In the dynamic world of technology and innovation, where groundbreaking ideas transform into market-ready products and services, the foundational decisions about a company’s legal structure are as critical as the technology itself. For many burgeoning tech ventures and established innovators alike, the choice often narrows down to two primary corporate forms: the C Corporation (C Corp) and the S Corporation (S Corp). These structures, though seemingly bureaucratic, wield significant influence over a company’s taxation, ability to raise capital, administrative burden, and overall operational flexibility. Understanding the nuances between a C Corp and an S Corp is not merely an exercise in legal compliance; it is a strategic imperative that can dictate a company’s trajectory, profitability, and eventual success in a competitive landscape driven by rapid advancement.

This comprehensive guide will delve into the definitions, characteristics, advantages, and disadvantages of both C Corporations and S Corporations, providing a clear framework for tech entrepreneurs, investors, and stakeholders to make informed decisions. As technology continues to evolve at an unprecedented pace, so too do the considerations for how these innovative companies are structured and managed.

Understanding Corporate Structures in the Tech Landscape

The legal entity selected for a tech startup or an innovative project is more than just a name on a registration form; it’s a blueprint for its future. This choice impacts everything from how profits are distributed and how losses are handled, to the ease with which external investment can be secured and the potential for a public offering. For companies operating in areas like AI, autonomous systems, advanced mapping, or remote sensing, the implications of this decision can be profound.

The Fundamental Choice for Innovators

At its core, a corporation is a legal entity distinct from its owners. This separation provides limited liability protection to its shareholders, meaning their personal assets are generally shielded from the company’s debts and liabilities. This protection is particularly vital in tech, where R&D often involves significant risk and potential for legal challenges or financial setbacks. The key distinction between C Corps and S Corps primarily lies in their taxation methods and the rules governing their ownership. While both offer limited liability, their approaches to profit distribution, investor attraction, and regulatory compliance diverge significantly.

Legal Entities and Their Strategic Implications

The strategic implications extend beyond immediate financial considerations. The chosen structure influences perception among potential investors, partners, and even employees. A C Corp, for instance, is often viewed as the standard for companies aiming for significant external funding and eventual public listing, while an S Corp might be preferred by smaller, closely held tech firms focusing on pass-through income for founders. Navigating these complexities requires a forward-looking perspective, anticipating the company’s growth trajectory, funding needs, and long-term objectives within the fast-paced tech and innovation sector.

