The Credit Card Verification Code (CVC), also known as a Card Verification Value (CVV) or Card Security Code (CSC), is a critical security feature found on most credit and debit cards. Its primary purpose is to authenticate a cardholder during transactions where the physical card is not present, such as online purchases or mail-order telephone sales (MOTO). This three or four-digit code plays a vital role in combating fraud by providing an additional layer of security beyond the card number and expiration date. Understanding what the CVC is, where to find it, and how it functions is essential for both consumers and businesses to ensure secure transactions.

Understanding the CVC: Purpose and Function

The Credit Card Verification Code is a unique security feature designed to verify that the person making a transaction is in possession of the actual credit or debit card. Unlike the primary account number (PAN) and expiration date, which are embedded in the magnetic stripe and often printed on the card, the CVC is a distinct security measure. Its strategic placement and the fact that it is not stored in the magnetic stripe’s data make it a powerful tool against card skimming and data breaches where only the PAN and expiration date might be compromised.

The Genesis of Card Security Codes

The development of card security codes emerged as a response to the increasing prevalence of credit card fraud, particularly in the nascent stages of e-commerce and remote transactions. As businesses began accepting payments without the physical presence of the card, the risk of fraudulent transactions escalated. The CVC was introduced by major credit card networks like Visa and Mastercard to provide an additional authentication factor, making it significantly harder for fraudsters to make unauthorized purchases using stolen card numbers alone.

How the CVC Works in Transactions

When you make a purchase online or over the phone, you are typically asked to provide your CVC along with your card number and expiration date. The CVC is then transmitted securely to the payment processor and subsequently to the issuing bank for verification. The issuing bank checks the provided CVC against the code associated with your card. If the codes match, the transaction is considered more secure and is likely to be approved. If the CVC does not match, the transaction may be flagged as suspicious or declined, even if the card number and expiration date are valid.

It’s crucial to understand that merchants are generally prohibited from storing the CVC after a transaction is authorized. This “no-storage” rule is a fundamental aspect of PCI DSS (Payment Card Industry Data Security Standard) compliance, further enhancing the security of this code. By not retaining the CVC, merchants significantly reduce the risk of it being compromised in a data breach.

Differentiating CVC, CVV, and CSC

While often used interchangeably, the terms CVC, CVV, and CSC refer to the same fundamental security code, with slight variations in nomenclature employed by different credit card networks:

- CVC (Card Verification Code): This term is primarily used by Mastercard.

- CVV (Card Verification Value): This term is used by Visa.

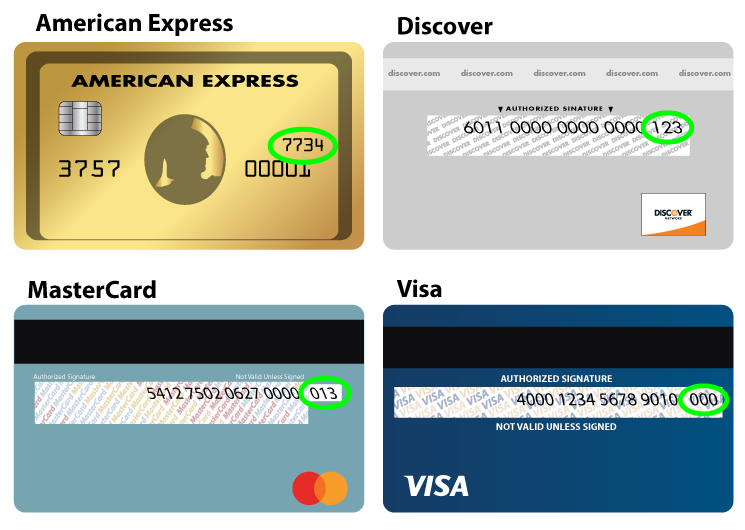

- CSC (Card Security Code): This is a more general term often used by Discover and American Express, though American Express typically uses a four-digit code.

Regardless of the specific acronym, the function and location of the code on the card are largely the same. For American Express cards, the code is usually a four-digit number located on the front of the card, above the embossed account number. For Visa, Mastercard, and Discover cards, it’s typically a three-digit number on the back of the card, in or near the signature strip.

Locating Your Credit Card Verification Code

The physical location of your Credit Card Verification Code varies slightly depending on the card issuer and the type of card you possess. Knowing where to find it is straightforward for most consumers.

Three-Digit Codes: Visa, Mastercard, and Discover

For the vast majority of Visa, Mastercard, and Discover cards, the CVC (or CVV/CSC) is a three-digit number. You will find it printed on the back of your card, typically within or adjacent to the signature strip. In most cases, it will be the last three digits printed in the signature area.

