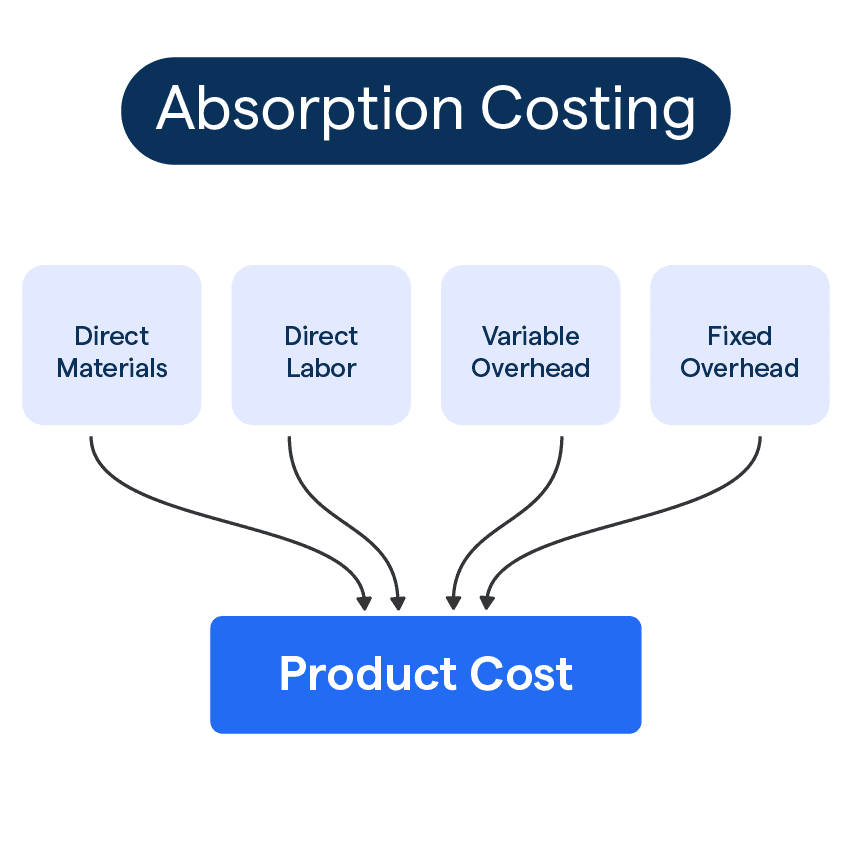

Absorption costing, also known as full costing, is a fundamental accounting method used by businesses to determine the profitability of their products and services. It stands in contrast to variable costing (or direct costing) by treating all manufacturing costs, both fixed and variable, as product costs. This means that these costs are “absorbed” into the cost of each unit produced and are only recognized as an expense on the income statement when the product is sold. Understanding absorption costing is crucial for accurate financial reporting, inventory valuation, and informed decision-making within a manufacturing environment.

The Core Principles of Absorption Costing

At its heart, absorption costing adheres to the principle that all costs incurred in the manufacturing process are necessary for the creation of a product. Therefore, these costs should be allocated to the units produced. This broad inclusion of costs distinguishes it from other costing methods.

Variable Costs

Variable costs are those that fluctuate directly with the level of production. For every unit manufactured, a certain amount of these costs is incurred. Under absorption costing, all variable manufacturing costs are assigned to the product. These typically include:

- Direct Materials: The raw materials that become an integral part of the finished product. For example, the wood in a chair, the steel in a car, or the flour in a loaf of bread.

- Direct Labor: The wages paid to workers who directly assemble or manufacture the product. This includes assembly line workers, machine operators directly involved in production, and quality control personnel focused on the physical product.

- Variable Manufacturing Overhead: Indirect costs associated with manufacturing that vary with production volume. This can include:

- Indirect materials: Lubricants for machinery, cleaning supplies for the factory floor.

- Indirect labor: Supervisors of the production line, maintenance staff for manufacturing equipment.

- Utilities: Electricity and water consumed by the manufacturing machinery and factory.

- Supplies: Small items used in the production process that aren’t direct materials, such as packaging materials for components.