The C Corporation: A Foundation for Growth and Investment

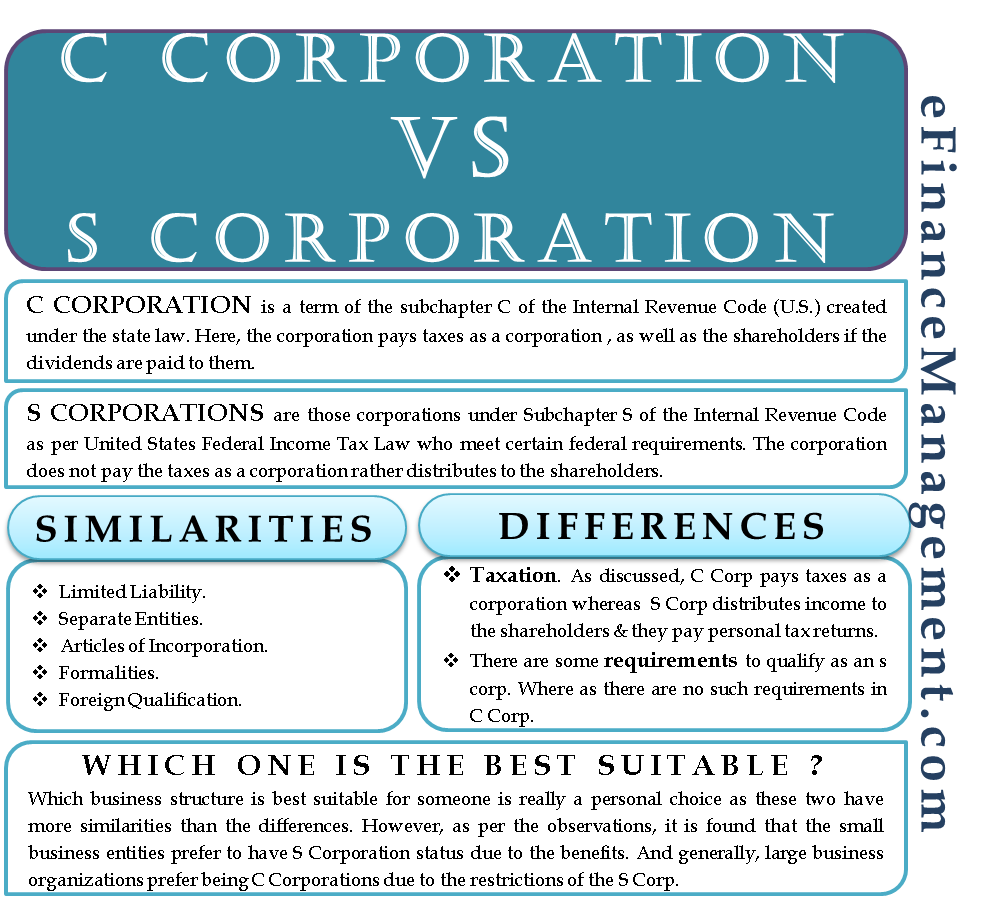

The C Corporation is the traditional and most common form of incorporation. It is the default structure when a business incorporates and does not elect S Corp status. This structure is particularly prevalent among large, publicly traded companies, but it’s also a common choice for tech startups with ambitions for rapid scaling, significant external investment, and eventual exit strategies like acquisition or initial public offering (IPO).

Taxation and Double Taxation Explained

The most defining characteristic of a C Corp is its tax structure, specifically the concept of “double taxation.” A C Corp is treated as a separate taxable entity by the Internal Revenue Service (IRS). This means the corporation pays taxes on its profits at the corporate level. Subsequently, when the corporation distributes these after-tax profits to shareholders as dividends, those shareholders pay taxes on the dividends at their individual income tax rates. This two-tiered taxation is the “double taxation” referred to. While this can seem like a disadvantage, especially for profitable companies, recent changes in corporate tax rates (e.g., the U.S. federal corporate tax rate is now a flat 21%) have somewhat mitigated its impact, making C Corps more attractive than they once were.

Attracting Venture Capital and Public Offerings

For tech companies aiming to attract substantial venture capital (VC) funding or eventually go public, the C Corp structure is often the preferred, if not mandatory, choice. VCs and other institutional investors typically invest in C Corps because it allows for multiple classes of stock (e.g., preferred stock with special rights for investors) and does not impose restrictions on the number or type of shareholders. Foreign investors, for example, cannot be shareholders in an S Corp, which is a significant limitation for globally-minded tech firms. The C Corp structure provides the flexibility and familiarity that large investors and stock exchanges require, streamlining the process of capital acquisition critical for scaling innovative technologies.

Governance and Shareholder Flexibility

C Corps offer the greatest flexibility in terms of ownership and governance. They can have an unlimited number of shareholders, and these shareholders can be individuals, other corporations, partnerships, or trusts. This allows for complex ownership structures and strategic partnerships. The corporate governance structure typically involves a board of directors overseeing management, providing a robust framework for decision-making and accountability that appeals to sophisticated investors. This flexibility is a key enabler for tech companies that foresee complex capitalization tables, employee stock option plans (ESOPs), and diverse ownership interests as they grow.

The S Corporation: Prioritizing Pass-Through Taxation

The S Corporation is a special designation granted by the IRS that allows a corporation to avoid federal income tax at the corporate level. Instead, profits and losses are “passed through” directly to the owners’ personal income tax returns, similar to a partnership or sole proprietorship. This structure is often favored by smaller, closely held tech companies or startups where founders want to manage tax burdens directly.

Avoiding Double Taxation: A Key Advantage

The primary appeal of an S Corp is the avoidance of double taxation. Corporate profits are taxed only once, at the individual shareholder level. This can lead to significant tax savings for profitable companies, as business owners can often take a reasonable salary (subject to payroll taxes) and then receive additional distributions of profits tax-free, as these profits have already been accounted for on their personal returns. For tech innovators who are also owners, this can optimize their personal tax situation and allow more capital to remain within the business or in their pockets.

Shareholder Limitations and Eligibility Requirements

However, the S Corp status comes with strict eligibility requirements and limitations on its shareholders. An S Corp can have no more than 100 shareholders, all of whom must generally be U.S. citizens or residents (with some exceptions for certain trusts and estates). Corporations, partnerships, and non-resident aliens cannot be shareholders. Furthermore, an S Corp can only issue one class of stock, although different voting rights among shares are permitted. These limitations often make the S Corp structure unsuitable for tech startups seeking significant VC funding from a diverse pool of investors, many of whom might be foreign entities or require preferred stock.

