Income-Based Repayment (IBR) is a student loan repayment plan that adjusts your monthly payment based on your income and family size. This can be a crucial tool for borrowers who are struggling to afford their standard monthly loan payments. By offering a payment that is proportional to what you can realistically afford, IBR aims to prevent defaults and make managing student loan debt more manageable over the long term.

The fundamental principle behind IBR is that no borrower should have to pay more than they can reasonably afford towards their student loans. This contrasts with the standard 10-year repayment plan, where monthly payments are fixed and do not change regardless of your financial circumstances. For individuals with lower incomes, high debt-to-income ratios, or unpredictable income streams, the standard plan can be an overwhelming burden. IBR provides a flexible alternative, offering a pathway to consistent repayment without jeopardizing essential living expenses.

Eligibility and Application Process

To be eligible for an Income-Based Repayment plan, borrowers must have federal student loans. Private student loans generally do not qualify for IBR. The primary federal loan programs that offer IBR are Direct Loans and FFEL Program loans. Federal Perkins Loans may also be eligible if they have been consolidated into a Direct Consolidation Loan.

The application process for IBR typically involves submitting an application to your loan servicer. This application will require you to provide information about your income and family size. You will need to document your income, usually by providing recent tax returns, pay stubs, or other proof of income. Your family size is determined by the number of people you claim as dependents on your tax return, including yourself.

The U.S. Department of Education’s Federal Student Aid (FSA) website is the central hub for information and applications related to federal student loans, including IBR. Borrowers can often start the application process online through their loan servicer’s portal or by visiting the FSA website. It’s important to have all your financial documentation readily available to ensure a smooth application process.

Documenting Your Income

Accurate income documentation is critical for IBR. The calculation of your monthly payment is directly tied to your “discretionary income,” which is the difference between your adjusted gross income (AGI) and 150% of the poverty guideline for your family size.

- Adjusted Gross Income (AGI): This is your gross income minus certain deductions. You can find your AGI on your most recent federal income tax return (Form 1040).

- Poverty Guideline: These are set annually by the U.S. Department of Health and Human Services and vary based on family size and state of residence (Alaska and Hawaii have separate guidelines).

You will typically need to provide proof of your AGI for the year in which you are applying. This can include:

- Tax Returns: Your most recent federal income tax return (e.g., Form 1040).

- Pay Stubs: Recent pay stubs if your income is variable or if you are not filing taxes as an individual.

- Other Income Documentation: If you are self-employed or have other sources of income, you may need to provide documentation such as profit and loss statements or unemployment benefits statements.

Family Size Determination

Your family size is a key factor in determining your poverty guideline. Generally, it includes:

- Yourself.

- Your spouse, if filing jointly.

- Your dependents, as claimed on your tax return.

If you are married and filing separately, your family size calculation may differ, and it’s essential to consult with your loan servicer or refer to official guidance to ensure accuracy.

