The Annual Percentage Rate (APR) on a credit card is a fundamental metric that significantly impacts the overall cost of borrowing money. For consumers, understanding what constitutes a “good” APR is crucial for managing debt effectively, minimizing interest charges, and making informed decisions when choosing a credit card. This article delves into the nuances of credit card APRs, exploring the factors that influence them, the average rates, and strategies for securing a favorable APR.

Understanding the Anatomy of a Credit Card APR

An APR represents the yearly cost of borrowing money on a credit card, expressed as a percentage. It’s important to distinguish APR from the simple interest rate, as APR typically includes certain fees, such as an annual fee or origination fee, that are factored into the overall cost of credit. However, for most credit card transactions, the APR primarily dictates the interest charged on any balance carried over from month to month.

Several components contribute to the APR on a credit card:

The Prime Rate Influence

The most significant external factor influencing credit card APRs is the U.S. prime rate. This is a benchmark interest rate published by The Wall Street Journal, typically set by major banks. When the Federal Reserve adjusts its target for the federal funds rate, commercial banks often adjust their prime rates in response. Most credit card APRs are structured as a “variable rate,” meaning they are tied to the prime rate plus a margin. For instance, a credit card might have an APR of Prime Rate + 15%. Therefore, as the prime rate rises, so will the APR on your credit card, and vice versa. This makes it essential to monitor economic indicators and Federal Reserve policy when assessing your credit card’s interest rate.

Creditworthiness and Risk Assessment

An issuer’s assessment of your creditworthiness is the primary internal factor determining your APR. Lenders use your credit history, including your credit score, payment history, credit utilization, and length of credit history, to gauge the risk associated with lending you money.

- Credit Score: A higher credit score (generally above 700) indicates a lower risk to lenders, often resulting in access to cards with lower APRs. Conversely, a lower credit score suggests a higher risk, leading to higher APRs.

- Credit History: A long history of responsible credit management, including consistent on-time payments and low credit utilization, signals reliability and can help secure a better APR.

- Income and Debt-to-Income Ratio: While not as direct as credit score, lenders may also consider your income and existing debt burden to assess your ability to repay. A lower debt-to-income ratio generally suggests a stronger financial position.

