Filing taxes on time is a fundamental civic duty for most individuals and businesses. The annual tax deadline, typically in mid-April, often looms large, causing anxiety for those who haven’t yet submitted their returns. While many strive to meet this crucial deadline, life’s unpredictable nature or simple procrastination can lead to a delay. The immediate question that arises for anyone in this predicament is: “What happens if I file my taxes a day late?” The simple answer is that consequences can vary significantly depending on whether you owe the government money, if you’ve filed an extension, or if you’re due a refund. Understanding these repercussions and how to navigate them is essential to minimize financial strain and legal complications.

Understanding the Penalties for Late Filing and Payment

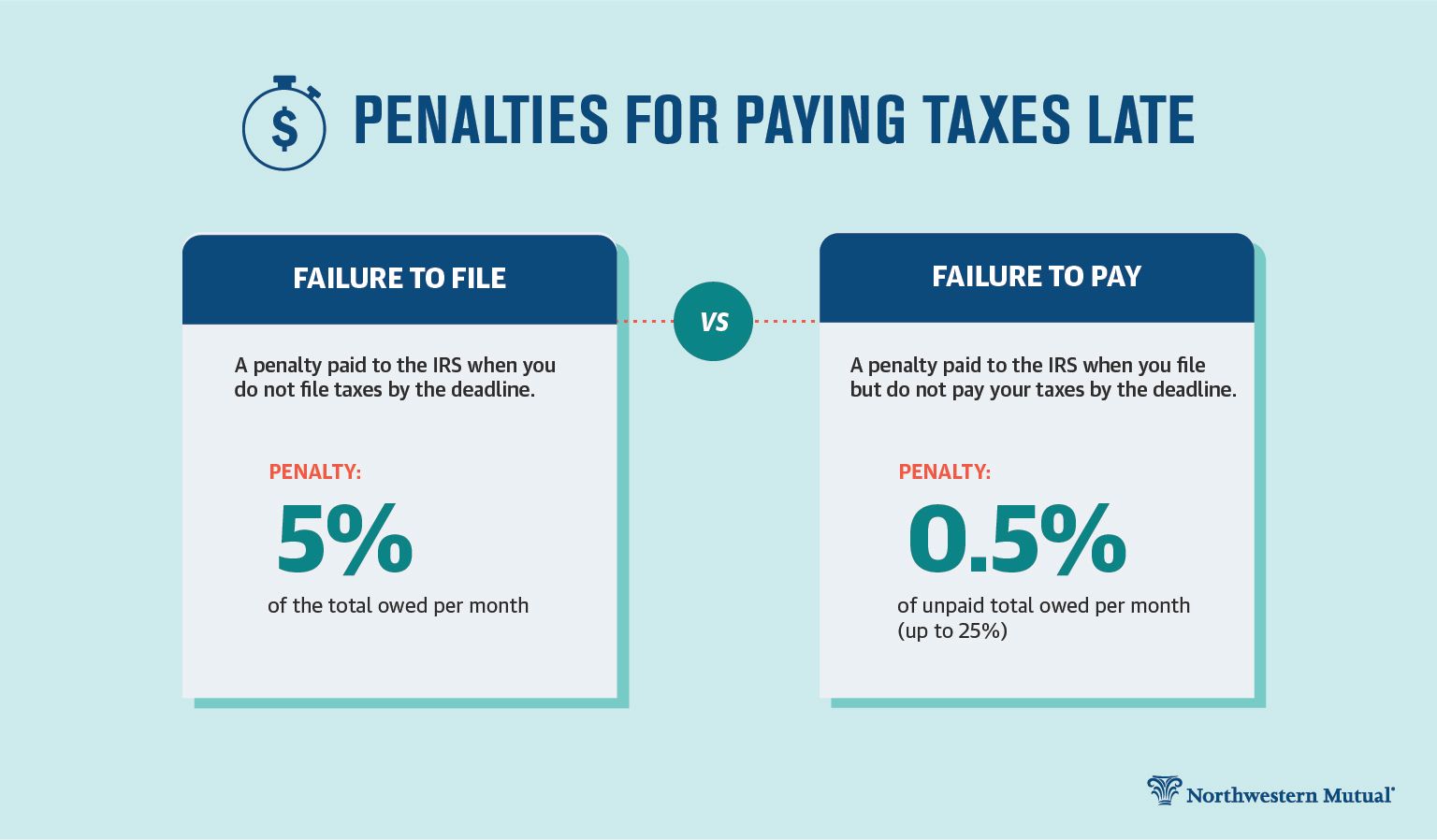

The Internal Revenue Service (IRS) is clear about the penalties associated with failing to meet tax obligations. These penalties are designed to encourage timely compliance and are generally assessed in two primary categories: failure to file and failure to pay. It’s crucial to distinguish between these, as their calculation and severity differ.

Failure-to-File Penalty

This is often the more severe of the two penalties. If you fail to file your tax return by the deadline (or extended deadline), the IRS can impose a penalty of 5% of the unpaid taxes for each month or part of a month that a tax return is late. This penalty is capped at 25% of your unpaid tax bill. Even if your return is only a day late, it counts as a full month for penalty calculation purposes.

For instance, if you owe $2,000 in taxes and file one month and one day late, the penalty would be 5% of $2,000, which is $100. This accrues monthly until you file or hit the 25% cap. If your return is more than 60 days late, the minimum penalty is either $485 (for tax returns required to be filed in 2024) or 100% of the tax due, whichever is less. This means that even if you owe very little, a significant minimum penalty could apply if you’re substantially late. The minimum penalty applies even if no tax is due. This illustrates why the failure-to-file penalty is so potent and why filing something, even if you can’t pay, is paramount.

Failure-to-Pay Penalty

Distinct from the failure-to-file penalty, the failure-to-pay penalty applies when you don’t pay the taxes you owe by the due date. This penalty is much smaller, typically 0.5% of the unpaid taxes for each month or part of a month the taxes remain unpaid. Like the failure-to-file penalty, it’s capped at 25% of your unpaid tax bill.

