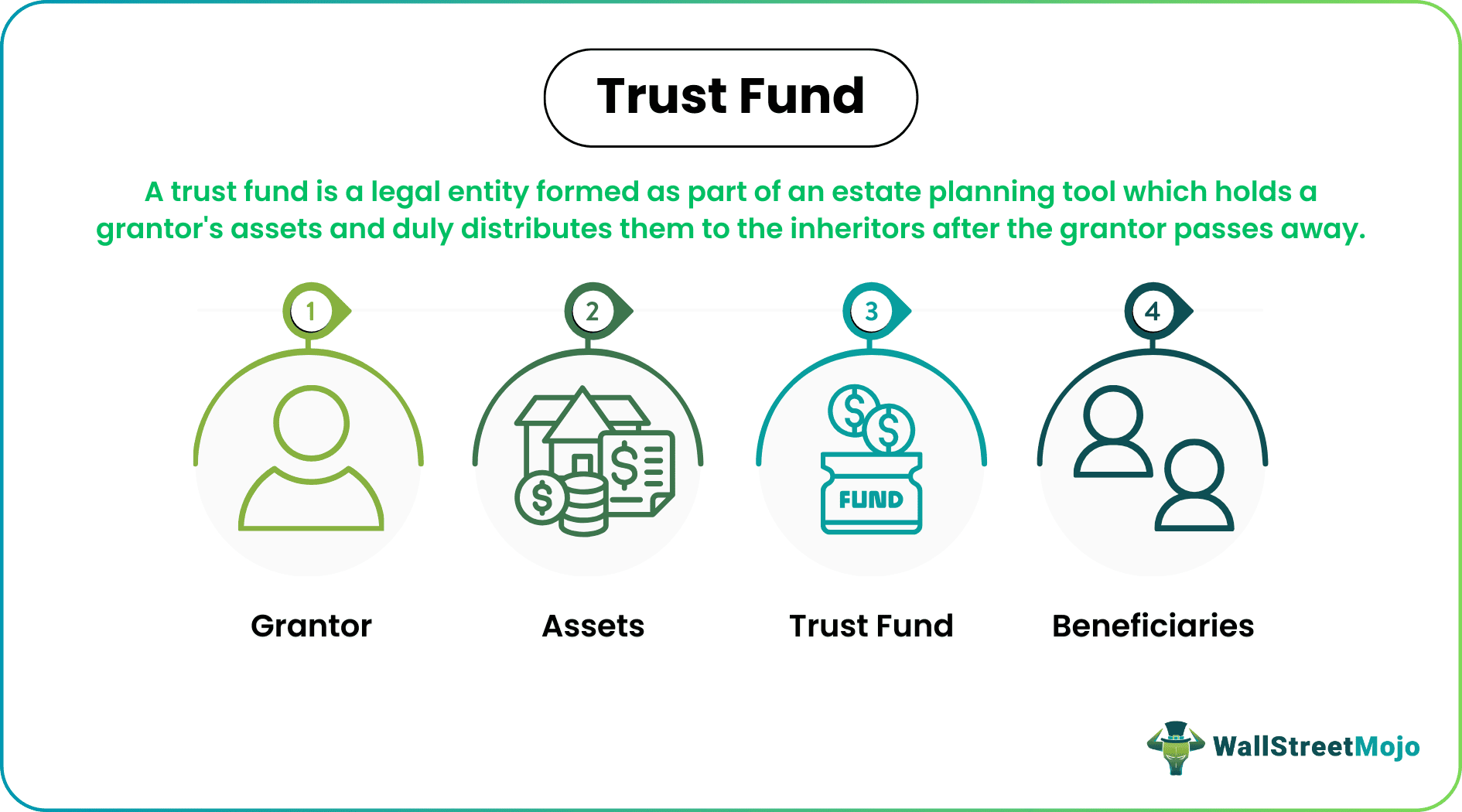

A trust fund represents a sophisticated legal arrangement designed to hold assets for the benefit of an individual or group, managed by a third party. Far from being an exclusive tool for the ultra-wealthy, trusts serve as foundational instruments in comprehensive estate planning, offering unparalleled flexibility, privacy, and control over how assets are distributed and managed over time. At its core, a trust involves a grantor (the creator of the trust), a trustee (the manager of the assets), and beneficiaries (those who receive the benefits from the trust’s assets). This tripartite structure facilitates the transfer and stewardship of wealth, ensuring that the grantor’s intentions for their legacy are meticulously carried out, often long after they are no longer able to manage their affairs. Understanding the nuances of trust funds is crucial for anyone contemplating effective wealth management, charitable giving, or securing the financial future of loved ones.

