Current Bank, a prominent player in the digital banking landscape, represents a modern approach to financial services, particularly resonating with a tech-savvy demographic that values convenience, integration, and streamlined management of their money. While not a traditional brick-and-mortar institution, its digital-first model, often built upon partnerships with established financial entities, allows it to offer a suite of services that cater to the contemporary consumer’s needs. Understanding Current Bank requires a look at its core offerings, technological underpinnings, and the innovative strategies it employs to differentiate itself in a rapidly evolving fintech market. This exploration delves into the essence of Current Bank, examining its operational framework, user experience, and its position within the broader context of digital finance.

The Foundation of Digital Banking

Current Bank operates primarily as a financial technology company, often leveraging the infrastructure of partner banks to provide its services. This model allows it to focus on user experience and feature development, while outsourcing the complex regulatory and operational aspects of traditional banking.

Partner Banks and Regulatory Compliance

The backbone of any digital bank, including Current Bank, is its relationship with licensed financial institutions. These partner banks hold the necessary charters and regulatory approvals, enabling Current Bank to offer services like FDIC-insured deposits. This partnership model is crucial for ensuring that customer funds are protected and that the bank operates within the stringent guidelines of financial regulations. Understanding this structure is key to appreciating how a digital-first entity can offer the security and legitimacy of traditional banking.

Technological Infrastructure

At its core, Current Bank is a technology platform. Its operations are driven by sophisticated software, secure data management systems, and robust payment processing capabilities. The mobile application serves as the primary interface, through which users manage accounts, make transactions, and access various financial tools. This reliance on technology allows for greater agility, faster innovation, and a more personalized user experience compared to many legacy institutions.

The “Neobank” Distinction

Current Bank is often categorized as a “neobank” or “challenger bank.” These terms refer to financial institutions that operate entirely online, without physical branches, and typically focus on delivering services through mobile apps and digital platforms. Unlike traditional banks that are gradually adopting digital features, neobanks are built from the ground up with a digital-centric philosophy. This distinction highlights Current Bank’s commitment to a modern, accessible, and often more user-friendly banking experience.

