When it comes to saving for retirement, understanding the different account types available is crucial for making informed financial decisions. For many individuals, especially those employed by non-profit organizations or public educational institutions, the distinction between a 401(k) and a 403(b) plan can be a source of confusion. While both are tax-advantaged retirement savings accounts designed to help individuals build wealth for their golden years, they cater to different employment sectors and possess unique characteristics. This article aims to demystify these retirement vehicles, outlining their similarities and highlighting their key differences to empower individuals in navigating their retirement planning journey.

Understanding the Fundamentals: Tax-Advantaged Retirement Accounts

At their core, both 401(k) and 403(b) plans are employer-sponsored retirement savings vehicles that offer significant tax benefits. The primary advantage lies in the way contributions and earnings are taxed.

Pre-Tax Contributions and Tax Deferral

The most common feature of both plans is the pre-tax nature of contributions. This means that the money you contribute to your 401(k) or 403(b) is deducted from your gross income before federal and state income taxes are calculated. This immediate tax break reduces your current taxable income, potentially lowering your tax bill for the year.

Furthermore, the earnings within these accounts, whether from interest, dividends, or capital gains, grow on a tax-deferred basis. You do not pay any taxes on this growth year after year. Taxes are only due when you withdraw the money in retirement, at which point it is typically taxed at your ordinary income tax rate. This tax deferral allows your investments to compound more effectively over time, as your entire investment balance, including earnings, continues to grow without being diminished by annual taxes.

Roth Options: Post-Tax Contributions

In recent years, many 401(k) and 403(b) plans have begun offering a “Roth” option. With a Roth 401(k) or Roth 403(b), contributions are made with after-tax dollars. While you don’t receive an immediate tax deduction in the present, qualified withdrawals in retirement are tax-free. This can be a significant advantage if you anticipate being in a higher tax bracket in retirement than you are currently. The decision between a traditional pre-tax contribution and a Roth after-tax contribution often depends on an individual’s current income, expected future income, and tax situation.

Key Differentiators: Who Offers What?