The Foundational Elements of a Trust Fund

To grasp the full utility of a trust fund, it’s essential to delineate its primary components and how they interact to form a cohesive financial mechanism. The relationships between the parties involved are governed by a legally binding document, the trust agreement, which outlines the rules for asset management and distribution.

Key Parties in a Trust

Every trust fund operates through the interplay of three fundamental roles:

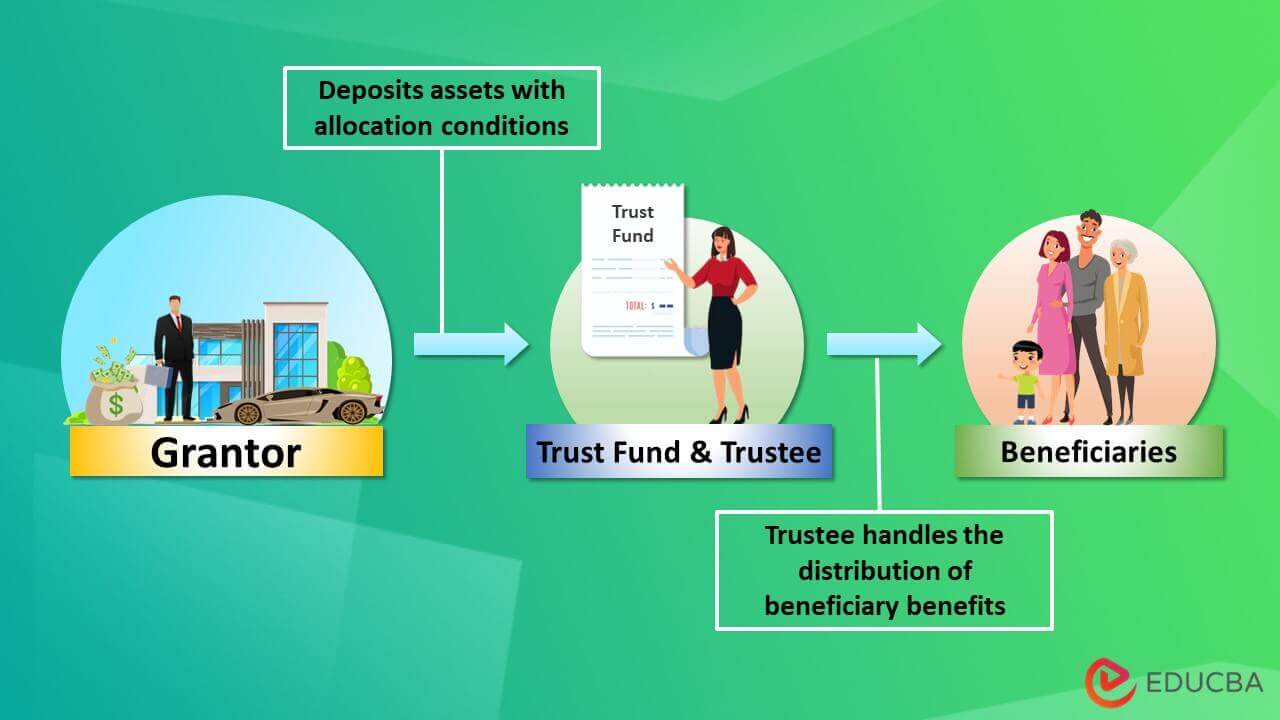

- The Grantor (or Settlor/Trustor): This is the individual or entity who creates the trust. The grantor contributes assets to the trust and defines the terms and conditions under which those assets will be managed and distributed. Their intentions are paramount and are meticulously detailed within the trust agreement.

- The Trustee: Appointed by the grantor, the trustee is the individual or institution (such as a bank or trust company) legally responsible for holding and managing the trust’s assets. The trustee has a fiduciary duty to act in the best interests of the beneficiaries, adhering strictly to the terms set forth in the trust agreement. Their duties include investing assets prudently, distributing income and principal according to the trust’s stipulations, and providing regular accounting to the beneficiaries.

