In an increasingly interconnected global economy, the seamless flow of capital across borders is not merely an advantage but a fundamental necessity. From individual remittances to large-scale corporate transactions, the ability to transfer funds internationally efficiently and securely underpins global commerce and fosters economic integration. At the heart of this complex financial ecosystem lies a seemingly simple string of alphanumeric characters: the International Bank Account Number, or IBAN. Far from being just another identifier, the IBAN represents a significant leap in financial technology and standardization, designed to streamline cross-border payments and minimize errors in an intricate global network.

The IBAN is an internationally agreed-upon system for identifying bank accounts across national borders, standardized by the European Committee for Banking Standards (ECBS) and later adopted as ISO 13616:1997. Its primary purpose is to facilitate automated processing of international payment transactions, ensuring that funds reach the correct recipient account without delay or misdirection. In an era where technological prowess dictates efficiency and reliability, understanding the IBAN is crucial for anyone engaging with international finance, highlighting the silent yet powerful innovation driving global economic interactions.

The Technological Evolution of Global Finance

The journey towards standardized international bank account identification is a testament to the persistent pursuit of technological solutions to complex logistical challenges in finance. Before the widespread adoption of the IBAN, international wire transfers were often a convoluted process, prone to manual errors, delays, and additional costs due to incomplete or incorrect account information. This inefficiency was a significant bottleneck for global commerce, hindering the very agility that modern businesses and individuals demand. The advent of the IBAN system marks a pivotal moment in the technological evolution of global finance, transitioning from fragmented national systems to a unified, internationally recognized standard.

From SWIFT to IBAN: A Journey of Standardization

The backbone of international financial communication historically has been the SWIFT (Society for Worldwide Interbank Financial Telecommunication) network. SWIFT provides a secure platform for financial institutions to send and receive information about financial transactions. Each bank on the SWIFT network has a unique identifier code, known as a BIC (Bank Identifier Code) or SWIFT code. While the SWIFT/BIC code identifies the bank, it does not specify the individual account within that bank with the same level of precision as an IBAN.

