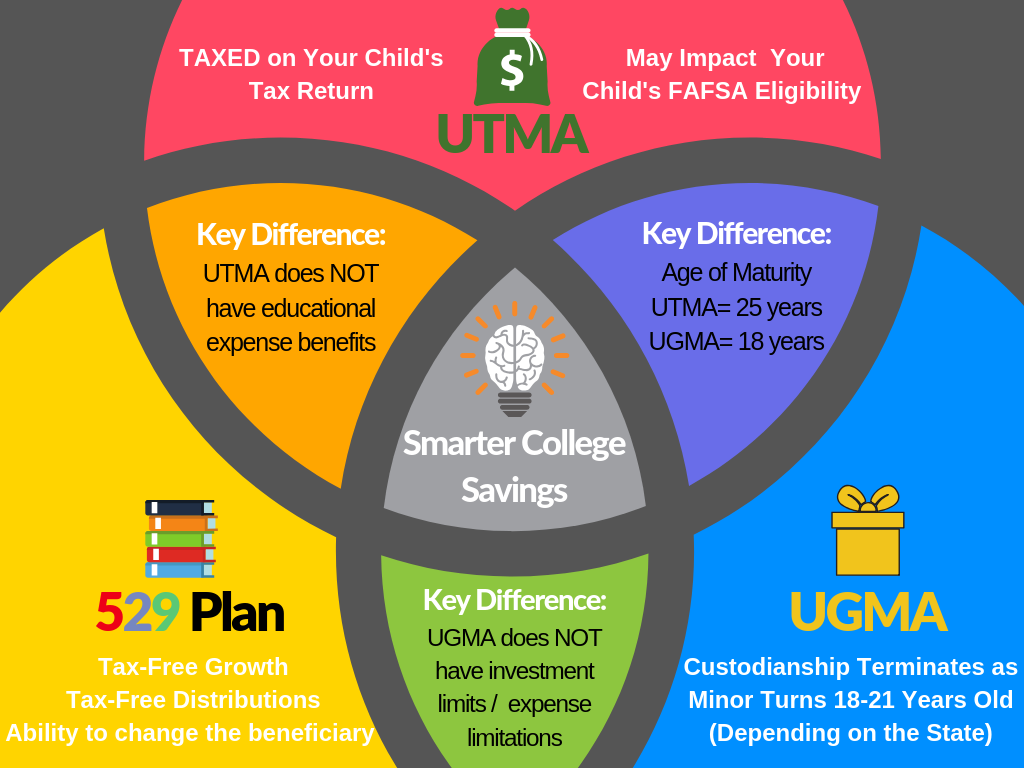

A significant benefit of UGMA/UTMA accounts often cited is their potential for tax efficiency, primarily due to the “Kiddie Tax” rule. Under this rule, a certain amount of the minor’s unearned income (such as interest, dividends, and capital gains from the custodial account) is taxed at the child’s lower tax rate rather than the parents’ potentially higher rate. For 2024, the first $1,250 of a child’s unearned income is typically tax-free, and the next $1,250 is taxed at the child’s income tax rate. Any unearned income above $2,500, however, is subject to the parents’ marginal income tax rate. While this rule limits the tax arbitrage potential for very large accounts, it still offers an advantage for smaller and moderately sized accounts compared to assets held directly by the parent. This tax treatment can allow the account’s investments to grow more rapidly over time by minimizing the tax drag on earnings, thereby maximizing the long-term benefit for the minor.

Simplicity in Gifting and Management

One of the most attractive features of UGMA/UTMA accounts is their simplicity. Establishing these accounts is typically straightforward, often requiring only a few forms at a bank or brokerage firm, significantly less complex and costly than setting up a formal trust. Donors can make contributions with ease, and the custodial structure simplifies the management process. The designated custodian handles all investment decisions and administrative tasks until the minor reaches the age of majority. This simplicity extends to the legal aspects as well; the statutory framework of UGMA and UTMA eliminates the need for complex legal drafting or ongoing legal oversight that a trust might require. This ease of setup and management makes these accounts an accessible option for individuals who wish to make meaningful financial gifts to minors without navigating extensive legal procedures.