Fixed Costs

Fixed costs, unlike variable costs, remain relatively constant regardless of the production volume over a relevant range. Under absorption costing, fixed manufacturing overhead costs are also allocated to the product. This is a key differentiator from variable costing. Examples of fixed manufacturing overhead include:

- Factory Rent or Mortgage Payments: The cost of occupying the manufacturing facility.

- Depreciation of Manufacturing Equipment: The cost of using machinery over time.

- Salaries of Factory Supervisors and Management: The compensation for personnel overseeing the entire production process, whose salaries don’t typically change with minor fluctuations in output.

- Property Taxes on the Factory: Taxes levied on the manufacturing facility.

- Insurance on the Factory and Equipment: Premiums paid for coverage of the manufacturing assets.

The rationale behind allocating fixed manufacturing overhead to products is that these costs are necessary for the capacity to produce. Even if a factory is not operating at full capacity, these costs are incurred to maintain that capacity. By spreading these costs over all units produced, the cost per unit reflects the full cost of making that unit available.

How Absorption Costing Works in Practice

The process of absorption costing involves several steps to allocate these costs to individual units.

Calculating the Cost Per Unit

The fundamental goal is to arrive at a cost per unit that encompasses all manufacturing expenditures.

-

Sum Total Manufacturing Costs: First, all direct materials, direct labor, variable manufacturing overhead, and fixed manufacturing overhead incurred during a period are totaled.

-

Determine Production Volume: The total number of units produced during that same period is identified.

-

Allocate Fixed Manufacturing Overhead: This is the most complex step. Fixed manufacturing overhead is typically allocated using a predetermined overhead rate. This rate is calculated before the period begins based on estimated costs and a planned activity level (e.g., estimated machine hours, direct labor hours, or units produced). The formula for the predetermined overhead rate is:

Predetermined Overhead Rate = Estimated Total Fixed Manufacturing Overhead / Estimated Activity Base

The “activity base” is a measure that is expected to drive overhead costs. Common activity bases include:

- Direct labor hours

- Machine hours

- Units produced

-

Apply Fixed Overhead to Production: Once the predetermined overhead rate is established, it is applied to the actual activity level achieved during the period.

Applied Fixed Manufacturing Overhead = Predetermined Overhead Rate × Actual Activity Base Used

-

Calculate Total Cost Per Unit: The total cost per unit is then calculated by summing the direct materials cost per unit, direct labor cost per unit, variable manufacturing overhead cost per unit, and the allocated fixed manufacturing overhead cost per unit.

Cost Per Unit = Direct Materials Per Unit + Direct Labor Per Unit + Variable Manufacturing Overhead Per Unit + Allocated Fixed Manufacturing Overhead Per Unit

Inventory Valuation

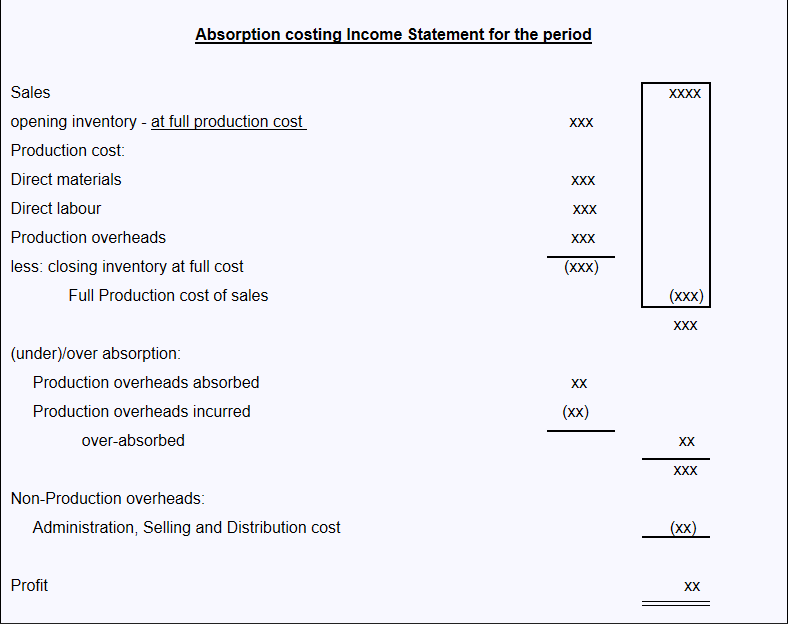

A significant implication of absorption costing is its impact on inventory valuation. Since both fixed and variable manufacturing costs are treated as product costs, they are included in the cost of finished goods inventory. This means that the value of inventory on the balance sheet will be higher under absorption costing compared to variable costing, as it includes a portion of fixed manufacturing overhead.