How Monthly Payments are Calculated

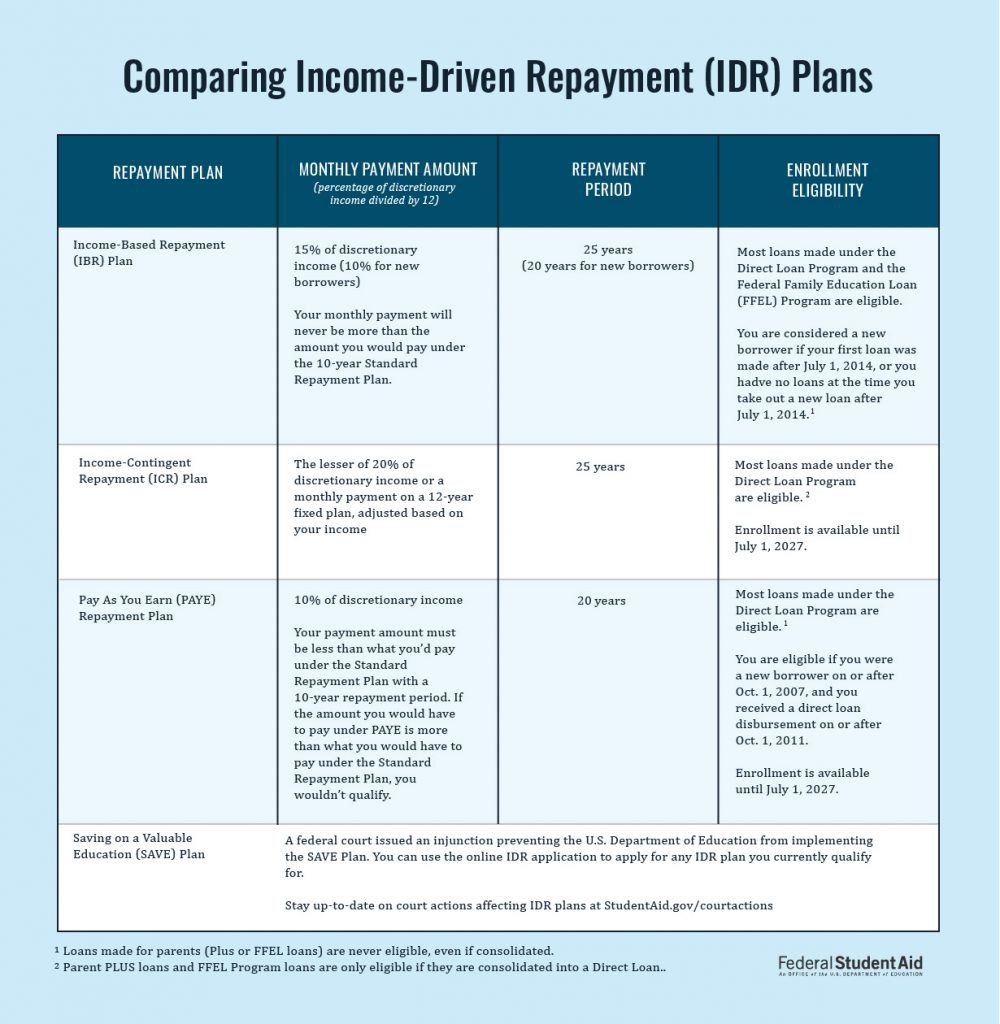

The core of the Income-Based Repayment plan is how your monthly payment is calculated. As mentioned, it’s based on your discretionary income. The IBR payment is typically set at 10% or 15% of your discretionary income, depending on when you received your first federal student loan.

- For borrowers whose first federal student loan was disbursed on or after July 1, 2014: Your IBR payment will be 10% of your discretionary income.

- For borrowers whose first federal student loan was disbursed before July 1, 2014: Your IBR payment will be 15% of your discretionary income.

The Formula in Practice:

- Determine your Adjusted Gross Income (AGI).

- Find the poverty guideline for your family size and state.

- Calculate 150% of the poverty guideline.

- Calculate your discretionary income: AGI – (150% of Poverty Guideline).

- Calculate your monthly IBR payment: (10% or 15% of Discretionary Income) / 12.

Example:

Let’s assume:

- Your AGI is $40,000.

- Your family size is 2.

- The poverty guideline for a family of 2 in your state is $22,600.

- You received your first loan after July 1, 2014, so your payment is 10% of discretionary income.

- 150% of the poverty guideline = $22,600 * 1.5 = $33,900

- Discretionary Income = $40,000 – $33,900 = $6,100

- Annual IBR Payment = 10% of $6,100 = $610

- Monthly IBR Payment = $610 / 12 = approximately $50.83

This means your monthly student loan payment would be around $50.83, significantly less than it might be under the standard repayment plan.

Loan Forgiveness and Repayment Terms

One of the most significant features of Income-Based Repayment is the potential for loan forgiveness. After making qualifying payments for a set period, the remaining balance on your federal student loans may be forgiven.

-

Repayment Period: The length of time you must make payments to be eligible for forgiveness depends on when you received your first federal student loan and your payment percentage.

- For borrowers whose first federal student loan was disbursed on or after July 1, 2014: You will make payments for 20 years.