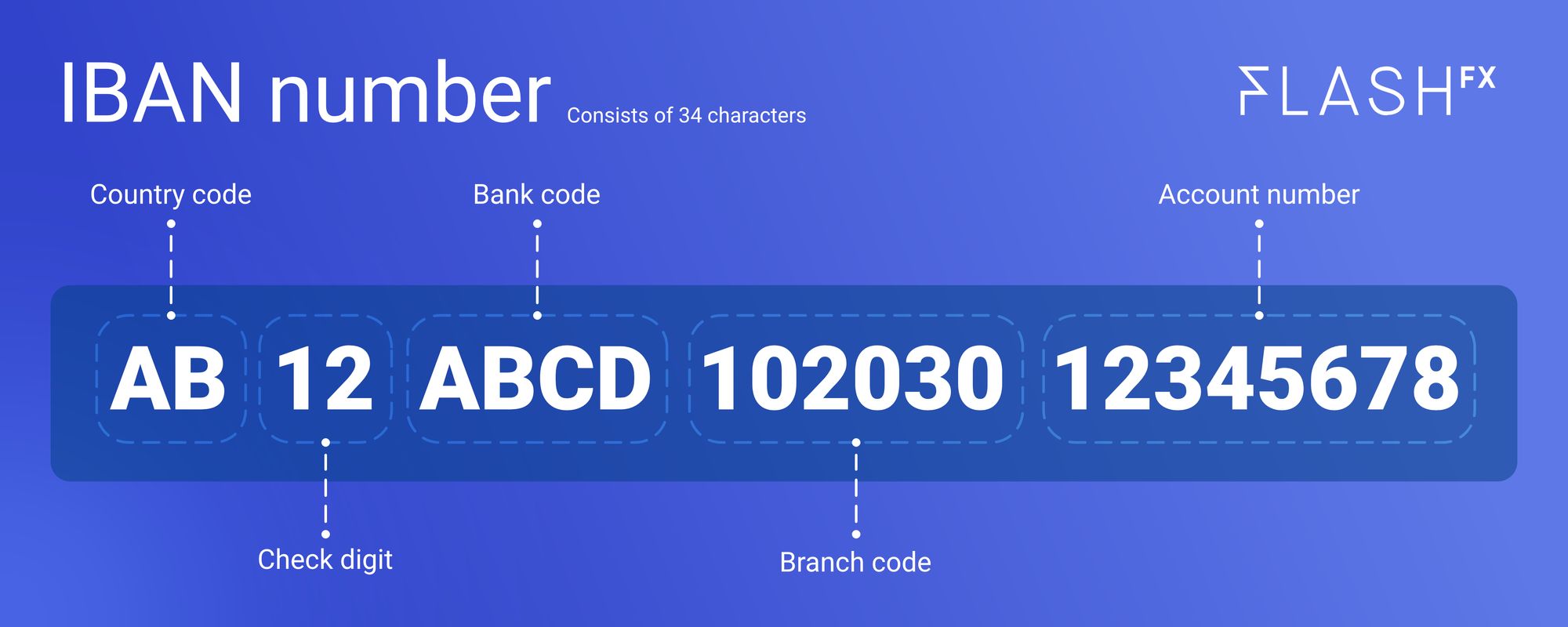

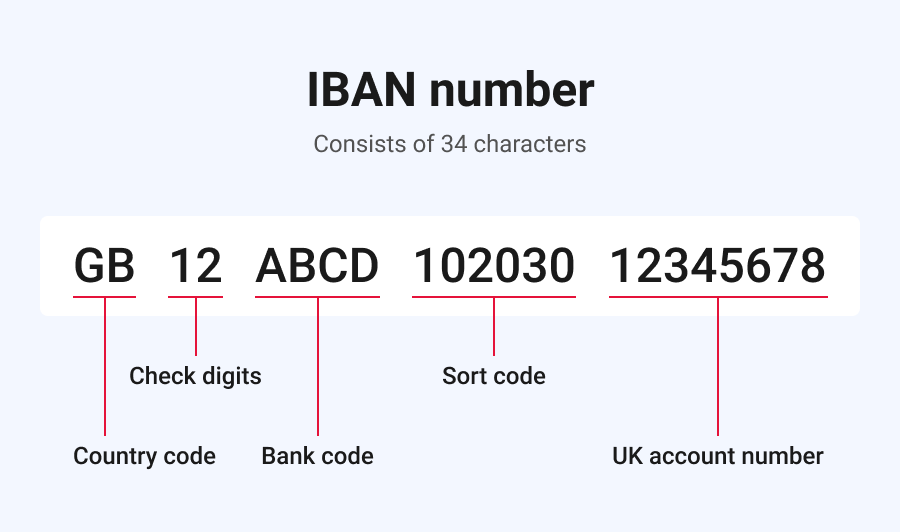

The IBAN emerged to complement the SWIFT system by standardizing the account identification itself. Originating in Europe to facilitate payments within the Single Euro Payments Area (SEPA), its benefits quickly became apparent, leading to its global adoption. The structure of an IBAN is carefully designed to contain all necessary information for identifying a specific bank account in a specific country. It begins with a two-letter country code (e.g., DE for Germany, GB for United Kingdom), followed by two check digits, and then a Basic Bank Account Number (BBAN) which is specific to each country and includes the bank code and account number. The check digits are a critical technological innovation, designed to validate the entire IBAN, acting as a safeguard against transcription errors. Before a payment is initiated, banking systems can automatically verify the IBAN’s integrity, significantly reducing the chances of misdirected funds. This automated validation process is a prime example of how digital technologies are employed to enhance the reliability and security of financial transactions.

Enhancing Efficiency and Reducing Errors

The primary technological advantage of the IBAN system lies in its ability to standardize and automate the processing of international payments. Prior to IBAN, a myriad of different national account numbering systems meant that banks had to develop complex internal systems to interpret and process various formats. This often required manual intervention, leading to higher operational costs, increased processing times, and a greater propensity for errors. A single mistyped digit could lead to funds being delayed, returned, or, in worst-case scenarios, sent to the wrong recipient, resulting in costly investigations and rectifications.

The IBAN standardizes this information into a universally recognized format, enabling straight-through processing (STP). With STP, payment instructions can be processed end-to-end without manual intervention, from initiation to settlement. This technological advancement translates into several tangible benefits:

- Reduced Error Rates: The built-in check digits allow for immediate validation, catching most common transcription errors at the point of entry.

- Faster Processing Times: Automation eliminates delays associated with manual checks and corrections, speeding up the entire payment cycle.

- Lower Transaction Costs: Reduced manual intervention and error resolution costs lead to more economical international transfers for both banks and their customers.

- Improved Transparency: A standardized format makes it easier for all parties to understand and verify payment details.

These improvements are not just minor conveniences; they represent fundamental innovations in how global financial institutions leverage technology to manage the intricate web of international money movement.

IBAN in the Digital Age: Enabling Cross-Border Innovation

The significance of the IBAN extends beyond merely standardizing account numbers; it is a foundational piece of infrastructure that enables the burgeoning digital economy and fosters innovation across various sectors. In a world increasingly reliant on digital platforms for commerce, services, and communication, the ability to make and receive international payments quickly and reliably is paramount. The IBAN system facilitates this by providing a common language for financial transactions that can be easily integrated into diverse digital applications and services.

Supporting Global E-commerce and Digital Services

The rise of global e-commerce has dramatically reshaped the retail landscape, allowing businesses to reach customers across continents and consumers to access products from around the world. For this ecosystem to thrive, efficient international payment mechanisms are essential. The IBAN plays a crucial role by simplifying the collection and disbursement of funds for online merchants, digital service providers, and gig economy workers operating internationally.

