Treasury stock, a concept deeply intertwined with corporate finance and shareholder equity, represents a crucial element in understanding a company’s financial health and strategic maneuvering. While the term might sound esoteric, its implications for investors, management, and the overall market are significant. Essentially, treasury stock refers to shares of a company’s own stock that it has repurchased from the open market or from shareholders. These shares are no longer outstanding, meaning they do not carry voting rights, are not eligible for dividends, and are not included in the calculation of earnings per share (EPS).

The decision for a company to repurchase its own shares is multifaceted, driven by a variety of strategic objectives. These can range from returning capital to shareholders in a tax-efficient manner to signaling confidence in the company’s future prospects. Understanding why a company chooses to buy back its stock, and how these repurchased shares are treated, is fundamental for any astute investor seeking to decipher financial statements and corporate actions.

The Mechanics of Treasury Stock

When a company decides to buy back its own shares, it can do so through several avenues. The most common is through open market purchases, where the company buys its shares on the stock exchange just like any other investor. This approach allows for flexibility, as the company can adjust the pace and volume of repurchases based on market conditions and its cash flow. Alternatively, companies may conduct a tender offer, a formal proposal to buy a specified number of shares at a fixed price, often a premium to the current market price, within a defined period. Some buybacks might also occur through private negotiations with large shareholders.

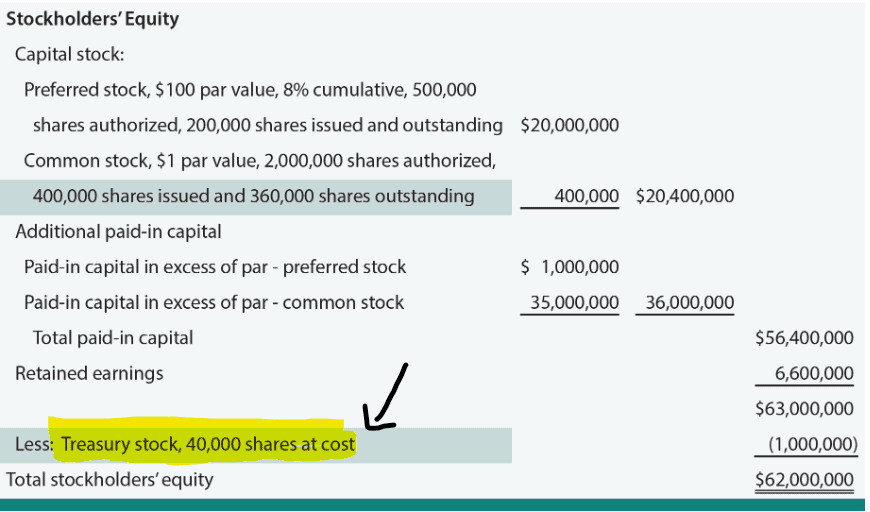

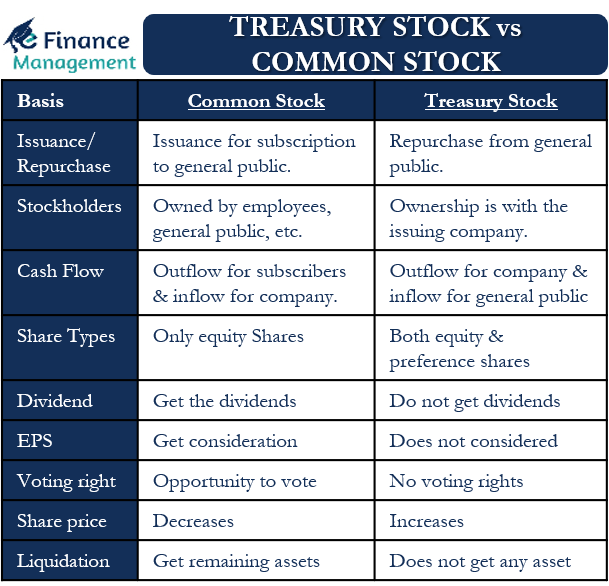

Once repurchased, these shares are no longer considered “outstanding.” This distinction is critical. Outstanding shares are those held by investors, including common stockholders and preferred stockholders, and are the basis for calculating key financial metrics. Treasury shares, by contrast, are held by the company itself. From an accounting perspective, treasury stock is typically recorded as a contra-equity account, meaning it reduces the total shareholders’ equity on the balance sheet. This is different from reacquiring shares and retiring them permanently, which would also reduce the number of authorized shares. Treasury shares can, in theory, be reissued at a later date.

Accounting Treatment of Treasury Stock

The accounting for treasury stock is generally one of two methods: the cost method or the par value method. The cost method is more common. Under the cost method, the treasury stock account is debited for the full cost of repurchasing the shares, including any brokerage fees. When the shares are later reissued, the treasury stock account is credited for the cost, and any difference between the reissue price and the cost is recorded in additional paid-in capital (APIC) or, if the reissue price is below cost, it is debited against APIC from previous treasury stock transactions or retained earnings.

The par value method, less frequently used, involves adjusting the par value of the outstanding shares and recording the repurchase at par value. Any excess paid above par is debited to APIC and retained earnings. Regardless of the method, the core principle remains that treasury stock is a reduction in equity.

Reasons for Stock Repurchases

Companies engage in stock repurchase programs for a variety of strategic and financial reasons, each aiming to enhance shareholder value or optimize the company’s capital structure.