- For borrowers whose first federal student loan was disbursed before July 1, 2014: You will make payments for 25 years.

- Note: There are also newer plans like the SAVE (Saving on a Valuable Education) plan, which offer potentially shorter forgiveness periods (e.g., 10 or 20 years depending on loan type and if the borrower received it as a new borrower). It is crucial to understand which plan applies to your loans.

-

Qualifying Payments: Not all payments count towards the forgiveness period. Generally, qualifying payments are those made under an income-driven repayment plan, including IBR, after the loan was first disbursed. Payments made under the standard repayment plan do not count. Your payments must also be made on time.

-

Forgiveness Amount: If you meet the requirements for forgiveness, the remaining balance on your federal student loans will be forgiven.

Tax Implications of Loan Forgiveness

A critical aspect to understand is the tax treatment of forgiven student loan debt. Historically, forgiven student loan debt was considered taxable income by the IRS. This meant that if you had a substantial amount of debt forgiven, you could face a significant tax bill in the year the forgiveness occurred.

However, there have been legislative changes and temporary waivers that have impacted this. For example, the American Rescue Plan Act of 2021 made student loan forgiveness tax-free through December 31, 2025. It is crucial to stay informed about current tax laws and regulations, as they can change. Always consult with a tax professional or refer to official IRS guidance for the most up-to-date information regarding the taxability of student loan forgiveness.

Pros and Cons of Income-Based Repayment

Like any financial tool, IBR has its advantages and disadvantages. Understanding these can help you determine if it’s the right option for your student loan management strategy.

Advantages of IBR:

- Reduced Monthly Payments: The most significant benefit is the potential for substantially lower monthly payments, making it easier to manage your budget and cover other essential living expenses.

- Prevents Default: By aligning payments with income, IBR helps borrowers avoid delinquency and default, which can have severe consequences for credit scores and future borrowing capabilities.

- Potential for Loan Forgiveness: The prospect of having remaining loan balances forgiven after a set period offers a long-term solution for managing overwhelming debt.

- Flexibility: Your payments can adjust annually based on changes in your income and family size, providing flexibility during periods of financial fluctuation.

Disadvantages of IBR:

- Longer Repayment Period: While offering relief, IBR plans typically extend the repayment period beyond the standard 10 years. This means you will likely pay more in total interest over the life of the loan compared to the standard plan.

- Interest Accrual: If your monthly payment does not cover the accruing interest, the unpaid interest can capitalize and be added to your principal balance. This can cause your total loan balance to grow over time, especially if your payments are very low.

- Annual Recertification: You must recertify your income and family size annually to remain on the IBR plan. Failure to do so can result in your payments reverting to the standard plan and potential capitalization of unpaid interest.

- Tax Implications of Forgiveness: As noted, forgiven debt may be considered taxable income in certain circumstances, requiring careful financial planning.

- Eligibility Restrictions: Not all federal loans qualify for IBR, and private student loans are excluded.

When to Consider Income-Based Repayment

Income-Based Repayment is a valuable option for several categories of borrowers:

- Low-Income Earners: Individuals whose current income is insufficient to comfortably manage payments under the standard 10-year plan.

- Recent Graduates with High Debt: Those who have a substantial amount of student loan debt relative to their starting salaries.

- Public Service Workers: While Public Service Loan Forgiveness (PSLF) is a separate program, IBR can be a component of managing loans while working towards PSLF eligibility, as payments made under IBR can count towards the 120 qualifying payments for PSLF.

- Borrowers with Unpredictable Income: Freelancers, self-employed individuals, or those in industries with variable income may find the flexibility of IBR beneficial.

- Individuals Facing Financial Hardship: Anyone experiencing temporary or ongoing financial difficulties that make standard loan payments unmanageable.

Before opting for IBR, it’s crucial to compare your projected payments and total interest paid under IBR versus other repayment plans, including the standard plan and other income-driven options like PAYE (Pay As You Earn) or SAVE. Your loan servicer can help you explore these options and estimate your potential payments and forgiveness amounts. Understanding the long-term financial implications is key to making an informed decision about your student loan repayment strategy.