A hard inquiry, often referred to as a “hard pull” or “hard credit check,” is a critical component of the credit assessment process that can significantly influence an individual’s financial standing. It occurs when a lender or service provider genuinely reviews your credit report to make a lending decision. This deep dive into your financial history is typically initiated when you formally apply for new credit, such as a mortgage, car loan, personal loan, student loan, or a new credit card. Unlike a soft inquiry, a hard inquiry is recorded on your credit report and can subtly affect your credit score, making it a pivotal concept for anyone managing their financial health. Understanding its nature, implications, and how to manage it effectively is essential for maintaining a robust credit profile and securing favorable lending terms.

Understanding the Mechanics of a Hard Inquiry

At its core, a hard inquiry represents a formal request by a potential creditor to access your full credit report from one or more of the three major credit bureaus: Experian, Equifax, and TransUnion. This comprehensive review allows lenders to gauge your creditworthiness, assess your risk level, and ultimately decide whether to extend credit and on what terms. It’s a signal to other potential creditors that you are actively seeking new credit, which is why it holds a different weight than more casual credit checks.

The Distinction from Soft Inquiries

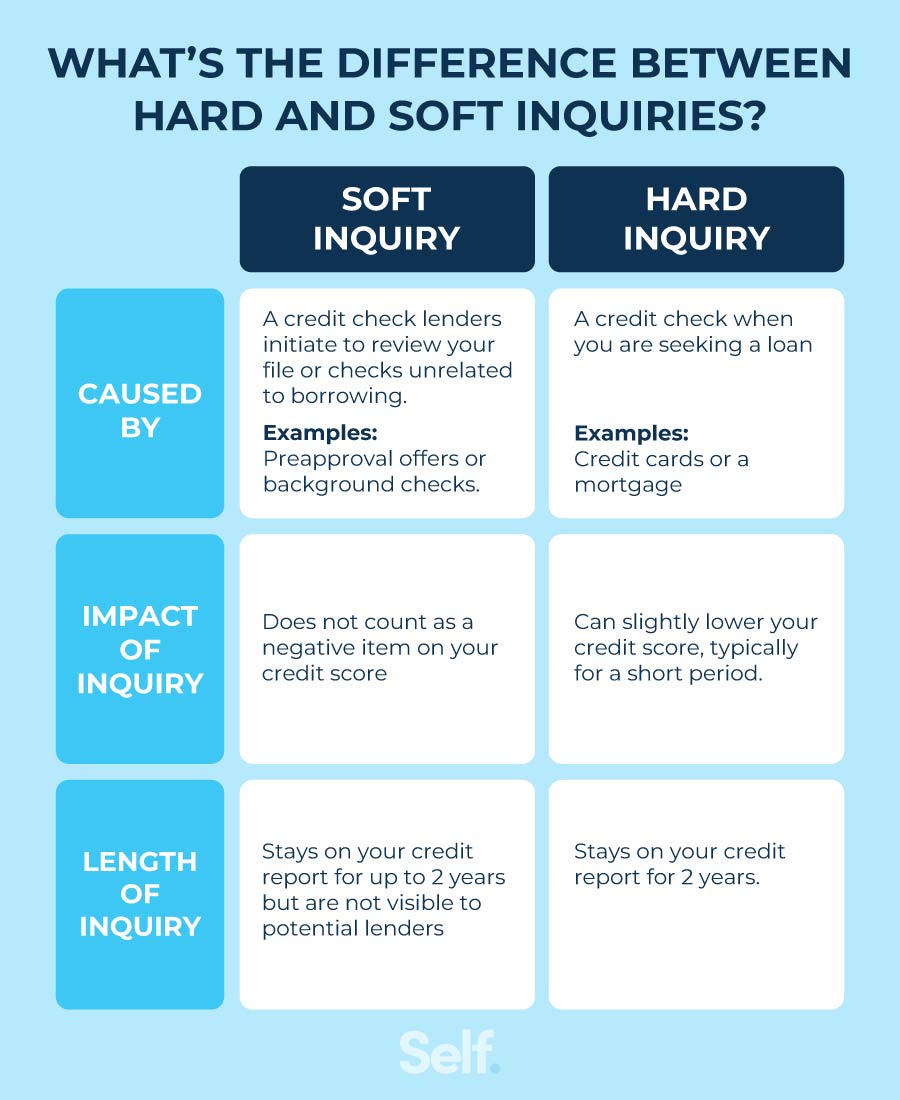

To fully grasp the significance of a hard inquiry, it’s crucial to differentiate it from a soft inquiry (or “soft pull”). While both involve accessing your credit information, their purposes, visibility, and impact are fundamentally different.