Types of APRs

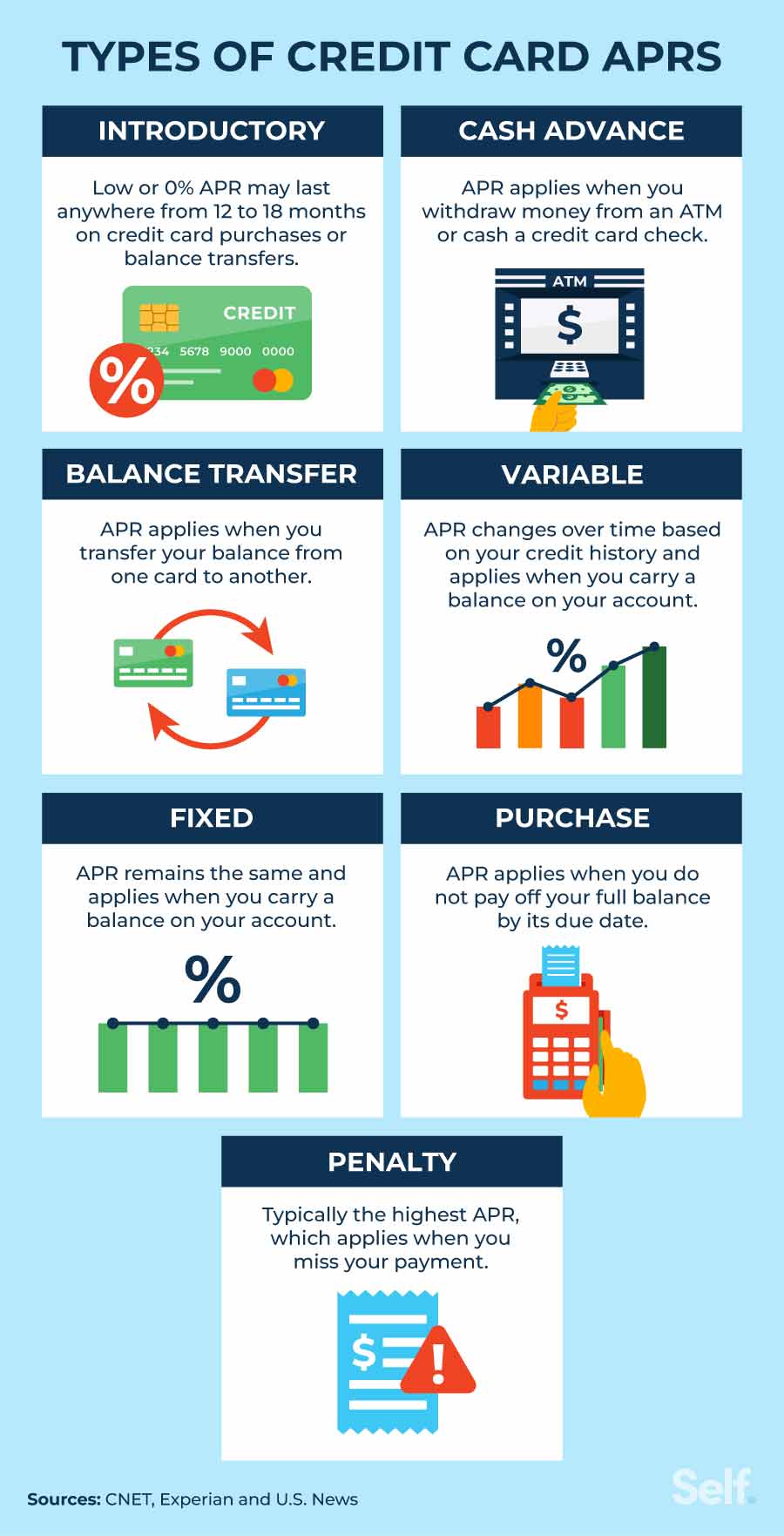

It’s crucial to recognize that credit cards often feature multiple APRs, each applying to different types of transactions or balances.

- Purchase APR: This is the most common APR and applies to purchases made with your credit card.

- Balance Transfer APR: This APR applies to balances you transfer from another credit card. These often come with introductory 0% APR periods, but revert to a higher rate afterward.

- Cash Advance APR: Cash advances are typically subject to significantly higher APRs than purchases, and interest often begins accruing immediately with no grace period.

- Penalty APR: If you miss a payment or violate other terms of your cardholder agreement, your APR can increase dramatically to a penalty APR. This rate can be very high and remain in effect for an extended period.

- Introductory APR: Many cards offer a promotional 0% or low introductory APR for a limited time on purchases and/or balance transfers. This is a significant benefit for short-term financing needs but requires careful attention to the expiration date.

What Constitutes a “Good” Credit Card APR?

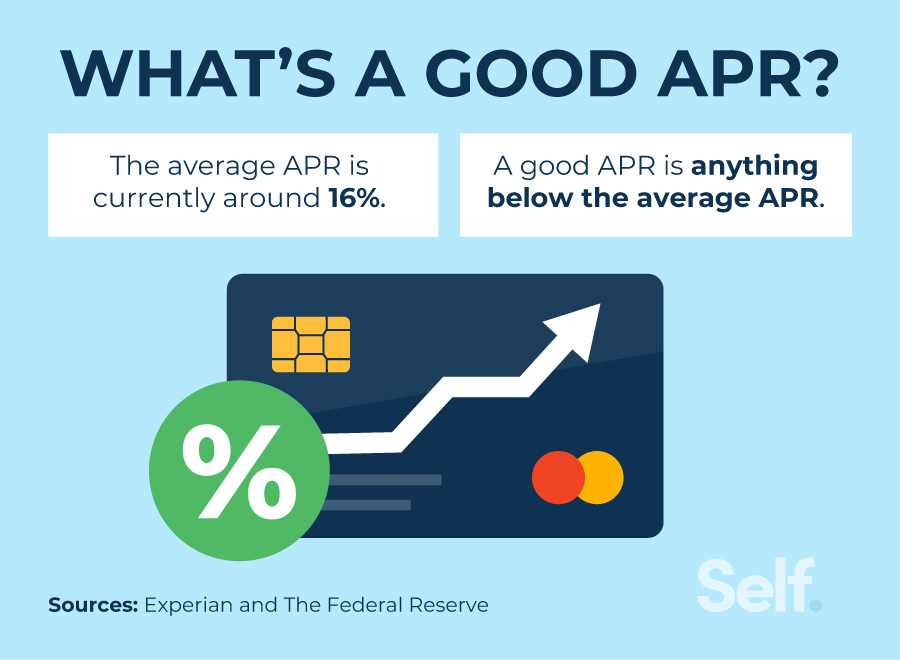

Defining a “good” credit card APR is subjective and depends heavily on your individual financial situation and the current economic climate. However, we can establish benchmarks and understand what is considered competitive.

Average Credit Card APRs

As of late 2023 and early 2024, average credit card APRs for new offers have been hovering in the mid-20% range, often between 20% and 25%. This figure represents the average across all credit card types and applicant credit profiles.

