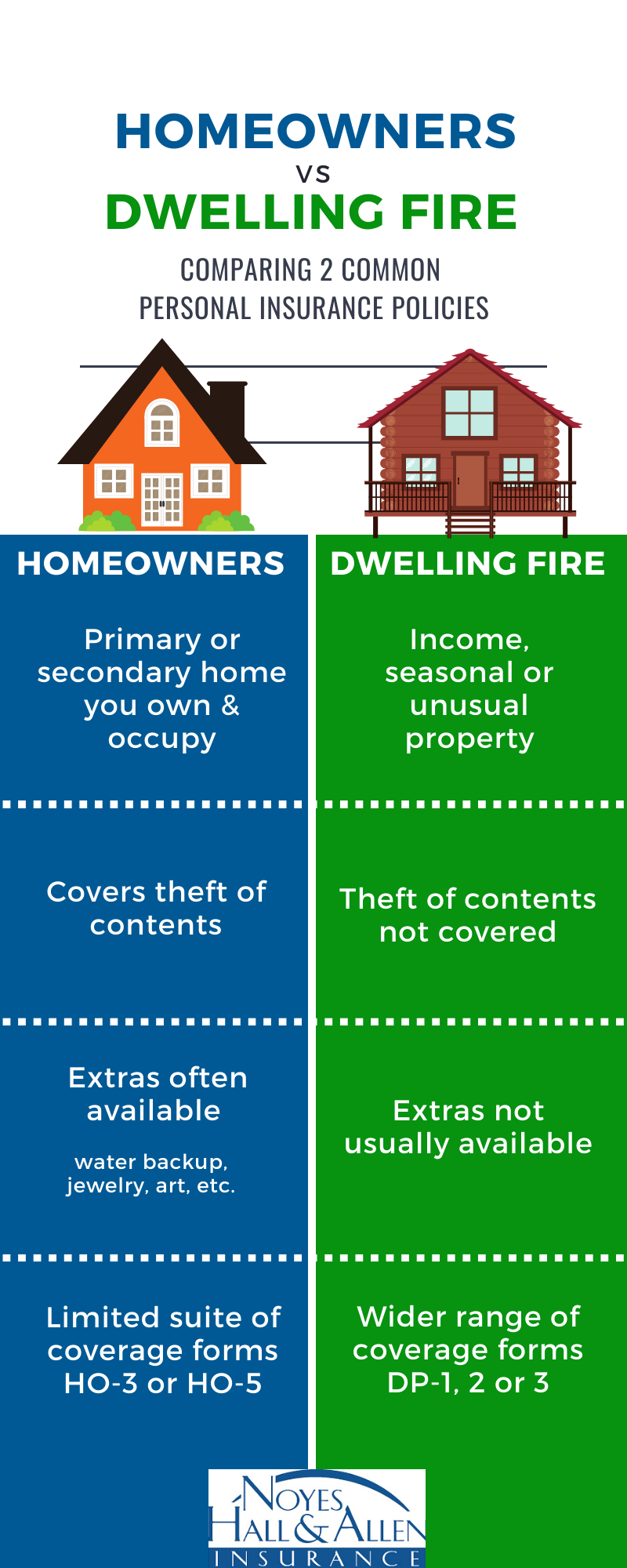

Dwelling fire insurance, often referred to as “dwelling property insurance” or “fire insurance for homes,” is a specialized type of homeowners insurance designed to protect a dwelling and its attached structures against damage from fire and other specified perils. While it shares similarities with a standard homeowners policy (HO-3), dwelling fire policies typically offer a more focused and often more affordable level of coverage, making them an attractive option for a specific range of property owners. Understanding the nuances of dwelling fire insurance is crucial for making informed decisions about protecting your most significant asset.

Understanding the Core Coverage of Dwelling Fire Insurance

At its heart, dwelling fire insurance provides protection for the physical structure of your home. This includes the walls, roof, foundation, and other permanently attached components. The policy is designed to cover the cost of repairing or rebuilding your dwelling if it is damaged or destroyed by a covered peril.