- The Beneficiary: These are the individuals or entities who are designated to receive the benefits from the trust’s assets. Beneficiaries can be immediate family members, charities, or any other person or organization the grantor wishes to support. A trust can have multiple beneficiaries, and the distribution terms can vary, specifying when, how much, and under what conditions they receive assets (e.g., reaching a certain age, completing education, or specific life events).

How a Trust Differs from a Will

While both wills and trusts are integral to estate planning, they serve distinct purposes and operate differently. A will is a legal document that dictates how an individual’s property will be distributed after their death and typically involves the probate process. Probate is a public, often lengthy, and sometimes costly legal procedure where a court validates the will and oversees the distribution of assets.

In contrast, a trust allows assets to bypass probate. When assets are placed into a trust, they are legally transferred from the grantor’s name to the trust’s name. This means that upon the grantor’s death, the assets within the trust can be managed and distributed by the trustee directly to the beneficiaries according to the trust’s terms, without court intervention. This distinction offers significant advantages in terms of privacy, speed, and cost efficiency. Furthermore, a trust can provide for asset management during the grantor’s lifetime if they become incapacitated, a feature a will does not offer.

Diverse Structures: Types of Trust Funds

Trust funds are not monolithic; they come in various forms, each tailored to specific financial goals, legal requirements, and grantor objectives. The choice of trust type often depends on the grantor’s desire for control, tax planning strategies, and the timing of asset distribution.

Revocable vs. Irrevocable Trusts

One of the most fundamental distinctions lies between revocable and irrevocable trusts:

- Revocable Living Trust: Also known as an “inter vivos” trust, a revocable trust can be altered, amended, or revoked entirely by the grantor during their lifetime, as long as they are mentally competent. The grantor often serves as the initial trustee and a beneficiary, maintaining significant control over the assets. While offering flexibility and avoiding probate, assets held in a revocable trust are generally still considered part of the grantor’s taxable estate upon death and are not protected from creditors.

- Irrevocable Trust: Once established and funded, an irrevocable trust generally cannot be changed, amended, or terminated by the grantor without the consent of the trustee and beneficiaries. The grantor relinquishes control over the assets once they are transferred into the trust. This lack of control, however, comes with significant benefits: assets in an irrevocable trust are typically removed from the grantor’s taxable estate, potentially reducing estate taxes, and are generally protected from creditors and legal judgments. They are often used for gifting, charitable planning, or qualifying for government benefits.

Other Specialized Trust Types

Beyond the revocable/irrevocable dichotomy, several other specialized trusts cater to specific needs:

- Testamentary Trust: Unlike a living trust, a testamentary trust is established through a will and comes into existence only after the grantor’s death, following the probate of the will. It provides a structured way to manage assets for beneficiaries who might be minors or have special needs, ensuring funds are distributed responsibly over time rather than in a lump sum.

- Special Needs Trust (Supplemental Needs Trust): Designed to benefit individuals with disabilities, these trusts allow beneficiaries to receive financial support without jeopardizing their eligibility for essential government benefits (like Medicaid or Supplemental Security Income). The trust assets are used to supplement, rather than replace, government assistance.

- Charitable Trusts: These trusts are designed for philanthropic giving.

- Charitable Remainder Trust (CRT): The grantor or other non-charitable beneficiaries receive income from the trust for a specified period, after which the remaining assets go to a designated charity.

- Charitable Lead Trust (CLT): Income is paid to a charity for a set period, and then the remaining assets revert to the grantor or other non-charitable beneficiaries.

- These trusts offer tax benefits to the grantor, including income tax deductions and potential estate tax reductions.

The Advantages of Establishing a Trust Fund

The strategic implementation of a trust fund offers a multitude of benefits, extending beyond mere asset distribution to encompass comprehensive wealth protection, tax efficiency, and enduring control.

Estate Planning and Probate Avoidance

One of the most compelling advantages of a trust, particularly a revocable living trust, is its ability to bypass probate. As previously noted, probate can be a protracted and public process. By holding assets in a trust, the transfer of ownership to beneficiaries occurs privately and often more quickly, minimizing legal fees and court costs associated with probate. This streamlined process ensures that beneficiaries gain access to assets without unnecessary delays, alleviating potential financial burdens during a time of grief.