Benchmarks for Different Credit Profiles

The “goodness” of an APR is best evaluated relative to your creditworthiness:

- Excellent Credit (740+ FICO Score): Individuals with excellent credit scores are typically eligible for the lowest APRs. A “good” APR for this group might be in the 15% to 20% range. Some premium cards or limited-time offers might even dip below 15% for purchases or balance transfers.

- Good Credit (670-739 FICO Score): Those with good credit can expect slightly higher APRs. A competitive APR for this segment would likely fall between 18% and 23%.

- Fair Credit (580-669 FICO Score): Applicants in this range will generally face higher APRs. A “good” APR here is relative and might be in the 24% to 29% range, though it could be higher depending on the issuer and specific card.

- Poor Credit (Below 580 FICO Score): For individuals with poor credit, obtaining a credit card with a low APR is challenging. Secured credit cards or cards specifically designed for rebuilding credit often come with very high APRs, sometimes exceeding 30% or even 35%. In this scenario, a “good” APR is more about finding a card that helps rebuild credit rather than minimizing interest costs.

Beyond the Average: Considering Promotional Offers

It’s vital to remember that introductory offers can dramatically alter the immediate cost of borrowing. A card with a standard APR of 25% might be considered “good” if it offers a 0% introductory APR on purchases and balance transfers for 12-18 months. However, the long-term APR after the promotional period expires is the more critical factor for ongoing balances.

Strategies for Securing a Favorable APR

Obtaining a credit card with a low APR is not solely about luck; it involves proactive financial management and strategic card selection.

Build and Maintain Strong Credit

The most impactful strategy for securing a low APR is to cultivate excellent credit.

- Pay Bills On Time, Every Time: Payment history is the single largest factor in your credit score. Set up automatic payments or reminders to ensure you never miss a due date.

- Keep Credit Utilization Low: Aim to use no more than 30% of your available credit limit on each card and overall. Lower utilization signals to lenders that you are not overextended.

- Avoid Opening Too Many New Accounts Quickly: While opening new accounts can be beneficial, doing so in rapid succession can negatively impact your credit score. Space out applications.

- Review Your Credit Reports Regularly: Check your credit reports from the three major bureaus (Equifax, Experian, TransUnion) for any errors that could be dragging down your score.

Shop Around and Compare Offers

Don’t settle for the first credit card offer you receive. Actively compare APRs, fees, and benefits from various issuers.

- Use Pre-qualification Tools: Many credit card issuers offer pre-qualification tools that allow you to see if you’re likely to be approved for a card and at what potential APR without a hard inquiry on your credit report.

- Focus on Cards for Your Credit Profile: Target cards that are designed for individuals with your credit score range. Applying for cards that are out of reach will likely result in rejection and multiple hard inquiries.

Negotiate Your APR

If you have a good credit history with your current card issuer and are facing a high APR, consider negotiating.

- Call Customer Service: After a few months of responsible usage (on-time payments, low utilization), contact the card issuer’s customer service department.

- Highlight Your Loyalty and Payment History: Explain that you are a loyal customer with an excellent payment record and inquire if they can offer a lower APR.

- Be Prepared to Switch: If your current issuer is unwilling to budge, you may need to consider transferring your balance to a card with a better rate.

The Impact of APR on Your Financial Health

The APR on your credit card has a profound effect on your financial well-being, especially if you carry a balance.

