The financial world, particularly as it pertains to central banking and monetary policy, often employs specific terminology that can seem arcane to the uninitiated. Among these, “excess reserves” is a concept that plays a pivotal role in the functioning of the banking system and, by extension, the broader economy. Understanding what excess reserves are, how they are formed, and their implications is crucial for anyone seeking a deeper grasp of economic stability and the tools employed to manage it.

The Foundation: Reserves in the Banking System

Before delving into excess reserves, it’s essential to understand the concept of “reserves” in banking. Banks are legally required to hold a certain percentage of their deposits in reserve. These reserves are typically held either as physical cash in their vaults or, more commonly, as balances held at the central bank (in the United States, this is the Federal Reserve).

Required Reserves: The Mandated Minimum

The primary purpose of required reserves is to ensure that banks have a baseline level of liquidity. This liquidity is intended to meet unexpected demands for cash from depositors and to facilitate the smooth clearing of payments between banks. Central banks set a “reserve requirement,” which is the minimum percentage of certain types of deposits that commercial banks must hold in reserve.

Historically, reserve requirements have been a significant tool for monetary policy. By adjusting these requirements, central banks could influence the amount of money banks had available to lend. A higher reserve requirement would mean banks had less money to lend, potentially slowing down economic activity. Conversely, a lower requirement would free up more funds for lending, potentially stimulating growth.

The Evolution of Reserve Requirements

It’s important to note that the role and prevalence of explicit reserve requirements have evolved over time and vary across jurisdictions. In many advanced economies, including the United States since March 26, 2020, reserve requirements have been set to zero percent. This shift doesn’t mean banks no longer hold reserves. Instead, it signifies a change in how central banks manage liquidity and interest rates. Even with zero percent reserve requirements, banks still hold significant balances at the central bank for operational reasons, to manage their liquidity, and to earn interest on those balances.