Asset Protection and Control

Trusts provide an unparalleled degree of control over how and when assets are distributed. Grantors can set specific conditions for distribution, such as tying payouts to educational milestones, marriage, or responsible financial behavior. This control is invaluable for protecting beneficiaries who may be too young, financially inexperienced, or susceptible to mismanagement. For irrevocable trusts, assets are removed from the grantor’s personal ownership, offering a layer of protection against creditors, lawsuits, and even divorce settlements for beneficiaries, subject to specific legal regulations and the timing of the transfer.

Potential Tax Advantages

Certain types of trusts, particularly irrevocable trusts, can offer significant tax planning benefits. By removing assets from the grantor’s taxable estate, these trusts can help reduce estate taxes upon death, allowing a larger portion of wealth to pass to beneficiaries. Furthermore, income generated within some trusts may be subject to different tax treatments, and charitable trusts can provide immediate income tax deductions for the grantor. Navigating the complex landscape of trust taxation requires expert guidance, but the potential for substantial savings makes trusts a cornerstone of sophisticated financial planning.

Privacy

Unlike wills, which become public record once probated, the terms of a trust agreement remain private. This confidentiality ensures that the details of an individual’s wealth, beneficiaries, and distribution plans are not disclosed to the public, offering a valuable layer of discretion and protection against potential disputes or unwanted attention.

Setting Up a Trust Fund

Establishing a trust fund is a significant legal undertaking that requires careful consideration and professional guidance to ensure it aligns perfectly with your intentions and legal requirements.

Choosing a Trustee

The selection of a trustee is perhaps the most critical decision in establishing a trust. The trustee is entrusted with substantial responsibilities, including managing investments, making distributions, and maintaining meticulous records. Options include:

- Individual Trustee: A trusted family member, friend, or professional advisor. It’s crucial they possess financial acumen, integrity, and the willingness to fulfill their fiduciary duties diligently.

- Corporate Trustee: A bank, trust company, or wealth management firm. These institutions offer professional management, continuity regardless of an individual’s health, and adherence to regulatory standards, albeit typically for a fee.

It’s wise to appoint successor trustees to ensure continuity if the initial trustee becomes unable or unwilling to serve.

Funding the Trust

Once the trust agreement is drafted and signed, the next step is to “fund” the trust, which means transferring assets into its legal ownership. This crucial step is often overlooked, rendering an unfunded trust ineffective. Assets commonly placed in trusts include real estate, bank accounts, investment portfolios, business interests, and valuable personal property. The process involves retitling assets from the grantor’s name to the name of the trust.

The Critical Role of Legal and Financial Advice

Given the legal complexities, tax implications, and diverse options available, attempting to create a trust without professional assistance is ill-advised. An experienced estate planning attorney can:

- Help determine the most suitable type of trust for your specific goals.

- Draft a legally sound trust agreement that accurately reflects your intentions.

- Advise on tax consequences and strategies to optimize your estate plan.

- Ensure proper funding of the trust to avoid potential pitfalls.

- Coordinate the trust with other estate planning documents, such as wills and powers of attorney.

Collaborating with a financial advisor can also ensure that the assets within the trust are managed effectively to meet long-term objectives.

Common Misconceptions About Trust Funds

Many misconceptions surround trust funds, often perpetuated by popular culture or a lack of understanding. It’s important to clarify these to appreciate their true utility.

One common myth is that trusts are exclusively for the extremely wealthy. While trusts are indeed used by affluent individuals for sophisticated planning, they are increasingly accessible and beneficial for middle-income families seeking to avoid probate, protect minor children’s inheritances, or plan for potential incapacity. The value a trust offers in privacy, control, and efficiency can outweigh its setup costs for many individuals and families.

Another misconception is that establishing a trust is overly complicated and rigid. While the initial setup requires legal expertise, a properly drafted trust provides immense flexibility. Revocable trusts, as discussed, can be easily changed, while even irrevocable trusts can sometimes be modified with the consent of all parties or through legal processes. The goal of a well-crafted trust is to be adaptable to changing life circumstances, not to create an inflexible prison for assets.

In conclusion, trust funds are versatile and powerful tools in modern financial and estate planning. They offer robust solutions for asset management, wealth transfer, tax efficiency, and privacy, providing grantors with peace of mind that their legacy will be managed according to their wishes. While the initial setup requires careful planning and professional guidance, the long-term benefits in control, protection, and efficiency make them an invaluable component of a comprehensive financial strategy for many.