If both failure-to-file and failure-to-pay penalties apply in the same month, the failure-to-file penalty is reduced by the failure-to-pay penalty. This means the combined total penalty for both won’t exceed 5% per month. The failure-to-pay penalty can continue to accrue after the failure-to-file penalty has reached its maximum.

Interest Charges

Beyond the penalties, the IRS also charges interest on underpayments. This interest is applied to any unpaid tax from the original due date until the date of payment. The interest rate is determined quarterly and is typically the federal short-term rate plus 3 percentage points. While the penalties can seem substantial, the interest charges continue to accrue until the debt is fully paid, adding to the overall cost of a late filing or payment. This makes it financially prudent to resolve outstanding tax liabilities as quickly as possible. The interest rate for the second quarter of 2024, for example, is 8% for underpayments, making even small balances grow significantly over time.

What If You’re Owed a Refund?

One of the most common misconceptions about filing late revolves around refunds. Many believe that if the IRS owes them money, there are no repercussions for a late filing. While it’s true that the IRS generally does not impose a penalty for failure to file if you are due a refund, there’s a critical catch: you won’t get your refund until you actually file your return.

More importantly, there’s a strict time limit to claim your refund. The IRS generally allows taxpayers three years from the original due date of the return to claim a refund. If you fail to file within this three-year window, you forfeit your right to that refund. The money then becomes the property of the U.S. Treasury. This applies even if you are owed a substantial sum. For example, if your 2020 tax return was due in April 2021, you generally have until April 2024 to file and claim any refund. Missing this deadline means losing that money forever.

Therefore, while the immediate financial penalty might be absent, failing to file for a refund is akin to leaving money on the table. It is always advisable to file your return, regardless of whether you anticipate a payment or a refund, to ensure you claim what is rightfully yours and avoid future complications, such as potential issues with federal benefits or loan applications that require proof of filed tax returns.

Strategies to Mitigate Penalties and Interest

Even if you find yourself in a situation where you’ve filed or paid late, there are several avenues to explore for mitigating the financial impact. The IRS understands that life happens and offers certain relief options under specific circumstances.