The True Cost of Carrying a Balance

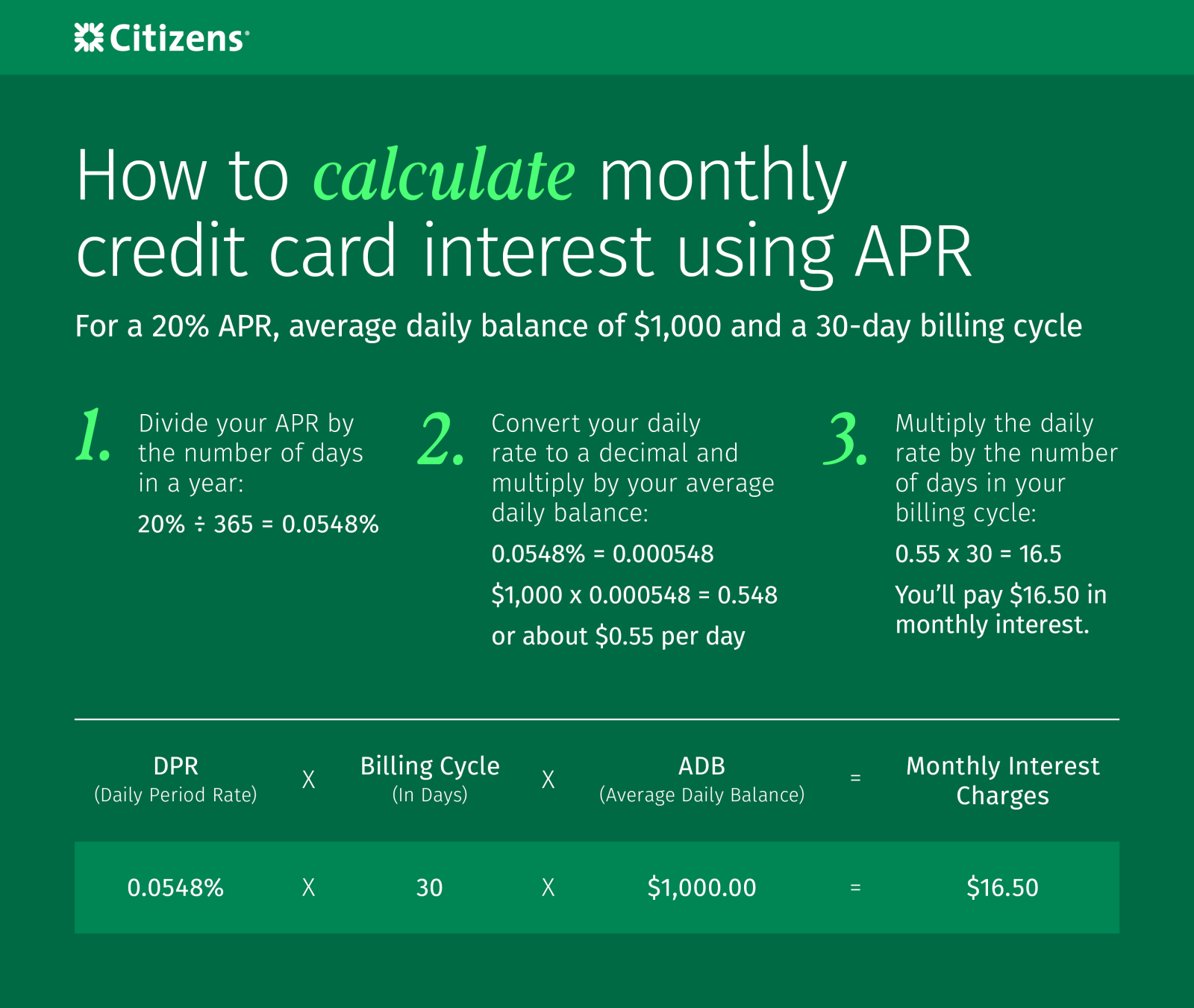

Let’s illustrate the impact of APR with an example. Suppose you have a $5,000 balance on a credit card with a 22% APR. If you only make the minimum payment, it could take years and thousands of dollars in interest to pay off the debt. For instance, a minimum payment of 1% of the balance plus interest would result in an initial payment of around $100-$120. At this rate, it could take over 10 years and you would pay nearly $4,000 in interest.

Conversely, if you had a card with a 15% APR on the same $5,000 balance and paid it off more aggressively, say $300 per month, you would clear the debt in under two years and pay significantly less in interest. This highlights the critical importance of a lower APR for anyone who anticipates carrying a balance.

Strategic Use of Low APR Cards

- Large Purchases: If you plan to make a large purchase, a card with a 0% introductory purchase APR can allow you to pay it off over time without incurring interest charges.

- Debt Consolidation: For those with multiple high-interest credit card debts, a balance transfer to a card with a 0% introductory balance transfer APR can be a powerful tool for saving money and simplifying repayment. However, always factor in any balance transfer fees and be aware of the APR after the promotional period ends.

Conclusion: APR as a Key Factor in Credit Card Selection

In conclusion, a “good” credit card APR is one that is competitive relative to your credit score and the current economic environment, and crucially, is one that aligns with your spending and repayment habits. For individuals with excellent credit, an APR in the mid-to-high teens is a benchmark, while those with less-than-perfect credit will naturally face higher rates. The primary strategy for achieving a favorable APR is to consistently maintain strong creditworthiness. Beyond the advertised rate, understanding the different types of APRs and their implications, especially penalty APRs and introductory offers, is essential. By prioritizing a low APR, especially if you anticipate carrying a balance, you can significantly reduce the cost of borrowing and improve your overall financial health. When choosing a credit card, always consider the APR as a paramount factor alongside rewards, fees, and benefits.