Consider a small business in Europe selling handcrafted goods to customers in the Middle East, or a freelance software developer in Asia providing services to clients in North America. In both scenarios, the IBAN streamlines the payment process, making it as straightforward as a domestic transfer within the respective IBAN-participating regions. This ease of transaction reduces friction in cross-border trade, lowering barriers for businesses to expand globally and for individuals to participate in the international digital economy. From subscription services to app purchases and digital content, the seamless financial infrastructure supported by IBANs ensures that digital goods and services can be exchanged globally with minimal financial complexity.

The Role of Fintech in Streamlining Payments

Financial technology, or FinTech, has been a driving force behind many of the innovations that have transformed how we interact with money. From mobile banking apps to peer-to-peer payment platforms and blockchain-based remittance services, FinTech aims to make financial services more accessible, efficient, and user-friendly. The IBAN, while predating many modern FinTech innovations, serves as a critical component that these new technologies often build upon or integrate with.

Many FinTech companies, especially those focusing on international payments and remittances, leverage the IBAN system to offer competitive exchange rates, lower transaction fees, and faster transfer speeds compared to traditional banking channels. By integrating IBAN validation and routing capabilities into their platforms, these innovators can provide a superior user experience, making international money transfers feel almost as easy as sending a text message. For example, neo-banks and digital payment platforms often utilize IBANs to provide users with multi-currency accounts, enabling them to hold and transfer funds in different currencies seamlessly. This technological synergy between established standards like IBAN and cutting-edge FinTech solutions is continuously pushing the boundaries of what’s possible in global financial transactions.

Security, Compliance, and Future Innovations

While the IBAN significantly enhances efficiency and reduces errors, its role in the broader landscape of financial technology also encompasses critical aspects of security and regulatory compliance. Moreover, as technology continues to evolve at an unprecedented pace, the future of international payments is poised for even more transformative innovations, potentially building upon or even moving beyond the current IBAN framework.

Mitigating Fraud and Ensuring Regulatory Adherence

Security is paramount in financial transactions. While the IBAN itself is a public identifier and does not inherently contain sensitive information like passwords, its standardized format and check-digit system contribute indirectly to security by reducing the opportunities for human error that can be exploited by fraudsters. The immediate validation of an IBAN significantly lowers the risk of funds being sent to a non-existent or incorrect account due to a typo, which could otherwise be a vector for certain types of social engineering scams or simply lost funds.

Furthermore, IBANs play a role in regulatory compliance, particularly concerning Anti-Money Laundering (AML) and Know Your Customer (KYC) regulations. Financial institutions use the IBAN in conjunction with other identifiers and sophisticated transaction monitoring systems to track the flow of funds, identify suspicious patterns, and comply with international sanctions. The structured nature of IBANs allows for easier integration with these compliance technologies, strengthening the global fight against financial crime. In an increasingly regulated financial landscape, the technological foundation provided by IBANs aids institutions in meeting their stringent legal obligations.

The Future of International Payments: Beyond IBAN

The financial technology sector is constantly evolving, with new innovations regularly emerging to challenge existing paradigms. While the IBAN has proven to be an incredibly effective and enduring standard for international account identification, discussions about the future of international payments inevitably involve exploring technologies that could further enhance efficiency, lower costs, and increase accessibility.

One area of significant innovation is blockchain technology and cryptocurrencies. Distributed ledger technology (DLT) offers the potential for near-instantaneous, borderless, and low-cost transactions, bypassing traditional banking intermediaries. Projects like stablecoins and central bank digital currencies (CBDCs) are exploring how digital currencies could fundamentally reshape international transfers. While these technologies are still maturing and face significant regulatory hurdles, they represent a potential long-term shift in how cross-border payments are executed.

Another area of development is real-time gross settlement (RTGS) systems that aim to process transactions continuously rather than in batches, leading to instant settlement. Many countries are developing or have already implemented domestic real-time payment systems, and the challenge now is to extend this real-time capability across international borders. Initiatives like the G20’s roadmap for enhancing cross-border payments aim to make international transfers cheaper, faster, more transparent, and more accessible, leveraging a combination of existing infrastructure improvements and emerging technologies.

In this dynamic landscape, the IBAN, while a testament to successful standardization and technological foresight, will likely continue to evolve. It may integrate with newer payment rails, adapt to new digital currencies, or even find its function supplemented or partially superseded by more advanced, distributed identification and transfer mechanisms. However, for the foreseeable future, the IBAN remains a cornerstone of efficient and secure international financial transactions, a robust example of how technology and standardization can drive global connectivity and economic progress. Its enduring utility underscores the power of innovation in making complex financial processes simpler, faster, and more reliable for everyone involved in the global marketplace.