Operational Simplicity and Owner Compensation

While requiring formal corporate formalities (like maintaining corporate records, holding board meetings, etc.) similar to a C Corp, the S Corp often presents a simpler tax reporting structure for smaller operations. Owners of an S Corp who also work for the business must pay themselves a “reasonable salary” for the services they provide. This salary is subject to payroll taxes (Social Security and Medicare). Any additional profits distributed to them beyond this salary are generally not subject to self-employment taxes, providing a potential tax advantage compared to a partnership or LLC. This balance of formal structure with simplified pass-through taxation makes it an attractive option for certain tech businesses focused on immediate owner benefits.

Deciding Between C Corp and S Corp for Tech Ventures

The decision between a C Corp and an S Corp for a tech venture is a strategic one, deeply intertwined with the company’s vision, funding strategy, and long-term objectives. There is no one-size-fits-all answer, and what might be optimal for a micro-drone software developer focusing on niche applications could be entirely unsuitable for an AI company aiming for global market domination.

Growth Trajectory and Funding Needs

One of the most critical factors is the company’s expected growth trajectory and funding requirements. If a tech company anticipates needing substantial external capital from venture capitalists or institutional investors, and especially if it aims for an IPO, the C Corp structure is almost always the appropriate choice. Its flexibility with multiple classes of stock and an unlimited number of diverse shareholders is essential for these scenarios. Conversely, if a tech venture plans to be self-funded, grow organically, or rely on smaller, angel investments, and wants to minimize immediate tax burdens, an S Corp might be more appealing, provided it meets the shareholder limitations.

Tax Planning and Profit Distribution

The tax implications are another pivotal consideration. For highly profitable tech companies, especially those that plan to retain earnings for reinvestment rather than immediately distributing them as dividends, the C Corp’s lower corporate tax rate (currently 21% federal) might be advantageous. However, if the primary goal is to minimize overall tax liability for the owners and distribute profits regularly, the S Corp’s single layer of taxation often provides a superior outcome. Entrepreneurs should consult with tax professionals to model various scenarios based on projected profitability, owner compensation, and distribution plans.

Administrative Burden and Compliance

Both C Corps and S Corps require adherence to corporate formalities, including maintaining corporate records, holding annual meetings, and filing specific reports with state agencies. However, C Corps, especially as they grow and attract more investors, often face more stringent regulatory compliance and reporting requirements. While an S Corp still demands professional accounting and tax preparation, its smaller shareholder base and simpler tax structure can sometimes translate into slightly less complex administration. For lean tech startups, managing administrative overhead efficiently is key.

Beyond the Basics: Evolving Considerations for Tech Startups

The landscape for tech innovation is constantly shifting, and so too are the business considerations for structuring these ventures. Beyond the fundamental C vs. S Corp debate, entrepreneurs must also consider state-specific regulations, the potential for international expansion, and the long-term flexibility to adapt their corporate structure as needs change.

State-Specific Nuances and Global Reach

While the federal tax treatment of C Corps and S Corps is well-defined, state laws can introduce additional layers of complexity. Some states do not recognize the S Corp status for state income tax purposes, meaning an S Corp might still be subject to corporate-level taxes at the state level. For tech companies with a global vision, aiming to attract international talent or serve overseas markets, the C Corp structure generally offers more straightforward integration with international tax treaties and foreign investment laws. The limitations on foreign shareholders in S Corps can be a significant hurdle for such aspirations.

Future Planning and Conversion Potential

It’s important to remember that the initial choice of corporate structure is not necessarily permanent. A business can convert from a C Corp to an S Corp, or vice versa, if its circumstances or strategic objectives change. For example, a tech startup might initially form as an S Corp to benefit from pass-through taxation in its early, less profitable years, only to convert to a C Corp once it starts attracting significant venture capital and requires more robust capitalization flexibility. However, these conversions can involve tax implications and administrative effort, so it’s best to plan as far ahead as possible.

In conclusion, choosing between an S Corporation and a C Corporation is a pivotal decision for any tech and innovation venture. It requires careful consideration of current needs, future ambitions, tax implications, and administrative capabilities. By thoroughly understanding the distinct features and trade-offs of each structure, tech entrepreneurs can establish a robust legal and financial foundation that supports their innovation, fuels their growth, and positions them for long-term success in an ever-evolving technological frontier.