Filing an Extension

The most straightforward way to avoid a late-filing penalty if you know you’ll miss the April deadline is to file for an extension. An extension, typically Form 4868, gives you an additional six months to file your federal income tax return, moving the deadline to mid-October. It’s crucial to understand that an extension to file is not an extension to pay. You must still estimate and pay any taxes owed by the original April deadline to avoid failure-to-pay penalties and interest. However, filing an extension effectively buys you time to gather your documents and accurately prepare your return without incurring the much steeper failure-to-file penalty. This single action can save hundreds or even thousands of dollars in penalties.

Reasonable Cause for Abatement

The IRS may abate (remove or reduce) penalties if you can demonstrate a “reasonable cause” for your failure to file or pay on time. Reasonable cause is generally defined as circumstances beyond the taxpayer’s control that prevented them from meeting their tax obligations. Examples of reasonable cause include:

- Serious Illness or Death: A serious illness or death of the taxpayer or an immediate family member.

- Natural Disaster or Casualty: A fire, casualty, natural disaster, or other disturbance that prevented the taxpayer from obtaining records or accessing a tax professional.

- Unavoidable Absence: An unavoidable absence of the taxpayer.

- Inability to Obtain Records: The inability to obtain necessary records despite reasonable efforts.

- Reliance on Erroneous Advice: Reliance on incorrect written advice from the IRS.

To request penalty abatement, you typically need to contact the IRS and explain your situation, providing supporting documentation. This request is often made using Form 843, “Claim for Refund and Request for Abatement,” or by calling the IRS directly. While the IRS considers each case individually, a well-documented and compelling argument for reasonable cause can lead to significant penalty relief. This option is not available for interest charges, as interest is compensation for the use of money and not a penalty.

Offer in Compromise (OIC) and Payment Plans

If you genuinely cannot pay your tax liability, even with penalties, the IRS offers options such as an Offer in Compromise (OIC) or an installment agreement. An OIC allows certain taxpayers to resolve their tax liability with the IRS for a lower amount than what they originally owe, but it’s typically granted only when there is significant doubt as to the taxpayer’s ability to pay the full amount due. The IRS considers your ability to pay, income, expenses, and asset equity when evaluating an OIC.

An installment agreement, on the other hand, allows you to make monthly payments for up to 72 months. While interest and penalties continue to accrue, they might be reduced, and it prevents the IRS from taking more aggressive collection actions like liens or levies. Setting up a payment plan demonstrates a good-faith effort to resolve your tax debt and is a practical solution for managing an outstanding balance.

State Tax Implications and Other Considerations

It’s important to remember that federal tax obligations are only one piece of the puzzle. Most states also have their own income tax systems, and their deadlines often mirror the federal one. Consequently, if you file your federal taxes late, you’re likely also late on your state taxes, which come with their own set of penalties and interest charges. These state-level penalties can vary widely, from relatively minor fees to significant percentages of your unpaid tax liability. Always check your state’s specific rules regarding late filing and payment.

Beyond penalties and interest, late filing can have other indirect consequences. If you are self-employed, late filing could impact your ability to qualify for certain government programs, loans, or even professional licenses that require proof of current tax compliance. It can also delay the processing of other financial applications that depend on your income and tax history.

Furthermore, repeated late filings can flag your account for increased scrutiny from the IRS. While a single late filing might be forgiven for reasonable cause, a pattern of non-compliance can lead to more aggressive enforcement actions and a reduced chance of penalty abatement in the future.

In conclusion, while filing your taxes even a day late might not seem catastrophic, it triggers a chain of events that can lead to accumulating penalties and interest. The severity of these consequences largely depends on whether you owe money or are due a refund, and whether you’ve taken proactive steps like filing an extension. The best course of action is always to file on time, or at least file for an extension if you need more time to prepare your return, ensuring that any estimated taxes are paid by the original deadline. By understanding the rules and utilizing available relief options, taxpayers can navigate the complexities of late filing and mitigate its financial impact.