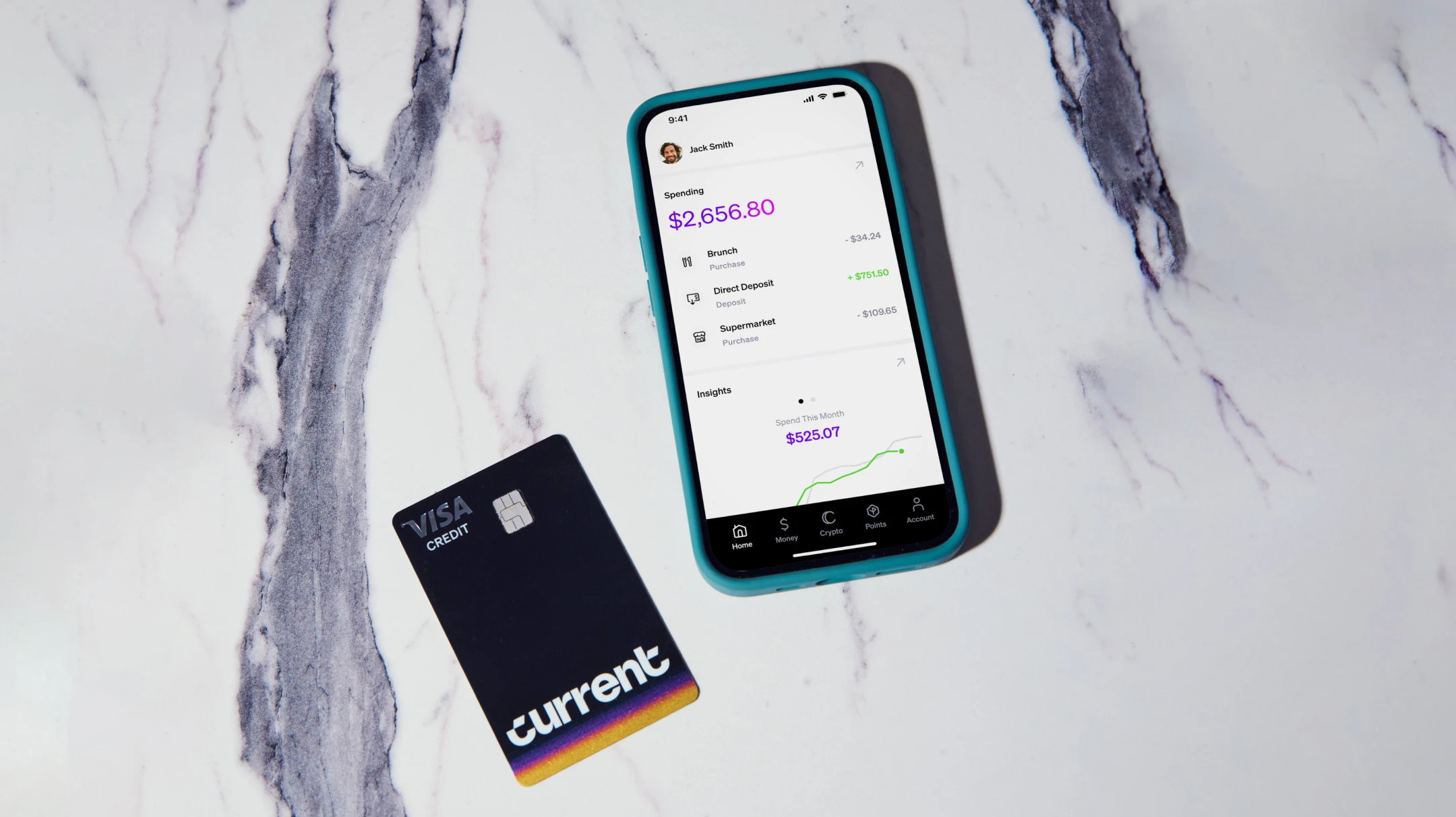

Core Services and User Experience

Current Bank distinguishes itself through a range of integrated financial services designed to simplify money management and provide tangible benefits to its users. The emphasis is on providing tools that go beyond basic checking and savings, aiming to empower users financially.

Account Offerings

The primary account offered by Current Bank is typically a checking account, often paired with a debit card. These accounts are designed for everyday use, facilitating transactions, bill payments, and direct deposits. What sets Current Bank apart is the added layer of features and benefits that complement these basic services.

Checking and Savings Features

Beyond standard account features, Current Bank often includes elements such as early direct deposit, allowing users to access their paychecks up to two days sooner. This is a common feature among neobanks, leveraging the efficiency of digital processing. Savings features may also be integrated, often allowing users to round up purchases and automatically transfer the difference into a savings pot, fostering a habit of consistent saving.

Debit Card Functionality and Rewards

The debit card is a central piece of the Current Bank experience. It functions like any other debit card for point-of-sale transactions and ATM withdrawals. However, Current Bank often enhances this by integrating loyalty programs, cashback rewards, or discounts with specific merchants. This transforms the debit card from a mere transactional tool into a value-added asset, aligning with the user’s spending habits.

Innovative Features and Financial Tools

Current Bank goes beyond traditional banking by incorporating a suite of innovative features aimed at improving financial wellness and management.

Budgeting and Spending Insights

A key differentiator for Current Bank is its emphasis on providing users with actionable insights into their spending habits. Through the app, users can often categorize transactions, set budgets, and receive personalized recommendations on how to manage their finances more effectively. This proactive approach to financial management is a significant draw for users seeking to gain better control over their money.

Peer-to-Peer Payments and Transfers

Facilitating easy money transfers is a cornerstone of modern banking, and Current Bank excels in this area. Users can typically send money to friends and family instantly within the Current platform, or to external bank accounts via standard methods like Zelle or ACH transfers. This seamless integration of payment functionalities streamlines financial interactions.