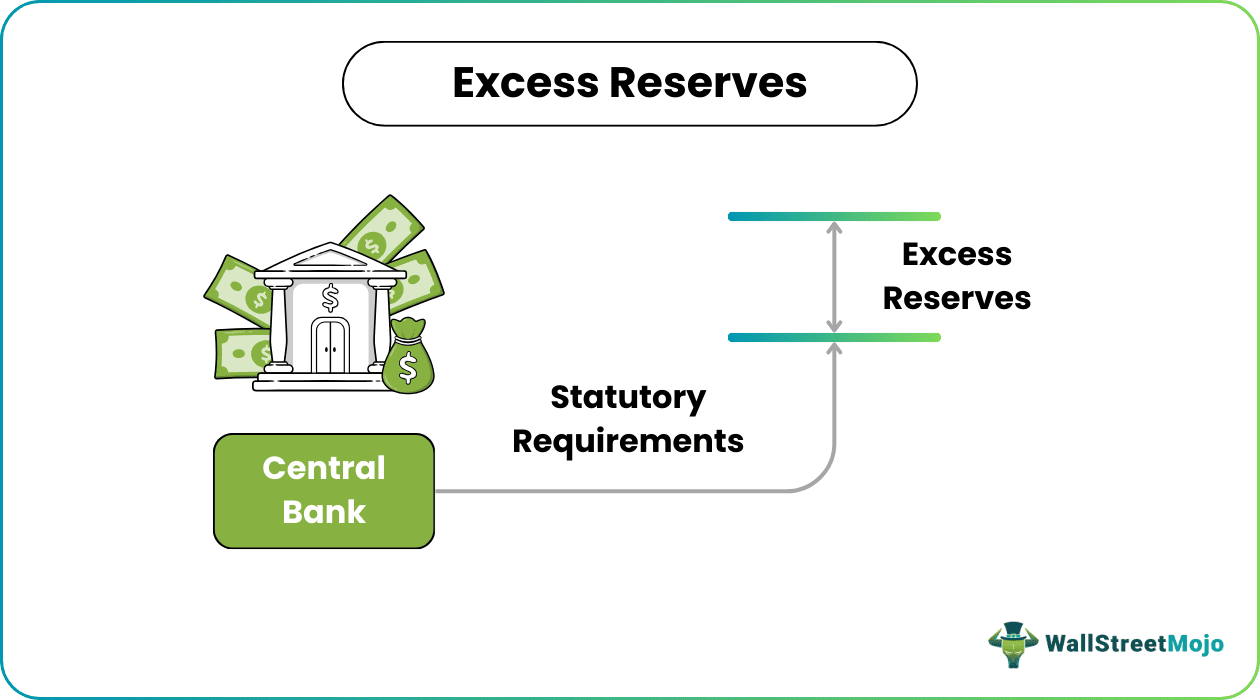

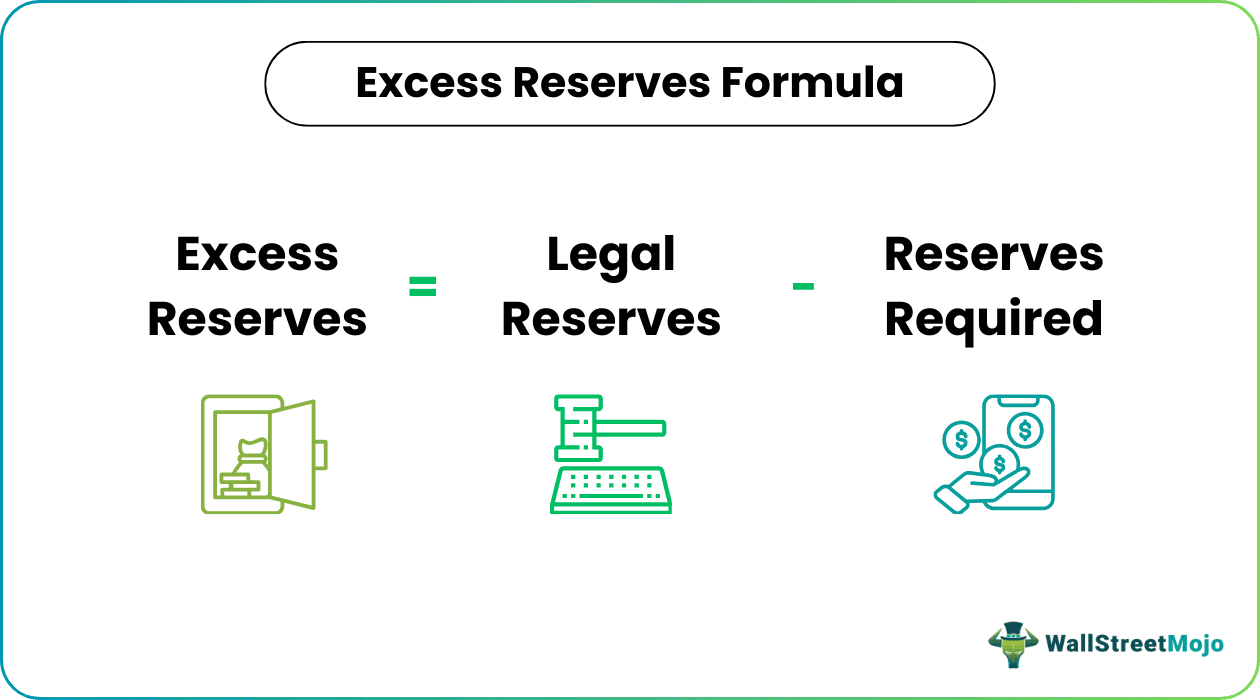

Defining Excess Reserves: The Cushion Beyond the Mandate

Excess reserves are, quite simply, the amount of reserves held by a bank that exceeds its legally required minimum. In simpler terms, if a bank is required to hold $1 million in reserves but actually holds $1.5 million, then it has $500,000 in excess reserves.

The Interplay with Zero Reserve Requirements

Given that many central banks, including the Federal Reserve, have moved to zero percent reserve requirements, the concept of “excess reserves” has taken on a slightly different nuance. When reserve requirements are zero, all reserves held by a bank at the central bank are, by definition, in excess of the requirement. Therefore, in such environments, the term “excess reserves” effectively refers to the total balances that commercial banks hold at the central bank, beyond any operational needs for physical cash.

Why Do Banks Hold Reserves (Even When Not Required)?

Even without a formal mandate, banks have several compelling reasons to hold reserves at the central bank:

- Interest on Reserves (IOR): Central banks often pay interest on reserves held by commercial banks. This “Interest on Reserve Balances” (IORB) rate, as it’s known in the US, provides a safe and profitable avenue for banks to park their funds. The central bank uses the IORB rate as a primary tool to influence short-term interest rates in the economy. By adjusting the IORB, the central bank can steer market rates towards its target.

- Liquidity Management: Banks operate with a constant flow of deposits and withdrawals. Holding ample reserves, even if not legally mandated, provides a critical buffer to meet unexpected surges in withdrawals or to facilitate large outgoing payments without needing to scramble for liquidity in the market, which can be costly.

- Regulatory Capital Requirements: While distinct from reserve requirements, banks are also subject to various capital adequacy ratios. Holding reserves can sometimes contribute indirectly to meeting these requirements and demonstrating financial soundness to regulators.

- Payment System Operations: Banks use their balances at the central bank to settle transactions with other banks and to clear checks. Maintaining sufficient balances is essential for the smooth functioning of the national payment system.

The Significance of Excess Reserves in Monetary Policy

The level of excess reserves in the banking system is a crucial indicator of monetary policy effectiveness and overall financial conditions. Its significance lies in its direct impact on the money supply, credit availability, and interest rates.

Impact on Money Supply and Lending

Traditionally, when banks held significant required reserves, an increase in excess reserves (often through open market operations by the central bank, where the central bank buys government securities from banks, injecting cash into the system) would theoretically enable them to lend more. This increased lending would expand the money supply, stimulating economic activity.