Covered Perils: Beyond Just Fire

While the name emphasizes “fire,” dwelling fire insurance policies typically extend coverage to a broader range of perils. The exact list of covered perils can vary between insurers and policy forms, but common inclusions often feature:

- Fire and Smoke: This is the foundational coverage, protecting against damage caused by intentional fires, accidental fires, and smoke damage.

- Lightning: Protection against damage from lightning strikes, which can cause electrical surges, fires, and structural damage.

- Windstorm and Hail: Coverage for damage caused by strong winds, hurricanes, tornadoes, and hailstorms. This is a critical component in many regions prone to severe weather.

- Explosion: Protection against damage from various types of explosions, such as gas explosions or explosions from internal household systems.

- Riot and Civil Commotion: Coverage for damage caused during riots or civil disturbances.

- Vandalism and Malicious Mischief: Protection against intentional damage to your property by others.

- Vehicle and Aircraft Impact: Coverage for damage caused by vehicles or aircraft colliding with your dwelling.

- Falling Objects: Protection against damage from objects that fall onto your property, such as trees or debris.

- Weight of Ice, Snow, and Sleet: Coverage for structural damage caused by excessive accumulation of ice, snow, or sleet.

- Water Damage (Limited): While not as comprehensive as in a standard homeowners policy, some dwelling fire policies may offer limited coverage for certain types of water damage, such as from burst pipes within the dwelling itself. It’s important to note that flood damage is almost universally excluded from these policies and requires separate flood insurance.

What Dwelling Fire Insurance Typically Does NOT Cover

It’s equally important to understand the limitations of dwelling fire insurance. These policies are generally more basic than a comprehensive homeowners policy and often exclude coverage for:

- Personal Property (Contents): Dwelling fire policies primarily focus on the structure itself. They usually do not include coverage for your personal belongings, such as furniture, electronics, clothing, or other possessions. If you need to cover your contents, you would typically need a separate policy or endorsement.

- Loss of Use/Additional Living Expenses: In the event of a covered loss that makes your home uninhabitable, dwelling fire insurance typically does not cover the costs of temporary housing, meals, and other expenses associated with living elsewhere while your home is being repaired.

- Liability Protection: Standard homeowners insurance includes liability coverage, which protects you if someone is injured on your property and sues you. Dwelling fire policies generally do not include this liability component.

- Flood and Earthquake Damage: As mentioned, damage from floods, rising waters, and earthquakes are almost always excluded and require separate specialized insurance policies.

- Wear and Tear/Gradual Deterioration: Insurance policies are designed to cover sudden, accidental events, not the natural aging and deterioration of your property over time.

- Mold and Fungus (with exceptions): Many policies exclude mold and fungus damage unless it results directly from a covered peril (e.g., mold that grows after a covered water pipe burst).

- Pest Infestations: Damage caused by termites, rodents, or other pests is typically not covered.

Types of Dwelling Fire Policies

Dwelling fire insurance is not a monolithic product. Insurers offer different forms, each with its own scope of coverage. The most common forms are:

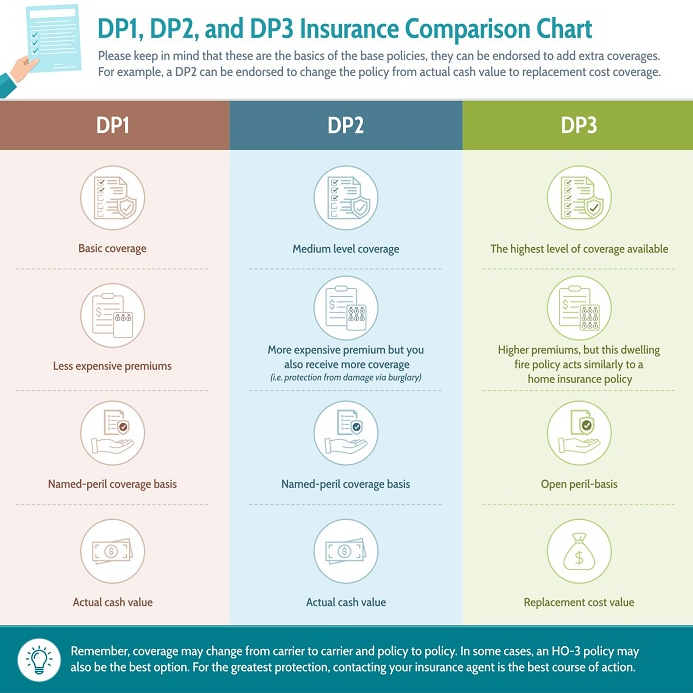

DP-1: Basic Form

The DP-1 policy, also known as the “Basic Form,” is the most limited and least expensive type of dwelling fire insurance. It covers only a specific, named list of perils. If a peril is not explicitly listed on the policy, it is not covered.

- Named Perils: Typically includes fire, lightning, and internal explosion. Some DP-1 policies may offer an option to add windstorm and hail coverage.

- Actual Cash Value (ACV): Losses are paid based on the current market value of the damaged property, taking into account depreciation. This means you’ll receive the cost to replace the damaged item minus its age and wear and tear.

- Limited Coverage: This is the most basic protection and is generally suitable for very low-value properties or as a temporary solution.

DP-2: Broad Form

The DP-2 policy, or “Broad Form,” offers a more extensive list of covered perils than the DP-1. It also provides a more favorable method of loss settlement.

- Broader Named Perils: Includes all perils covered by DP-1, plus additional perils such as vandalism, malicious mischief, windstorm and hail, weight of ice, snow, and sleet, falling objects, and water damage from plumbing, heating, or air conditioning systems.

- Replacement Cost Value (RCV) for the Dwelling: For the dwelling structure itself, DP-2 policies typically pay out on a replacement cost basis. This means the insurer will pay the cost to repair or rebuild the damaged portion of your home with materials of similar kind and quality, without deducting for depreciation. However, personal property coverage, if added, is usually still on an ACV basis.

- More Comprehensive Protection: A step up in coverage from DP-1, offering better protection against a wider array of common causes of damage.

DP-3: Special Form

The DP-3 policy, or “Special Form,” is the most comprehensive type of dwelling fire insurance. It offers the broadest protection and is closest in scope to a standard HO-3 homeowners policy, though still without personal property or liability coverage unless added.

- Open Perils Coverage for the Dwelling: This is the key distinction. Instead of listing specific perils that are covered, the DP-3 policy covers all perils except those that are specifically excluded. This provides significantly more protection against a wider range of unforeseen events.

- Named Perils for Other Structures: Typically, attached structures (like garages) and unattached structures on the property are covered on a named perils basis, similar to DP-2.

- Replacement Cost Value (RCV) for the Dwelling and Other Structures: Usually pays on an RCV basis for both the dwelling and other structures.

- Optional Coverage for Contents and Liability: While the base DP-3 policy doesn’t include personal property or liability, these coverages can often be added through endorsements or riders.

Who Needs Dwelling Fire Insurance?

Dwelling fire insurance is not suitable for every homeowner. It is primarily designed for individuals who own property but do not live in it, or for those who require a specific, more limited form of property protection. Common scenarios where dwelling fire insurance is appropriate include:

Landlords and Rental Properties

This is perhaps the most common use case for dwelling fire insurance. If you own a property that you rent out to tenants, you will need insurance to protect your investment. Standard homeowners insurance is not designed for rental properties, as it assumes you are the occupant. Dwelling fire policies (especially DP-2 and DP-3) are tailored to cover the dwelling and structures of a rental unit.

- Protection for the Structure: Covers the main building, garages, and other attached or detached structures from damage.

- Rental Income Loss (Optional): Many dwelling fire policies allow for an endorsement that covers lost rental income if the property becomes uninhabitable due to a covered peril. This is crucial for landlords to maintain cash flow.

- No Occupancy Clause: Unlike standard homeowners policies, dwelling fire policies do not typically have an occupancy clause that would void coverage if the property is vacant for an extended period (though there might be limitations for very long vacancies).

