A credit report is a detailed record of your credit history, serving as a crucial document for lenders, creditors, and increasingly, other service providers. Understanding the factual data contained within this report is paramount to managing your financial health effectively. This data is meticulously collected and updated by credit bureaus, painting a comprehensive picture of your financial behavior over time. While the term “factual” implies objective truth, it’s essential to recognize that the accuracy of this data hinges on the reporting entities and the integrity of the systems that collect and process it. This article will delve into the core components of your credit report, dissecting the factual data that comprises it.

Personal Identification Information

The bedrock of any credit report is accurate personal identification. This section aims to unequivocally link the report to you, preventing misidentification and ensuring the integrity of the credit data. Lenders use this information to verify your identity before extending credit or reviewing your existing accounts.

Name and Aliases

Your full legal name is the primary identifier. However, credit reports also often include any aliases or previous names you have used. This is crucial for capturing all credit accounts that might have been opened under a different name, especially for individuals who have been married and changed their surname.

Social Security Number (SSN)

Your Social Security Number is a unique, nine-digit identifier issued by the U.S. Social Security Administration. It is a critical piece of data used to accurately track your credit history across different financial institutions. Strict protocols govern the use and disclosure of SSNs due to their sensitive nature and importance in preventing identity theft.

Date of Birth

Your date of birth further helps in distinguishing you from individuals with similar names. It’s a standard demographic data point used in conjunction with other identifiers to confirm your identity.

Current and Previous Addresses

This section lists your current residential address and any previous addresses you have occupied. This information is valuable for lenders in assessing your stability and for fraud detection. A consistent address history can be viewed positively, while frequent moves might raise some concerns for certain types of credit applications. The inclusion of previous addresses ensures that all credit lines associated with your past residences are accurately reflected.

Credit Accounts: The Heart of Your Report

The most significant portion of your credit report details your various credit accounts. This is where lenders find the most relevant information to assess your creditworthiness. Each account entry is a rich source of factual data, reflecting your management of borrowed funds.

Types of Credit Accounts

Your report will enumerate different types of credit you have utilized. These typically include:

- Revolving Credit: This category encompasses credit cards, home equity lines of credit (HELOCs), and similar accounts where you have a credit limit and can borrow, repay, and re-borrow funds. The balance on these accounts can fluctuate, and minimum payments are usually required.

- Installment Loans: These are loans with a fixed repayment schedule, such as mortgages, auto loans, and personal loans. You borrow a specific amount and repay it in equal installments over a set period.

- Open Credit: This is less common but refers to accounts where the entire balance is due immediately, such as a retail store account that requires full payment at the time of purchase.

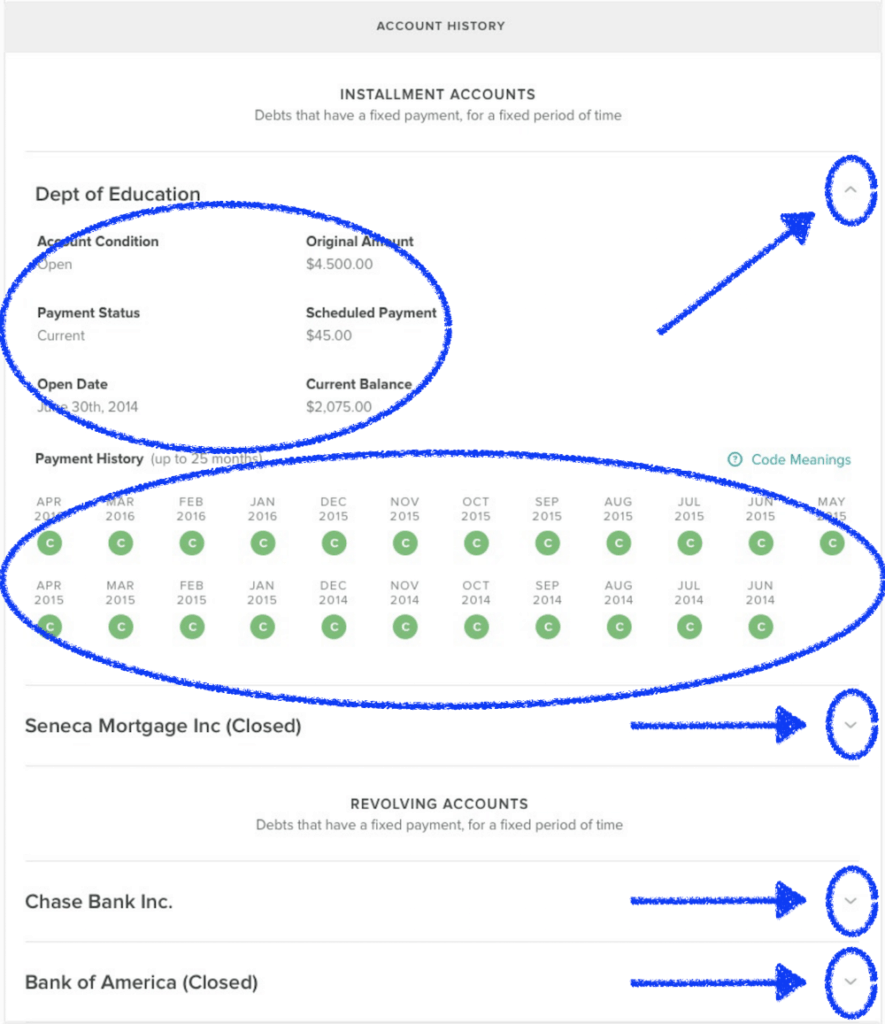

Account Status and History

For each credit account, the report provides a detailed history of its status. This factual data is crucial for understanding your credit behavior:

- Date Opened: The date the account was first established.