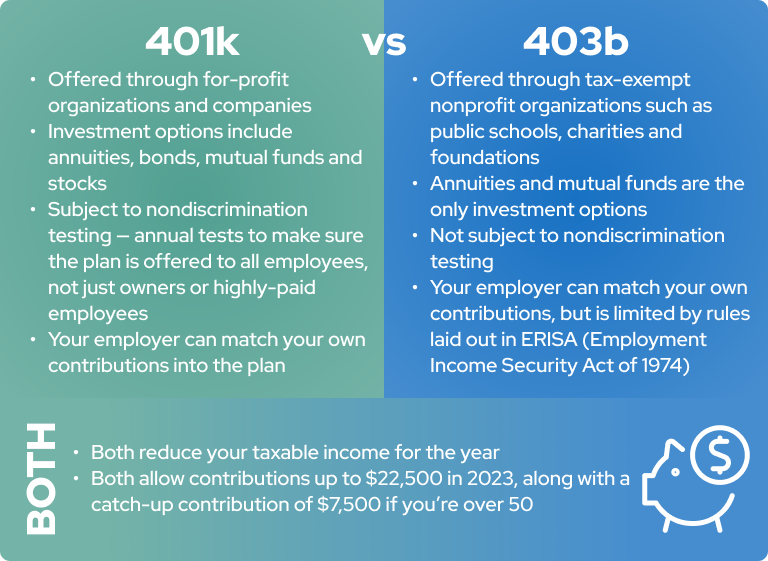

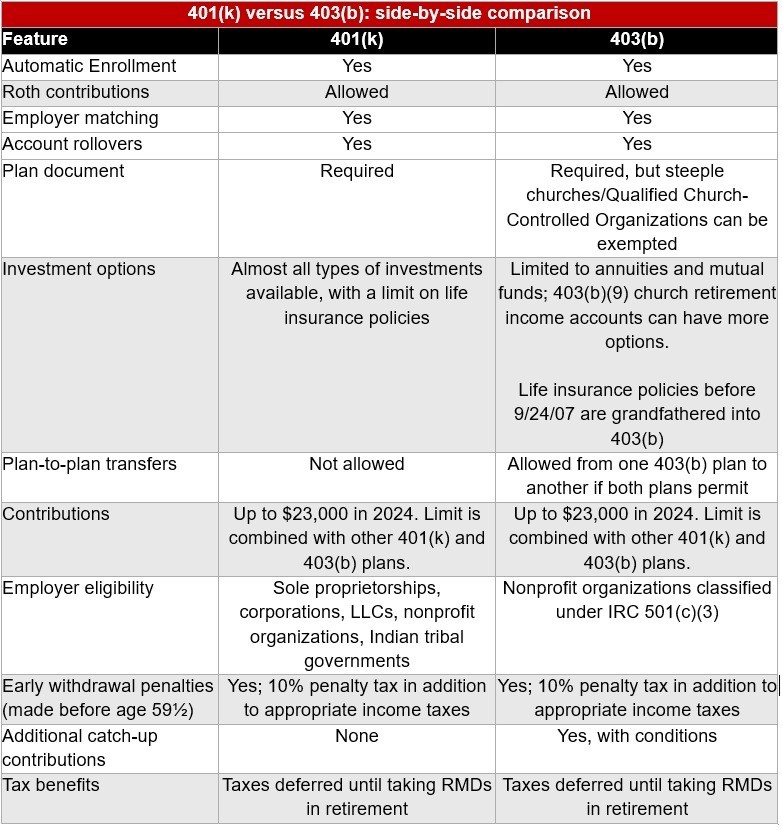

The most significant and fundamental difference between 401(k) and 403(b) plans lies in the types of organizations that are eligible to offer them. This distinction directly impacts the employee base that can benefit from each plan.

401(k) Plans: The Domain of For-Profit Businesses

The 401(k) plan, named after a section of the Internal Revenue Code, is primarily offered by for-profit companies. These are the retirement plans that most individuals associate with the private sector. If you work for a publicly traded corporation, a privately held business, or a sole proprietorship that has employees, there’s a high likelihood that a 401(k) plan is available to you. Employers use 401(k)s as a valuable tool for attracting and retaining talent, offering employees a structured way to save for retirement.

403(b) Plans: For Public Service and Non-Profits

In contrast, 403(b) plans, also known as tax-sheltered annuities (TSAs), are specifically designed for employees of certain tax-exempt organizations. These typically include:

- Public educational institutions: This encompasses teachers, administrators, and staff in K-12 school districts, colleges, and universities.

- Non-profit organizations: This includes charities, religious organizations, hospitals, and other entities classified as 501(c)(3) organizations.

- Certain research institutions and governmental entities.

The purpose behind offering 403(b) plans to these sectors is to provide a similar retirement savings benefit to employees who might not be working for traditional for-profit businesses.

Investment Options and Plan Administration

While the eligibility criteria are a primary differentiator, there are also subtle, yet important, differences in how these plans are administered and the types of investments typically available.

401(k) Investment Landscape

401(k) plans generally offer a broad array of investment options, often including:

- Mutual Funds: These are pooled investment vehicles that allow you to diversify across stocks, bonds, or other securities. 401(k) plans often feature a selection of actively managed and index mutual funds.

- Exchange-Traded Funds (ETFs): Similar to mutual funds, ETFs are baskets of securities, but they trade on stock exchanges like individual stocks.

- Company Stock: Some for-profit employers allow employees to invest in their own company’s stock, which can offer potential for growth but also concentrates risk.

- Stable Value Funds: These are low-risk, conservative investment options that aim to preserve capital and provide a predictable rate of return.

The administration of 401(k) plans is typically handled by third-party recordkeepers and investment management firms. Employers select these providers to manage the plan’s assets, process contributions, and handle participant services.

403(b) Investment Landscape and Historical Differences

Historically, 403(b) plans were often characterized by a more limited selection of investment options, primarily annuities offered by insurance companies. Annuities can offer guaranteed income streams in retirement but may come with higher fees and less flexibility compared to mutual funds.

However, over time, the investment landscape for 403(b) plans has evolved significantly. Many 403(b) plans now offer a much broader range of investment choices, including a variety of mutual funds that closely mirror the options found in 401(k) plans. Despite this convergence, it’s still common to find that some 403(b) plans may have a greater emphasis on annuity products or a more curated selection of mutual funds compared to the open architecture often seen in larger 401(k) plans.