A soft inquiry occurs when you check your own credit score or report, or when a lender pre-approves you for an offer without you having formally applied. For instance, when credit card companies send you pre-approved offers in the mail, they conduct a soft inquiry. Employers might also perform a soft inquiry as part of a background check, though this is less common and often requires your explicit permission. Crucially, soft inquiries are not visible to other lenders and have absolutely no impact on your credit score. They are a way to assess general creditworthiness without triggering any flags or affecting your standing.

A hard inquiry, conversely, is a direct result of your active application for new credit. It signifies your intent to take on additional debt. Because it reflects a potential increase in your debt burden, credit scoring models interpret hard inquiries as a mild risk factor. This is why they are visible to other lenders on your credit report and can cause a minor, temporary dip in your credit score.

Common Scenarios for Hard Inquiries

Hard inquiries are a standard part of applying for most forms of substantial credit. Recognizing these situations can help you anticipate when your credit report will be accessed in this manner:

- Mortgage Applications: Seeking to finance a home is one of the most significant financial commitments, inevitably leading to hard inquiries from mortgage lenders.

- Auto Loans: When purchasing a vehicle through financing, car dealerships or banks will perform a hard inquiry to assess your eligibility and interest rates.

- Credit Card Applications: Applying for a new credit card, whether it’s your first or an additional one, will result in a hard inquiry.

- Personal Loans: Unsecured personal loans, used for various purposes like debt consolidation or home improvements, require a hard inquiry.

- Student Loans: While some student loans have different criteria, private student loans typically involve a hard inquiry.

- Some Apartment Rental Applications: In certain competitive rental markets, landlords or property management companies might perform a hard inquiry.

- Opening New Utility Accounts: Some utility providers (electricity, gas, water, internet) may conduct a hard inquiry, especially if you have limited credit history, to assess risk before providing service.

- Cell Phone Contracts: Entering into a new cell phone contract, particularly with a new provider, can sometimes trigger a hard inquiry.

Understanding these common triggers allows consumers to be more deliberate in their applications, minimizing unnecessary credit checks that could accumulate and collectively impact their score.

The Impact on Your Credit Score

The immediate and long-term effects of a hard inquiry on your credit score are a frequent concern for individuals striving to maintain excellent credit. While the impact is generally modest, its nuances warrant a thorough explanation.

Short-Term Score Fluctuations

When a hard inquiry appears on your credit report, it typically causes a slight, temporary dip in your credit score. For most individuals, this dip is minimal, often just a few points, and generally recovers within a few months. Credit scoring models view multiple new credit applications within a short period as a potential indicator of financial distress or an increased likelihood of taking on too much debt, thereby increasing risk. This is a primary reason why hard inquiries carry a small penalty.

However, the severity of this dip isn’t uniform. Several factors influence how much a hard inquiry will affect your score:

- Your existing credit history: Consumers with a long, established history of responsible credit management and a high credit score tend to experience a smaller impact. Their extensive positive data points can absorb the minor shock of a new inquiry more easily. Conversely, individuals with a thin credit file or a lower existing score might see a more noticeable, albeit still temporary, drop.

- The number of recent inquiries: A single hard inquiry is less concerning than several inquiries within a short timeframe. Multiple inquiries suggest a desperate search for credit, which credit bureaus interpret as higher risk.

- The type of credit: Mortgages and auto loans, for instance, often benefit from “rate shopping” rules, where multiple inquiries for the same type of loan within a specific window (typically 14 to 45 days, depending on the scoring model) are counted as a single inquiry. This mechanism is designed to allow consumers to shop for the best rates without penalizing them for prudent financial behavior.

The Lingering Presence on Your Report

A hard inquiry will remain on your credit report for approximately two years from the date it occurred. While it stays on your report for two years, its impact on your credit score typically fades much sooner. Most credit scoring models only consider inquiries from the past 12 months when calculating your score. After a year, even if the inquiry is still visible, it generally no longer plays a role in determining your score. This means that while a lender might still see an inquiry from 18 months ago, it won’t be actively dragging down your creditworthiness.