- On the back of the card: Look for a series of numbers. The CVC will be the final three digits.

- Signature strip: The code is often printed to the right of the signature space.

If you have trouble locating it, a quick glance at your card’s rear face should reveal the three-digit code.

Four-Digit Codes: American Express

American Express cards have a slightly different system. Their security code, often referred to as a CID (Card Identification Number), is a four-digit number. This code is usually located on the front of the card, printed above the embossed account number, typically on the right-hand side.

- On the front of the card: Examine the area above your main card number.

- Right-hand side: The four-digit code is usually positioned on this side.

This distinct placement for American Express helps differentiate it from the three-digit codes found on other major credit card networks.

The Importance of CVC Security

The Credit Card Verification Code is more than just a series of digits; it’s a fundamental component of modern transaction security. Its proper handling and understanding are paramount to protecting yourself from fraudulent activities.

Protecting Your CVC from Fraud

Since the CVC is used to authenticate card-not-present transactions, it is a prime target for fraudsters. While merchants are restricted from storing it, the risk arises when this information is exposed through phishing scams, malware, or insecure websites.

- Be Wary of Phishing Attempts: Never provide your CVC in response to unsolicited emails, text messages, or phone calls. Legitimate merchants will only ask for the CVC during the checkout process on their secure website or when you are actively making a purchase over the phone.

- Secure Your Devices: Ensure your computer and mobile devices are protected with up-to-date antivirus software and firewalls. This helps prevent malware from capturing your sensitive information, including your CVC.

- Shop on Secure Websites: Look for “https://” at the beginning of the web address and a padlock icon in your browser’s address bar when entering your card details. This indicates that the website uses encryption to protect your data.

- Never Write Down Your CVC: Do not record your CVC on a sticky note or in an easily accessible digital file.

- Shred Sensitive Documents: If you must discard a card, ensure you shred it thoroughly, including the area where the CVC is printed.

CVC and PCI DSS Compliance

The Payment Card Industry Data Security Standard (PCI DSS) is a set of security standards designed to ensure that all companies that accept, process, store, or transmit credit card information maintain a secure environment. The CVC plays a significant role in PCI DSS compliance, particularly concerning the rule against storing sensitive authentication data.

Key PCI DSS rules related to CVC:

- Prohibition of Storage: Merchants are strictly forbidden from storing the CVC after the transaction authorization. This includes storing it in databases, logs, or any other form of electronic or physical record.

- Verification During Transactions: The CVC is used as a verification tool during card-not-present transactions to authenticate the cardholder.

- Transmission Security: While not explicitly mandated for transmission like the full card number, secure transmission protocols should be used for all sensitive cardholder data, including the CVC during the authorization process.

Adherence to these rules by merchants is crucial for preventing large-scale data breaches that could expose CVC information. For consumers, understanding these protocols reinforces the importance of sharing this code only through secure and trusted channels.

Beyond the Basic: Advanced Security and Future Trends

While the CVC has proven to be an effective fraud deterrent, the landscape of digital transactions is constantly evolving. The industry continues to explore and implement more robust security measures to stay ahead of sophisticated fraudsters.

Tokenization and EMV Chip Technology

Two significant advancements in payment security that complement and, in some cases, supersede the reliance on CVC for in-person transactions are tokenization and EMV chip technology.

- EMV Chip Technology: Chip-enabled cards (also known as smart cards) embed a microprocessor that generates a unique transaction code for each purchase. This makes it much harder to counterfeit cards for in-person transactions compared to the older magnetic stripe technology. For chip-enabled transactions, the CVC is generally not required.

- Tokenization: This process replaces sensitive cardholder data, such as the primary account number and CVC, with a unique identifier called a “token.” This token can be used for processing transactions without exposing the actual card details. Tokenization is widely used in mobile payment systems (like Apple Pay and Google Pay) and online payment gateways, offering a more secure alternative to transmitting raw card data.

The Future of Card Verification

As technology advances, the methods for verifying cardholder identity will continue to evolve. While the CVC remains a vital security feature for card-not-present transactions, its role might diminish over time as more secure authentication methods become widespread. Biometric authentication (fingerprint, facial recognition), multi-factor authentication, and advanced AI-driven fraud detection systems are increasingly being integrated into payment processes.

However, for the foreseeable future, the Credit Card Verification Code will continue to be an indispensable part of secure online and remote purchasing, acting as a silent guardian of your financial information. Understanding its purpose, location, and the importance of keeping it confidential is a fundamental step towards ensuring a safer digital shopping experience.