Plan Administration and Compliance

Both 401(k) and 403(b) plans are subject to regulation under the Employee Retirement Income Security Act (ERISA) for most private employers, which sets minimum standards for retirement plans. However, 403(b) plans offered by governmental entities and certain religious organizations may be exempt from some ERISA requirements. This can sometimes lead to differences in fiduciary responsibilities and reporting obligations for the plan sponsors.

Contribution Limits and Withdrawal Rules

When it comes to saving, the amount you can contribute and when you can access your funds are critical considerations. Fortunately, for the most part, the limits and rules are very similar for both plan types.

Annual Contribution Limits

The Internal Revenue Service (IRS) sets annual limits on how much individuals can contribute to their retirement accounts. For both 401(k) and 403(b) plans, these limits are generally the same. These limits are adjusted periodically for inflation.

- Employee Elective Deferral Limit: This is the maximum amount an employee can contribute from their own salary.

- Catch-Up Contributions: For individuals aged 50 and over, there’s an additional “catch-up” contribution allowed, which increases the amount they can save for retirement in their later working years.

It’s important to note that these limits apply to the sum of employee contributions to all of your 401(k) and 403(b) plans. If you have multiple retirement accounts, you must ensure your total contributions do not exceed the IRS limits.

Employer Contributions

Employers can also contribute to both types of plans, often in the form of matching contributions or profit-sharing contributions.

- Employer Match: Many employers will match a portion of their employees’ contributions, effectively providing “free money” towards retirement. This is a powerful incentive for employees to save.

- Profit Sharing: Some employers, particularly in the 401(k) space, may make discretionary profit-sharing contributions to employee accounts, regardless of whether the employee contributes themselves.

The rules and generosity of employer contributions can vary significantly from one employer to another, regardless of whether it’s a 401(k) or 403(b) plan.

Withdrawal Rules and Penalties

Both 401(k) and 403(b) plans generally adhere to similar withdrawal rules.

- Early Withdrawal Penalty: Withdrawals made before age 59½ are typically subject to a 10% early withdrawal penalty from the IRS, in addition to ordinary income taxes on the withdrawn amount. There are some exceptions to this penalty, such as for permanent disability or certain medical expenses.

- Required Minimum Distributions (RMDs): Once you reach a certain age (currently 73, scheduled to rise to 75), you are generally required to start taking minimum distributions from your retirement accounts, whether they are 401(k)s or 403(b)s. These RMDs are taxed as ordinary income.

- Loans: Many 401(k) and 403(b) plans allow participants to take loans against their vested balance. While this can provide access to funds in an emergency, it’s crucial to understand the terms and repayment obligations, as failing to repay a loan can result in taxes and penalties.

Navigating Your Retirement Savings

Understanding the nuances between 401(k) and 403(b) plans empowers you to make the most of your retirement savings opportunities.

Making Informed Decisions

If you are offered a 401(k) or 403(b) plan, it’s essential to:

- Understand your employer’s match: If your employer offers a match, contribute at least enough to get the full match. This is essentially a guaranteed return on your investment.

- Review your investment options: Familiarize yourself with the investment choices available in your plan. Consider your risk tolerance, time horizon, and financial goals when selecting your investments. Look at expense ratios, fund performance, and diversification.

- Consider Roth vs. Traditional: If both options are available, weigh the benefits of an immediate tax deduction versus tax-free withdrawals in retirement.

- Monitor your account: Periodically review your account balance, investment performance, and contribution levels to ensure you are on track for your retirement goals.

Seeking Professional Advice

While this article provides a general overview, individual circumstances can vary greatly. If you have complex financial situations or are unsure about the best course of action for your retirement planning, consulting with a qualified financial advisor is highly recommended. They can help you understand the specifics of your employer’s plan, choose appropriate investments, and develop a comprehensive retirement strategy tailored to your unique needs.

In conclusion, while the terms 401(k) and 403(b) might sound similar, and their functional purposes are aligned, their key differentiator lies in the type of employer offering them. Both serve as powerful tools for long-term wealth accumulation, offering significant tax advantages that can help individuals build a secure and comfortable retirement. By understanding these differences and the underlying principles of tax-advantaged retirement saving, individuals can confidently navigate their options and take proactive steps toward achieving their financial future.