Factors Influencing Severity

Beyond the points mentioned, other aspects can subtly amplify or mitigate the effect of hard inquiries:

- Age of credit accounts: If you have many new accounts, additional inquiries might be seen more negatively.

- Utilization rates: If your existing credit cards are maxed out, and you’re seeking more credit, inquiries will be viewed with greater skepticism.

- Payment history: A stellar payment history can often buffer the negative impact of inquiries.

It’s crucial to understand that while hard inquiries do impact your score, they are generally one of the less influential factors compared to payment history (which accounts for about 35% of your FICO score) and credit utilization (about 30%). They typically account for roughly 10% of your score. Therefore, while mindful management is important, panicking over a single inquiry is usually unwarranted.

Strategic Management of Hard Inquiries

Effective management of hard inquiries is about being intentional with your credit applications. It involves planning, monitoring, and understanding how the system works to your advantage, rather than letting it detract from your financial standing.

Smart Application Practices

The most straightforward way to manage hard inquiries is to be selective and strategic about when and for what you apply for credit. Avoid applying for multiple types of credit simultaneously unless absolutely necessary. Each application for a different type of credit (e.g., a car loan and a credit card) will generally result in a separate hard inquiry and a separate score impact.

Before submitting an application:

- Assess your need: Is new credit truly necessary, or are there alternatives?

- Research eligibility: Check pre-qualification tools (which often use soft inquiries) to gauge your likelihood of approval before committing to a full application.

- Space out applications: If you anticipate needing various types of credit, try to space out your applications over several months to allow your score to recover between inquiries. For instance, avoid applying for a new credit card just before seeking a mortgage.

The Art of Rate Shopping

For major loans like mortgages, auto loans, and student loans, credit scoring models often have a built-in grace period for “rate shopping.” This allows consumers to compare offers from multiple lenders without being penalized for each inquiry. If you apply for the same type of loan multiple times within a specific window (which can range from 14 to 45 days, depending on the credit scoring model being used), these inquiries are typically treated as a single inquiry for scoring purposes. This is a critical feature that empowers consumers to seek out the best interest rates and terms without fear of damaging their credit excessively.

To maximize this benefit:

- Concentrate your shopping: Do all your rate comparisons for a specific type of loan within a tight timeframe.

- Understand the window: Be aware that the exact window can vary slightly between FICO and VantageScore models, but aiming for a 14-day window is a safe bet for most models.

Proactive Monitoring and Dispute Resolution

Regularly checking your credit report is a cornerstone of good credit management. You are entitled to a free copy of your credit report from each of the three major credit bureaus annually via AnnualCreditReport.com. Take advantage of this.

When reviewing your report, pay close attention to the “inquiries” section.

- Identify unfamiliar inquiries: Look for any hard inquiries you don’t recognize or didn’t authorize. An unauthorized inquiry could be a sign of identity theft or an error.

- Dispute errors immediately: If you find an unauthorized hard inquiry, you have the right to dispute it with the credit bureau that reported it. Provide evidence that you did not authorize the inquiry. Successfully removing an erroneous hard inquiry can restore a few points to your score and remove an unnecessary mark from your report.

The Broader Significance of Credit Inquiries

Hard inquiries are more than just numerical deductions on a score; they are a small but significant piece of the larger puzzle that forms your financial identity and future opportunities.

Your Financial Gateway

A healthy credit score, minimally affected by judicious hard inquiries, is your gateway to a vast array of financial products and services. It dictates your ability to:

- Secure loans: Access mortgages, car loans, and personal loans when you need them.

- Obtain credit cards: Open accounts with better rewards, lower interest rates, and higher credit limits.

- Rent housing: Landlords often check credit as part of the application process.

- Get better insurance rates: Some insurers use credit-based insurance scores.

- Access utility services: Often without needing a security deposit.

Each hard inquiry, therefore, represents a step you’ve taken to access these financial tools. When managed wisely, these inquiries contribute to building the credit history necessary for future financial endeavors.

Maintaining Credit Health

Ultimately, understanding what a hard inquiry is and how to manage it contributes to overall credit health. It fosters a more informed approach to borrowing and financial planning. By being intentional about your credit applications, taking advantage of rate shopping windows, and diligently monitoring your credit reports, you empower yourself to navigate the credit landscape more effectively. A thoughtful approach ensures that hard inquiries serve their purpose—to facilitate access to necessary credit—without unnecessarily detracting from the strong credit profile you’ve worked to build.