When units are sold, their full cost (including allocated fixed overhead) is transferred from inventory to Cost of Goods Sold (COGS) on the income statement. If units remain in inventory at the end of an accounting period, the cost associated with those unsold units, including their share of fixed manufacturing overhead, remains on the balance sheet as inventory.

Advantages of Absorption Costing

Absorption costing, despite its complexities, offers several benefits to businesses.

Financial Reporting Compliance

One of the primary advantages is that absorption costing is required for external financial reporting under Generally Accepted Accounting Principles (GAAP) in the United States and International Financial Reporting Standards (IFRS) globally. This is because these standards require that inventory be valued at its full cost, including all manufacturing costs. Using absorption costing ensures that financial statements are compliant with these reporting requirements, making them acceptable to external stakeholders such as investors and creditors.

More Accurate Product Costing for Pricing

By including all manufacturing costs, absorption costing provides a more complete picture of the cost to produce a unit. This comprehensive cost can be a valuable input for setting long-term pricing strategies. When a company understands the full cost of producing a product, including the fixed costs that must be covered, it can set prices that ensure not only the recovery of variable costs but also contribute to covering fixed costs and generating a profit.

Prevents Understating Inventory

Understating inventory can lead to misleading financial statements. Absorption costing ensures that all legitimate manufacturing costs are assigned to inventory, preventing the artificial inflation of profits in periods of high production and low sales. This leads to a more conservative and realistic valuation of assets on the balance sheet.

Aligns with the Matching Principle

The matching principle in accounting dictates that expenses should be recognized in the same period as the revenues they help to generate. Absorption costing aligns with this principle by matching the full cost of production, including fixed manufacturing overhead, with the revenue generated from the sale of those products. When a product is sold, its entire manufacturing cost is expensed; when it remains in inventory, its cost is deferred.

Disadvantages of Absorption Costing

While beneficial, absorption costing also has its drawbacks, particularly for internal decision-making.

Potential for Misleading Profitability Analysis

A significant criticism of absorption costing is that it can distort profitability analysis, especially in short-term decision-making. When production levels exceed sales levels, a portion of fixed manufacturing overhead is deferred in ending inventory. This can artificially inflate operating income in that period, as less fixed overhead is expensed through COGS. Conversely, when sales exceed production, fixed overhead from prior periods held in beginning inventory is released into COGS, potentially depressing operating income. This fluctuation can make it difficult to assess the true operational performance of the business based solely on reported profits.

Incentive to Overproduce

Because fixed manufacturing overhead is allocated to each unit produced, increasing production volume can lead to a lower cost per unit (as the fixed costs are spread over more units) and higher reported net income (due to deferring more fixed overhead in inventory). This can create an incentive for managers to overproduce units, even if they are not immediately needed, simply to manipulate reported profits and inventory values. This practice can lead to excess inventory, increased storage costs, and potential obsolescence.

Difficulty in Short-Term Decision Making

For decisions like accepting a special order, setting a specific price for a short-term promotion, or evaluating the profitability of a particular product line in the short run, absorption costing can be less helpful than variable costing. It obscures the true incremental cost of producing an additional unit, which is primarily composed of variable costs. Managers relying solely on absorption cost per unit might make suboptimal decisions because they are not seeing the direct marginal cost associated with a specific action.

Ignores Non-Manufacturing Costs

Absorption costing strictly focuses on manufacturing costs. Selling and administrative expenses, while crucial to a company’s overall profitability, are treated as period costs and are expensed in the period they are incurred, regardless of production or sales volume. This separation can sometimes make it harder to get a complete picture of the total cost of getting a product to the customer and realizing revenue.