Returning Capital to Shareholders

One of the primary motivations for repurchasing shares is to return excess cash to shareholders. While dividends are a direct way to distribute profits, stock buybacks can be a more tax-efficient method in certain jurisdictions. Unlike dividends, which are taxed as income to the recipient upon receipt, the capital gains from selling shares in a buyback are only taxed when the shareholder sells their stock, and at potentially lower capital gains rates. This flexibility allows shareholders to decide when to realize their gains, offering a more personalized approach to capital return.

Boosting Earnings Per Share (EPS)

By reducing the number of outstanding shares, a stock repurchase program automatically increases the earnings per share (EPS) calculation. EPS is a widely watched metric that reflects a company’s profitability on a per-share basis. Even if the company’s net income remains constant, a smaller number of outstanding shares will result in a higher EPS. This can make the stock appear more attractive to investors, potentially leading to an increase in its market price. While this can be a positive signal, sophisticated investors scrutinize EPS growth to ensure it’s driven by genuine operational improvements rather than solely by financial engineering.

Signaling Confidence and Undervaluation

Management’s decision to repurchase its own stock can also be interpreted as a strong signal of confidence in the company’s future prospects and its belief that the stock is undervalued by the market. When a company buys its own shares, it’s essentially betting on itself. This can reassure investors that management believes the current market price does not reflect the true worth of the company. This signal can be particularly impactful during periods of market volatility or when a company’s stock price has declined significantly without a fundamental change in its business operations.

Enhancing Shareholder Value and Financial Flexibility

Stock repurchases can also serve to increase the ownership stake of remaining shareholders. With fewer shares outstanding, each shareholder’s proportionate ownership in the company increases. This can be particularly beneficial for long-term investors. Furthermore, by reducing the number of outstanding shares and thereby the total equity, a company might also improve certain financial ratios, such as return on equity (ROE), making the company appear more efficient in its use of capital. Companies may also repurchase shares to offset the dilutive effect of employee stock options and grants, ensuring that the ownership percentage of existing shareholders is not significantly diminished.

Strategic Use of Excess Cash

Companies that generate substantial free cash flow and have limited compelling investment opportunities may choose to return that cash to shareholders through buybacks. Instead of letting cash sit idly on the balance sheet, which can be inefficient, a repurchase program provides a mechanism to deploy that capital effectively. This can also be part of a broader capital allocation strategy, balancing reinvestment in the business, debt repayment, and shareholder returns.

Impact on Investors and the Market

The presence and activity of treasury stock have tangible effects on how investors perceive and value a company, as well as broader market dynamics.

Effect on Shareholder Equity

As mentioned, treasury stock reduces total shareholders’ equity. This is a direct consequence of the company using its assets (cash) to buy back its own stock, effectively removing that equity from circulation. For investors analyzing a company’s balance sheet, it’s important to understand the magnitude of treasury stock relative to total equity and outstanding shares, as it provides insight into the company’s capital structure and its approach to shareholder returns. A significant amount of treasury stock might indicate a company that is actively managing its equity base.

Influence on Share Price and Valuation Metrics

While not guaranteed, a well-executed share repurchase program can positively influence a company’s stock price. The increased EPS, coupled with the signal of management confidence, can lead to higher investor demand. However, it’s crucial to differentiate between buybacks that genuinely create value and those that are merely aimed at artificially inflating EPS without underlying business growth. Investors often look beyond simple EPS figures and examine the quality of earnings and the sustainability of growth. Metrics like Price-to-Earnings (P/E) ratio, when considering treasury stock, should be interpreted with the understanding that the ‘E’ in P/E might be influenced by share count reduction.

Dilution and Anti-Dilution Effects

Stock repurchases are the inverse of stock issuance. When a company issues new shares, it dilutes the ownership percentage and EPS of existing shareholders. Conversely, buybacks reduce the number of outstanding shares, which is an anti-dilutive action. This is why companies often use buybacks to counteract the dilution caused by employee stock options and restricted stock units (RSUs). For employees who receive stock-based compensation, the company might repurchase shares to ensure that the total number of outstanding shares remains stable, thereby protecting the ownership stakes of existing shareholders.

Market Liquidity and Price Discovery

Open market repurchases can also contribute to market liquidity. As a company becomes a consistent buyer of its own stock, it adds to the trading volume, potentially making it easier for other investors to buy and sell shares. This can lead to a tighter bid-ask spread and a more efficient price discovery process. However, aggressive buybacks, particularly when a company is the dominant buyer, could also distort price discovery if they are not reflecting true market value.

Reissuing Treasury Stock

Companies are not obligated to hold treasury stock indefinitely. They have the option to reissue these shares back into the market. This can be done to raise capital, to fund acquisitions through stock swaps, or to provide shares for employee stock option plans. When treasury shares are reissued, they are treated as if they were newly issued shares, but the accounting treatment differs based on whether the reissue price is above or below the original repurchase cost.

If reissued above cost, the difference is typically credited to Additional Paid-In Capital (APIC). If reissued below cost, the difference is debited against APIC from previous treasury stock transactions. If APIC from treasury stock is insufficient to cover the deficit, the remaining amount is debited from Retained Earnings. This flexibility allows companies to manage their equity and capital needs dynamically.

Conclusion

Treasury stock is a fundamental concept in corporate finance, representing a company’s own shares that it has repurchased. The decision to engage in buybacks is often a strategic move, aimed at returning capital to shareholders, boosting EPS, signaling confidence, or optimizing the capital structure. For investors, understanding treasury stock is crucial for interpreting financial statements, evaluating valuation metrics, and assessing a company’s overall financial health and strategic direction. The presence of treasury stock on a balance sheet is not inherently good or bad; rather, its impact and interpretation depend on the specific context of the company, the motivations behind the buyback, and the prevailing market conditions.