Overdraft Protection and Credit Building

Current Bank has also sought to address common pain points in traditional banking, such as overdraft fees. Depending on the specific product and user history, they may offer forms of overdraft protection, sometimes through small, interest-free advances, or by providing tools to help users avoid overdrafts altogether. Furthermore, some Current Bank products are designed to help users build credit history, offering a pathway to improved financial standing.

Investment and Cryptocurrency Access

In recent years, many neobanks, including Current, have begun to integrate investment and cryptocurrency trading functionalities directly into their platforms. This allows users to manage their banking, spending, saving, and investing all from a single app, offering an unprecedented level of convenience and accessibility to a broader range of financial activities. These integrated offerings are a testament to the evolving nature of digital finance, where the lines between different financial services are increasingly blurred.

The Technological Edge

The success of Current Bank hinges on its advanced technological infrastructure, which enables its innovative features and user-centric design. This is where the “tech” in “fintech” truly shines.

Mobile-First Design and User Interface

The Current Bank mobile application is the primary gateway to its services, and its design reflects a deep understanding of user behavior and expectations in the digital age. The interface is typically intuitive, clean, and easy to navigate, ensuring that users can manage their finances efficiently without a steep learning curve. This mobile-first approach is crucial for engaging a digitally native audience.

AI and Machine Learning Applications

Artificial intelligence and machine learning play a significant role in personalizing the user experience and enhancing the functionality of the Current Bank platform. These technologies are used to analyze spending patterns, detect fraudulent activity, provide tailored financial advice, and optimize resource allocation. For instance, AI can help in identifying unusual transactions, flagging potential scams, or suggesting personalized savings strategies based on individual spending habits.

Data Security and Encryption

Given the sensitive nature of financial data, Current Bank places a strong emphasis on data security and encryption. Robust security protocols, including multi-factor authentication, end-to-end encryption, and regular security audits, are implemented to protect user information from unauthorized access and cyber threats. The trust of users is paramount, and maintaining a secure digital environment is non-negotiable.

API Integrations and Ecosystem Building

Current Bank, like many modern fintech companies, often utilizes Application Programming Interfaces (APIs) to connect with other services and build a broader financial ecosystem. This allows for seamless integration with payment processors, investment platforms, and other third-party applications, creating a more comprehensive and interconnected financial experience for the user. This open architecture approach fosters innovation and allows for the rapid introduction of new features and services.

The Future of Digital Banking with Current Bank

Current Bank represents a significant step forward in the evolution of financial services. By blending robust financial tools with cutting-edge technology and a user-centric design, it aims to redefine how individuals interact with their money.

Addressing the Needs of the Modern Consumer

The core of Current Bank’s appeal lies in its ability to cater to the evolving needs of the modern consumer. In an era where convenience, speed, and digital integration are paramount, Current Bank offers a compelling alternative to traditional banking models. Its focus on providing a seamless, intuitive, and feature-rich experience, all accessible through a mobile device, positions it as a leader in the fintech space.

Continuous Innovation and Expansion

The fintech industry is characterized by rapid innovation, and Current Bank is committed to staying at the forefront of this evolution. Future developments are likely to include further enhancements in AI-driven financial guidance, expanded investment and trading options, deeper integrations with other lifestyle and financial apps, and potentially new product lines that cater to a wider range of financial needs. The company’s agile approach allows it to adapt quickly to market trends and emerging technologies.

The Role of Fintech in Financial Inclusion

Companies like Current Bank also play a crucial role in promoting financial inclusion. By offering accessible and affordable banking services to individuals who may be underserved by traditional banks, they democratize access to essential financial tools. The low barriers to entry, coupled with user-friendly interfaces and educational resources, empower a broader segment of the population to manage their finances more effectively and participate more fully in the digital economy. The journey of Current Bank is, therefore, not just about providing banking services, but about shaping a more inclusive and technologically advanced financial future.