However, in an environment with zero reserve requirements and ample excess reserves, the traditional money multiplier effect is less pronounced. Banks’ lending decisions are now more directly influenced by factors such as:

- Creditworthiness of Borrowers: Banks will only lend if they find creditworthy borrowers and are comfortable with the associated risk.

- Economic Outlook: During periods of economic uncertainty, banks may be more hesitant to lend, even if they have abundant reserves.

- Regulatory Environment: Capital requirements and other regulations can influence a bank’s willingness and ability to extend credit.

- Profitability: Banks lend to make profits. If lending opportunities are not sufficiently profitable or carry excessive risk, they may choose to hold onto their reserves.

The Interest Rate Channel

The primary mechanism through which excess reserves influence the economy today is through interest rates, specifically short-term interbank lending rates.

- Federal Funds Rate: In the US, the Federal Reserve targets the federal funds rate, which is the rate at which banks lend reserves to each other overnight. When the banking system has abundant excess reserves, banks have little incentive to borrow from each other at a rate significantly above the IORB, as they can earn that rate risk-free by holding reserves at the Fed. This abundance of liquidity tends to push the federal funds rate down towards the IORB.

- The IORB as a Floor (or Near-Floor): The IORB rate acts as a powerful tool. Banks are generally unwilling to lend reserves in the federal funds market at a rate below what they can earn risk-free at the central bank. Therefore, the IORB effectively sets a floor, or at least a strong gravitational pull, for the federal funds rate.

- Quantitative Easing and Large Excess Reserves: Periods of quantitative easing (QE), where central banks purchase large quantities of assets, have significantly increased the level of excess reserves in the banking system. This has made the interest rate channel, particularly the IORB, the dominant mechanism for monetary policy implementation, rather than reserve requirements.

Factors Affecting the Level of Excess Reserves

The amount of excess reserves in the banking system is not static. It fluctuates based on several factors:

- Central Bank Operations: Open market operations, changes in the discount rate, and lending facilities by the central bank directly impact the level of reserves. QE, as mentioned, is a major driver of higher excess reserves.

- Demand for Currency: If the public withdraws more physical cash from banks, banks will need to replenish their vault cash, potentially drawing down their reserves at the central bank.

- Growth in Deposits: As the economy grows and deposits increase, banks may choose to hold more reserves as a precautionary measure or to meet potential future lending demand.

- Economic Conditions and Risk Appetite: During times of economic stress or uncertainty, banks might hoard reserves as a safe haven, increasing excess reserves. Conversely, in robust economic times, banks might deploy more of their reserves into lending and investments.

- Central Bank’s Management of Reserves: Central banks actively manage the supply of reserves to steer short-term interest rates towards their target. They conduct operations to either add reserves to the system (e.g., through asset purchases) or drain them (e.g., through asset sales or offering term deposits).

The Implications of Ample Excess Reserves

The shift towards an environment characterized by abundant excess reserves has profound implications for how monetary policy operates and how financial markets function.

Reduced Sensitivity to Reserve Requirements

The practical irrelevance of explicit reserve requirements means that central banks can no longer directly influence lending by simply adjusting the percentage of deposits banks must hold. The focus has shifted entirely to managing the overall supply of reserves and setting the interest rate on those reserves.

The Dominance of Interest Rate Policy

The primary tool for influencing economic activity becomes the central bank’s control over short-term interest rates, particularly through the IORB. By setting this rate, the central bank influences the cost of borrowing and the incentive for banks to lend or hold reserves.

Potential for Financial Instability (Under Stress)

While ample reserves generally promote liquidity, an overly large and concentrated amount of reserves held by a few very large institutions could, in extreme scenarios, pose systemic risks. However, this is generally mitigated by robust prudential regulation and supervision. The concern is more about the potential for liquidity crunches if banks become overly reliant on interbank borrowing or if the central bank’s reserve management is miscalculated, though this is rare.

The “Pushing on a String” Analogy

In an environment of very low interest rates and abundant liquidity, monetary policy can sometimes be described as “pushing on a string.” This means that while the central bank can make it very easy and cheap to borrow money (by lowering rates and providing ample reserves), it cannot force businesses and individuals to borrow or spend if they are not inclined to do so due to lack of confidence or other economic headwinds. Banks may be flush with reserves but unwilling to lend if they perceive too much risk or insufficient demand.

Conclusion: Excess Reserves as a Modern Monetary Policy Lever

In conclusion, excess reserves, once a direct constraint on bank lending through mandated requirements, have evolved into a key element of modern central banking strategy. In an environment where explicit reserve requirements are often set at zero, the concept of excess reserves essentially encompasses the total balances banks hold at the central bank. These reserves are not merely idle balances; they are crucial for liquidity management, payment system operations, and, most importantly, they are the foundation upon which central banks implement monetary policy through interest rate control. Understanding the dynamics of excess reserves is therefore fundamental to comprehending the mechanisms that influence credit availability, economic growth, and price stability in today’s financial landscape.