Fostering Financial Literacy

Beyond the direct financial benefits, UGMA/UTMA accounts can play a crucial role in fostering financial literacy in young beneficiaries. As children grow older, they can observe the custodian managing the account, learn about investments, and understand the principles of saving and compounding. When the assets are eventually transferred to them, they gain hands-on experience in managing a substantial sum of money. This direct exposure to financial concepts and responsibilities at a formative age can be invaluable. It provides a practical foundation for making informed financial decisions in adulthood, helping them understand budgeting, investing, and the importance of long-term financial planning. Many custodians engage their minor beneficiaries in discussions about the account’s performance and investment choices, transforming the account into a living educational tool.

Important Considerations and Potential Drawbacks

While UGMA/UTMA accounts offer considerable benefits, potential donors and custodians must be aware of certain considerations and drawbacks. These accounts come with inherent inflexibilities and can impact future financial aid eligibility, which are critical factors to weigh before establishment. Understanding these limitations ensures that a UGMA/UTMA account aligns with the donor’s long-term objectives and the beneficiary’s needs.

Irrevocability and Loss of Donor Control

A fundamental characteristic of UGMA/UTMA accounts is the irrevocability of gifts. Once assets are contributed to the account, they legally belong to the minor beneficiary and cannot be reclaimed by the donor, nor can the custodian use them for any purpose other than the minor’s benefit. This means the donor permanently relinquishes control over the gifted assets. While the custodian manages the account until the minor reaches the age of majority, they cannot change the beneficiary or withdraw funds for their own use, even in unforeseen financial emergencies for the donor or custodian. This loss of control can be a significant drawback if the donor anticipates needing access to those funds in the future or if circumstances change regarding the minor’s needs or behavior. The assets are irrevocably dedicated to the minor, irrespective of future events.

Impact on College Financial Aid Eligibility

One of the most significant potential drawbacks of UGMA/UTMA accounts is their adverse impact on a beneficiary’s eligibility for need-based college financial aid. When a student applies for federal financial aid (FAFSA), assets held in a UGMA/UTMA account are reported as the student’s assets, not the parents’. Student assets are assessed at a significantly higher rate—typically 20% of their value—compared to parent assets, which are assessed at a maximum of 5.64%. This higher assessment rate means that a UGMA/UTMA account can substantially reduce the amount of financial aid a student is eligible to receive, potentially offsetting the tax benefits or investment growth realized within the account. Families planning to rely on need-based aid for college expenses should carefully consider this impact and explore alternative savings vehicles like 529 plans, which are treated more favorably in financial aid calculations.

Tax Implications Post-Majority Age

While UGMA/UTMA accounts offer some tax advantages during the minor’s younger years due to the Kiddie Tax rules, the tax implications can change once the beneficiary reaches the age of majority. At this point, the assets transfer fully to the beneficiary’s control, and all future income and capital gains generated by these assets will be taxed at the beneficiary’s own income tax rate. If the beneficiary is still a student or in the early stages of their career, their income might be low, making this less of an issue. However, if the beneficiary enters a higher income bracket, the tax efficiency initially enjoyed by the account diminishes. Additionally, the transfer of ownership at the age of majority may trigger capital gains taxes if investments are sold immediately, or if the beneficiary decides to manage the portfolio differently, which is a consideration for beneficiaries and their families to plan for.

UGMA vs. UTMA: Key Distinctions

While both UGMA and UTMA accounts serve the same fundamental purpose of facilitating gifts to minors, they are distinct acts with important differences. The Uniform Transfers to Minors Act (UTMA) was enacted to address some of the limitations of the older Uniform Gifts to Minors Act (UGMA), primarily by expanding the types of assets that can be held and offering slightly more flexibility in terms of the age of majority. Understanding these distinctions is crucial for donors to select the most appropriate account type based on their specific gifting goals and the nature of the assets they intend to transfer.

Scope of Assets

The most significant difference between UGMA and UTMA lies in the scope of assets they can hold. UGMA accounts are generally limited to cash, bank deposits, securities (stocks, bonds, mutual funds), and life insurance policies. They are well-suited for traditional financial investments. UTMA, on the other hand, is much broader. It permits the inclusion of virtually any type of property, including real estate, tangible personal property (like art or collectibles), limited partnership interests, and other forms of intellectual property, in addition to all the assets permissible under UGMA. This expanded asset holding capability makes UTMA a more versatile choice for donors with diverse asset portfolios or those wishing to gift non-traditional assets to a minor. The availability of UTMA accounts varies by state, as some states have only adopted UGMA, while most have transitioned to UTMA.

