Owner’s equity, a fundamental concept in accounting and finance, represents the residual interest in the assets of an entity after deducting all its liabilities. In simpler terms, it’s what the owners of a business truly “own” – the portion of the company’s value that isn’t owed to creditors or other third parties. This concept is crucial for understanding a company’s financial health, its ability to fund operations, and its overall worth. For investors, creditors, and even the business owners themselves, a clear grasp of owner’s equity is indispensable for making informed decisions.

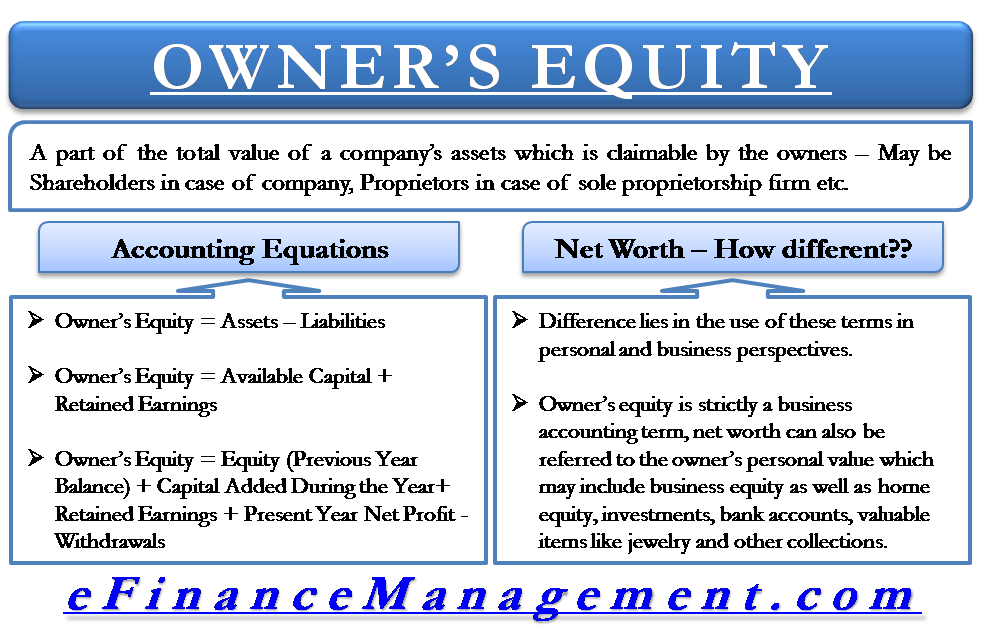

The accounting equation is the bedrock upon which owner’s equity is built: Assets = Liabilities + Owner’s Equity. This equation demonstrates the relationship between what a company owns (assets), what it owes to others (liabilities), and what is left for the owners (equity). Rearranging this equation, we can see that Owner’s Equity = Assets – Liabilities. This highlights that equity is the residual claim on the company’s assets. If a company were to liquidate all its assets and pay off all its debts, the remaining amount would belong to the owners.

Understanding owner’s equity is not just about a single number; it’s about the components that make it up and how it changes over time. Fluctuations in owner’s equity can signal various aspects of a company’s performance, such as profitability, the success of new investments, or the impact of shareholder distributions.

Components of Owner’s Equity

Owner’s equity is not a monolithic figure. It is typically comprised of several key components that provide a more detailed picture of the owners’ stake in the business. The specific accounts that constitute owner’s equity can vary depending on the legal structure of the business (sole proprietorship, partnership, or corporation), but the underlying principle remains the same.

Paid-in Capital

Paid-in capital represents the funds that owners have directly invested in the business in exchange for ownership stakes. This is often the initial infusion of capital when a business is formed or subsequent investments made by the owners.

- Common Stock (for Corporations): In a corporation, owners (shareholders) purchase shares of common stock. The par value of these shares, multiplied by the number of shares issued, constitutes the common stock account. Par value is an arbitrary nominal value assigned to a share of stock, often very low, and doesn’t reflect the market value.

- Preferred Stock (for Corporations): Preferred stock represents another class of ownership with certain preferential rights, often related to dividends and asset distribution in case of liquidation. The value of preferred stock issued is also part of paid-in capital.

- Additional Paid-in Capital (APIC) / Paid-in Capital in Excess of Par (for Corporations): When stock is issued for a price higher than its par value, the excess amount is recorded in the APIC account. For instance, if a company issues stock with a $1 par value for $10 per share, $1 would go to common stock, and $9 would go to APIC.

- Owner Contributions (for Sole Proprietorships and Partnerships): In simpler business structures, owner contributions are directly recorded in an equity account such as “Owner’s Capital” or “Partner’s Capital.”

Retained Earnings

Retained earnings represent the accumulated profits of a business that have not been distributed to owners as dividends. These profits are reinvested back into the business, allowing it to grow, expand operations, or pay down debt.

- Net Income: A company’s profitability over a period is the primary driver of retained earnings. Positive net income increases retained earnings, while net losses decrease them. Net income is calculated as revenues minus expenses.