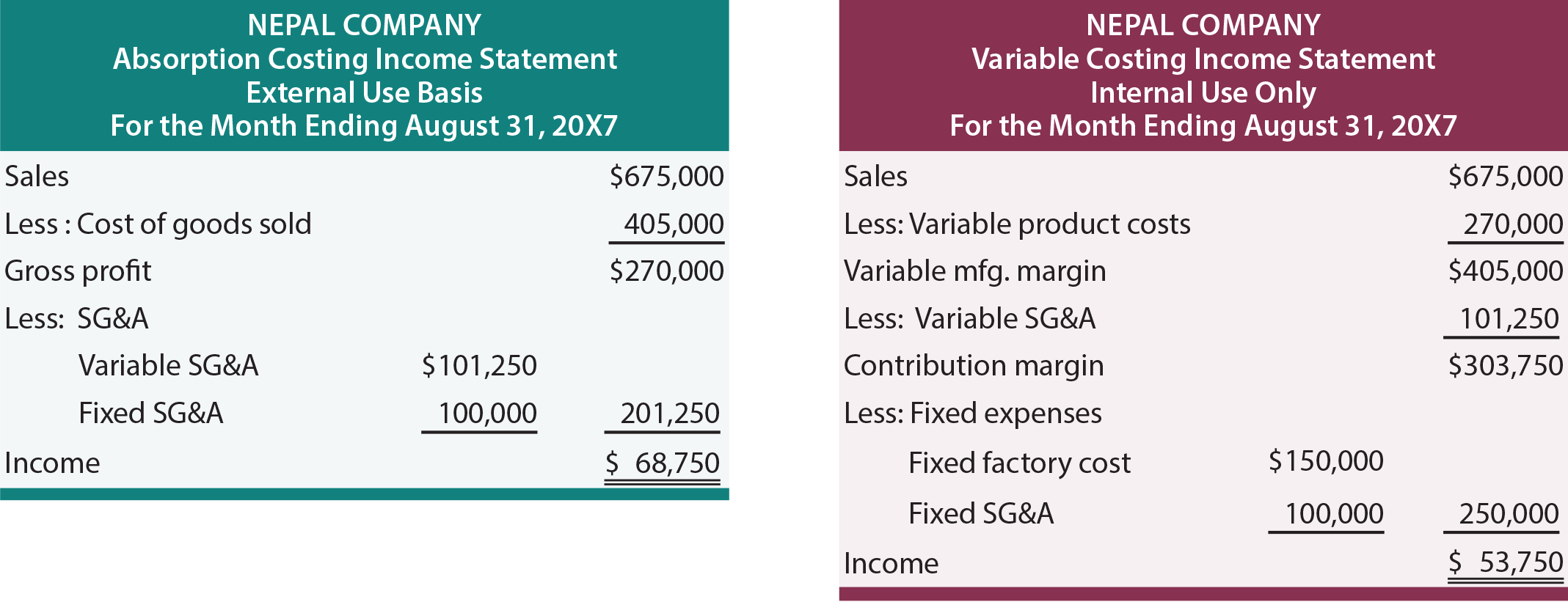

Absorption Costing vs. Variable Costing

The fundamental difference between absorption costing and variable costing lies in the treatment of fixed manufacturing overhead.

- Absorption Costing: Treats fixed manufacturing overhead as a product cost.

- Variable Costing: Treats fixed manufacturing overhead as a period cost, expensing it in the period it is incurred.

This leads to key distinctions:

| Feature | Absorption Costing | Variable Costing |

|---|---|---|

| Fixed MOH Treatment | Product Cost (included in inventory) | Period Cost (expensed when incurred) |

| Inventory Valuation | Higher (includes fixed MOH) | Lower (excludes fixed MOH) |

| Profitability | Can fluctuate with production levels | Primarily driven by sales volume |

| External Reporting | Required (GAAP/IFRS) | Not permitted |

| Internal Decision | Less useful for short-term, incremental decisions | More useful for short-term, incremental decisions |

While variable costing is valuable for internal analysis and decision-making, absorption costing remains the standard for external reporting due to its adherence to the matching principle and its comprehensive valuation of inventory.

Conclusion

Absorption costing is a vital accounting methodology that ensures all manufacturing costs are accounted for in the cost of each unit produced. Its requirement for external financial reporting makes it indispensable for accurate reporting to stakeholders. However, businesses must be aware of its potential limitations for internal decision-making, particularly concerning short-term choices and the potential incentive for overproduction. A comprehensive understanding of both absorption costing and variable costing allows businesses to leverage the strengths of each for robust financial management and strategic advantage.