- Credit Limit/Loan Amount: The maximum amount you can borrow on a revolving account or the initial principal amount of an installment loan.

- Current Balance: The outstanding amount owed on the account.

- Payment History: This is arguably the most critical component. It meticulously records whether payments were made on time, late payments (specifying the number of days past due, e.g., 30, 60, 90 days), and any defaults or bankruptcies. Each payment is documented chronologically.

- Account Type: Clearly indicates whether it’s a credit card, mortgage, auto loan, etc.

- Creditor Name: The name of the financial institution that extended the credit.

- Account Number (often partially masked): A reference number for the specific account.

Public Records and Collections

This section highlights any negative public records or accounts that have been sent to collections. These are significant indicators of financial distress.

- Bankruptcies: Details of Chapter 7, Chapter 11, or Chapter 13 bankruptcies, including the date filed and discharged.

- Judgments: Court judgments against you, often related to unpaid debts.

- Tax Liens: Claims filed by government entities for unpaid taxes.

- Collection Accounts: Accounts that have been sold to a third-party collection agency because of non-payment. This includes the name of the collection agency and the original creditor.

Inquiries: Tracking Your Credit Activity

When you apply for credit, lenders typically review your credit report. This action is recorded as an inquiry. The type and frequency of inquiries provide insights into your credit-seeking behavior.

Hard Inquiries

A hard inquiry occurs when a lender checks your credit report as part of a credit application process. This includes applications for mortgages, auto loans, credit cards, and personal loans. Hard inquiries can have a small, temporary impact on your credit score, as they suggest you are actively seeking new credit. Your credit report will list the name of the company that made the inquiry and the date it occurred.

Soft Inquiries

A soft inquiry occurs when your credit is checked for reasons other than a direct application for new credit. This includes:

- Checks by your existing creditors to monitor your account.

- Promotional offers of credit.

- Your own personal review of your credit report.

Soft inquiries do not affect your credit score and are not visible to lenders reviewing your report for a credit application. They are typically listed in a separate section of your credit report for your own information.

Credit Inquiries: Understanding Their Impact

The presence of inquiries on your credit report is factual data that lenders consider. While all inquiries are recorded, their significance in terms of credit scoring varies.

Monitoring Your Credit-Seeking Behavior

The factual data of inquiries allows lenders to assess how frequently you are applying for new credit. A high number of recent hard inquiries can sometimes signal increased credit risk, as it might suggest financial difficulties or a tendency to overextend oneself. However, credit scoring models are sophisticated and usually distinguish between a concentrated period of applications for a major purchase (like a mortgage or car) and scattered applications for multiple credit cards.

Distinguishing Between Hard and Soft Inquiries

It is vital to understand the difference between hard and soft inquiries. Hard inquiries are directly related to applying for credit and are therefore a factual indicator of your intent to take on new debt. Soft inquiries, on the other hand, are informational and do not reflect a commitment to borrow. Lenders primarily focus on hard inquiries when evaluating your creditworthiness.

Summary of Factual Data

The factual data on your credit report is a dynamic and comprehensive record. It comprises your personal identifiers, a detailed history of all your credit accounts (including how you’ve managed them), any public records or collection activity, and a log of credit inquiries. Each piece of information, from the date an account was opened to the precise day a payment was late, is a factual entry designed to provide a clear and objective overview of your financial past.

Accuracy and Dispute Resolution

While the data on your credit report is intended to be factual, errors can occur. These errors can stem from various sources, including incorrect reporting by creditors, data entry mistakes by credit bureaus, or issues with identity verification. If you find any inaccuracies on your credit report, you have the right to dispute them. The credit bureaus are legally obligated to investigate these disputes and correct any factual errors. This process ensures that your credit report accurately reflects your financial standing.

The Importance of Regular Review

Understanding the factual data on your credit report is not a one-time task. Regularly reviewing your report from each of the three major credit bureaus (Equifax, Experian, and TransUnion) is essential. This allows you to:

- Verify the accuracy of personal information.

- Monitor your credit accounts for unauthorized activity.

- Identify any negative information that may be inaccurately reported.

- Track your progress in building or improving your credit.

By actively engaging with the factual data presented in your credit report, you empower yourself to make informed financial decisions, maintain a healthy credit profile, and achieve your financial goals. The information contained within is a direct reflection of your financial journey, and comprehending it is the first step toward a stronger financial future.