Age of Majority

Another key distinction is the age at which the assets within the account automatically transfer to the beneficiary’s full control. Under UGMA, the age of majority is typically 18 or 21, depending on state law. Once the minor reaches this age, the custodian is legally required to transfer all assets to them. UTMA accounts often provide a bit more flexibility in this regard. While the standard age of majority is usually 21 (or 18 in some states), some states that have adopted UTMA allow the donor to specify an older age for transfer, often up to 25 years old. This extended custodianship can be beneficial for donors who believe a beneficiary might not be mature enough to handle a significant sum of money at 18 or 21. This allows for a longer period of guided management, potentially ensuring the funds are used more prudently for educational or other life goals. However, the exact maximum age for transfer under UTMA can vary significantly from state to state.

State-Specific Variations

It is imperative to note that both UGMA and UTMA are state laws, meaning their specific provisions can vary depending on the state where the account is opened or the custodian resides. While the core principles remain consistent, details such as the specific age of majority, the exact types of assets allowed (especially for UTMA), and administrative requirements can differ. For instance, some states may only have UGMA in effect, while others have adopted UTMA exclusively. The option to extend the age of majority for UTMA accounts is also state-dependent. Therefore, before establishing either type of account, donors should consult with a financial advisor or legal professional familiar with the laws of their specific state to ensure compliance and to choose the account that best fits their objectives.

Establishing and Managing a Custodial Account

Setting up and managing a UGMA or UTMA account is a relatively straightforward process, designed to be accessible to a wide range of donors. However, it involves important steps and ongoing responsibilities for the custodian. Proper establishment ensures the account functions as intended, while diligent management protects the beneficiary’s interests and optimizes the account’s growth.

Steps to Open an Account

Opening a UGMA/UTMA account typically involves a few simple steps. First, the donor needs to choose a financial institution, such as a bank, brokerage firm, or mutual fund company, that offers custodial accounts. Next, the donor will need to complete an application form, providing information about themselves as the donor/custodian and the minor beneficiary. This includes full legal names, addresses, Social Security numbers, and dates of birth for both parties. The donor then designates the initial assets to be transferred into the account, which can be cash, securities, or other permissible property. Once the account is established and funded, the designated custodian gains legal authority to manage the assets. It’s crucial for the donor to understand that once the initial gift is made, it is irrevocable. Future contributions can be made by the initial donor or other individuals, expanding the account’s value over time.

Custodian’s Fiduciary Responsibilities

The custodian plays a pivotal role in a UGMA/UTMA account, holding significant fiduciary responsibilities. This means they are legally and ethically obligated to manage the account’s assets prudently, solely in the best interest of the minor beneficiary. Their duties include making informed investment decisions, ensuring the portfolio aligns with the minor’s long-term needs, and keeping accurate records of all transactions. The custodian must avoid conflicts of interest and cannot use the account’s funds for personal gain or to fulfill their own parental support obligations to the child. They are also responsible for filing any necessary tax returns for the account and ensuring all distributions are made appropriately for the minor’s benefit. This role requires diligence, honesty, and a solid understanding of investment principles to ensure the assets grow effectively until transferred to the beneficiary.

Transitioning Ownership to the Beneficiary

The conclusion of a UGMA/UTMA account’s custodial phase occurs when the minor beneficiary reaches the age of majority as defined by state law and the specific account type (typically 18, 21, or up to 25 for some UTMA accounts). At this point, the custodian’s role legally terminates, and they are required to transfer full control and ownership of all remaining assets in the account to the now-adult beneficiary. This transfer is automatic and absolute; the beneficiary then has complete discretion over how to use or manage the funds. The custodian’s responsibility includes providing the beneficiary with all necessary account statements, tax documents, and investment information to facilitate a smooth transition. It is advisable for custodians to prepare the beneficiary for this responsibility by educating them about financial management during their teenage years, ensuring they are well-equipped to handle their new financial independence.