Vacant Properties

If you own a property that is currently unoccupied – perhaps while you are renovating it, it’s awaiting sale, or you are away for an extended period – a dwelling fire policy can provide essential coverage. Standard homeowners policies often have strict vacancy clauses that can limit or deny coverage if the property is vacant for more than 30 days.

- Protection During Vacancy: Ensures the property remains protected against fire, vandalism, and other covered perils even when it’s empty.

- Careful Review of Policy Terms: It’s vital to understand the specific vacancy clauses and duration limits within any dwelling fire policy to ensure continuous coverage.

Properties with Specific Insurance Needs

In some instances, individuals might choose dwelling fire insurance even if they occupy their home, particularly if they are seeking a more cost-effective solution or have specific risk exposures that are better addressed by these policies. This might include:

- Older Homes with Unique Risks: Sometimes older homes might have specific insurance challenges, and a dwelling fire policy might be structured to address those particular risks more effectively or affordably.

- Second Homes or Seasonal Properties: While not always the case, in some situations, dwelling fire policies might be considered for second homes that are not occupied year-round.

When Dwelling Fire Insurance is NOT Sufficient

It’s crucial to reiterate that dwelling fire insurance is not a one-size-fits-all solution. It is generally insufficient for owner-occupied homes that require comprehensive protection for both the structure and personal belongings, as well as liability coverage. For most homeowners who live in their homes, a standard HO-3 or HO-5 homeowners policy is the appropriate choice. These policies offer broader protection for personal property, liability, and additional living expenses.

Key Considerations When Purchasing Dwelling Fire Insurance

Choosing the right dwelling fire insurance policy requires careful consideration of your property, your needs, and the available options.

Deductibles

The deductible is the amount you pay out-of-pocket before your insurance coverage kicks in. Higher deductibles generally lead to lower premiums, but it’s important to choose a deductible you can comfortably afford in the event of a claim. Dwelling fire policies may have separate deductibles for different perils, such as a standard deductible for most claims and a higher deductible for windstorm and hail.

Policy Limits

The policy limit is the maximum amount your insurer will pay for a covered loss. For dwelling fire insurance, the dwelling coverage limit should be sufficient to rebuild your home at current construction costs. It’s a good idea to get an estimate from a reputable builder or use online replacement cost calculators to determine an adequate limit.

Endorsements and Riders

Many dwelling fire policies can be customized with endorsements or riders to add coverage that is not included in the base policy. Common endorsements include:

- Coverage for Other Structures: While DP-1 might have limited or no coverage for detached structures like sheds or garages, endorsements can add this.

- Loss of Rent/Rental Income: Essential for landlords to cover income lost if the property becomes uninhabitable.

- Personal Property Coverage (Contents): If you need to insure the contents of a rental property.

- Vandalism and Malicious Mischief: Can be added to DP-1 policies.

- Water Backup and Sump Pump Overflow: To cover damage from these specific causes.

Insurance Company Reputation and Financial Stability

When purchasing any insurance, it’s vital to choose a reputable and financially stable insurance company. Look for insurers with strong financial ratings from agencies like A.M. Best and research customer satisfaction reviews. A financially sound insurer is more likely to be able to pay claims promptly and reliably.

Policy Review and Understanding

Read your policy documents carefully, and don’t hesitate to ask your insurance agent or provider to clarify any terms or conditions you don’t understand. Understanding what is covered, what is excluded, and the claims process is crucial for a smooth experience.

Conclusion

Dwelling fire insurance serves a vital purpose in the insurance landscape, offering targeted protection for property owners who may not require or desire the comprehensive coverage of a standard homeowners policy. Primarily a tool for landlords and owners of vacant properties, it focuses on safeguarding the physical structure of a dwelling and its attached outbuildings. By understanding the different policy forms (DP-1, DP-2, and DP-3), the scope of covered perils, and the common exclusions, individuals can make informed decisions to adequately protect their real estate investments against a range of potential damages. When considering dwelling fire insurance, always assess your specific needs, the characteristics of your property, and the various coverage options available to ensure you have the right protection in place.