- Dividends: When a company distributes a portion of its profits to shareholders, typically in the form of cash or additional shares, these distributions reduce retained earnings. Dividends can be declared by the board of directors and represent a payout to the owners.

- Prior Period Adjustments: Occasionally, errors made in previous accounting periods are discovered and corrected. These adjustments can impact retained earnings.

Treasury Stock (Contra-Equity Account)

Treasury stock represents shares of a company’s own stock that it has repurchased from the open market. These shares are no longer outstanding and do not carry voting rights or entitle the holder to dividends. Because treasury stock reduces the total equity of the company, it is considered a contra-equity account, meaning it has a debit balance and reduces total owner’s equity. Companies may repurchase their stock for various reasons, including to boost earnings per share, to have shares available for employee stock options, or if management believes the stock is undervalued.

Other Comprehensive Income (OCI)

Other Comprehensive Income (OCI) includes certain unrealized gains and losses that are not recognized in the income statement but are reported in a separate section of the statement of comprehensive income. These items bypass net income but still affect total owner’s equity. Examples of OCI items include:

- Unrealized gains or losses on available-for-sale securities.

- Foreign currency translation adjustments.

- Gains or losses from hedging activities.

Importance of Owner’s Equity

The significance of owner’s equity extends across various stakeholders and aspects of business management. It provides a vital snapshot of a company’s financial structure and its ability to generate value for its owners.

Financial Health and Solvency

Owner’s equity is a key indicator of a company’s financial health and its long-term solvency. A healthy and growing owner’s equity suggests that the business is profitable and capable of generating returns for its investors. Conversely, a declining or negative owner’s equity can be a warning sign, indicating that the company may be experiencing financial difficulties, losses, or an unsustainable level of debt.

A strong equity base provides a cushion against unexpected losses or economic downturns. It signifies that the company has a substantial buffer before its liabilities exceed its assets, which is a critical factor for creditors assessing creditworthiness.

Investment and Growth

For investors, owner’s equity is a primary metric for evaluating potential investments. The level of owner’s equity, particularly when analyzed in conjunction with other financial ratios, helps investors gauge the value of their stake and the company’s potential for future growth.

- Return on Equity (ROE): This profitability ratio, calculated as Net Income / Average Owner’s Equity, measures how effectively a company is using its shareholders’ equity to generate profits. A higher ROE generally indicates better performance.

- Book Value Per Share: This is calculated as Total Owner’s Equity / Number of Outstanding Shares. It represents the theoretical value of each share of stock based on the company’s balance sheet.

Operational Management

For business owners and management, understanding and managing owner’s equity is critical for strategic decision-making.

- Financing Decisions: The level of owner’s equity influences a company’s ability to secure debt financing. A higher equity ratio (equity to debt) generally makes a company more attractive to lenders.

- Dividend Policy: Decisions about retaining earnings versus distributing dividends are directly tied to owner’s equity. Management must balance the need to reinvest in the business with the desire to provide returns to shareholders.

- Performance Evaluation: Tracking changes in owner’s equity over time provides insights into the effectiveness of business strategies and operational performance. Increases in equity driven by retained earnings reflect successful profitability, while increases from new capital injections may signal expansion plans.

Valuation

Owner’s equity serves as a basis for business valuation. While market-based valuations often differ from book value (equity on the balance sheet), equity provides a fundamental starting point. In mergers and acquisitions, the equity component of a target company is a critical consideration.

Owner’s Equity in Different Business Structures

The presentation and specific accounts within owner’s equity can differ based on the legal structure of the business.

Sole Proprietorships

In a sole proprietorship, owner’s equity is typically represented by a single “Owner’s Capital” account. This account reflects the owner’s initial investment and all subsequent net income less any withdrawals (drawings) made by the owner. There are no separate shareholders or complex capital structures.

Partnerships

Partnerships have a more complex equity structure, with each partner having their own “Partner’s Capital” account. These accounts track each partner’s initial investment, their share of the partnership’s net income or loss, and any drawings taken by the individual partner. The partnership agreement dictates how profits and losses are allocated among partners, which directly impacts their individual capital accounts.

Corporations

Corporations have the most complex owner’s equity section, reflecting the separation of ownership and management. As discussed earlier, this typically includes:

- Paid-in Capital: Common stock, preferred stock, and additional paid-in capital.

- Retained Earnings: Accumulated profits less dividends.

- Treasury Stock: Repurchased shares.

- Accumulated Other Comprehensive Income: Unrealized gains and losses.

The complexity of corporate owner’s equity is a consequence of the legal framework and the diverse ways in which capital can be raised and distributed in a publicly traded or privately held corporation.

Conclusion

Owner’s equity is a cornerstone of financial accounting, offering a clear and concise measure of the owners’ stake in a business. It is derived from the fundamental accounting equation and is composed of various components, including paid-in capital and retained earnings, with variations depending on the business structure. Understanding owner’s equity is not merely an academic exercise; it is a practical necessity for assessing financial health, making informed investment decisions, guiding operational management, and determining business valuation. As businesses evolve and their financial landscapes shift, monitoring and analyzing owner’s equity provides critical insights into their stability, profitability, and the long-term value created for their owners.