An Individual Retirement Arrangement (IRA) custodian plays a fundamental role in the retirement savings landscape. For anyone looking to establish or manage an IRA, understanding the custodian’s function, responsibilities, and significance is paramount. While often operating behind the scenes, custodians are the bedrock upon which IRAs are built, ensuring the security, compliance, and administration of your retirement assets. They are the entities legally empowered to hold and safeguard your investments within an IRA.

The Core Function of an IRA Custodian

At its most basic level, an IRA custodian is a financial institution – typically a bank, trust company, or brokerage firm – that is authorized to hold and administer IRA assets on behalf of the account holder. This is not merely a passive holding function; it involves a comprehensive set of duties designed to protect your retirement savings and ensure adherence to the complex regulations governing IRAs, as set forth by the Internal Revenue Service (IRS).

Holding and Safeguarding Assets

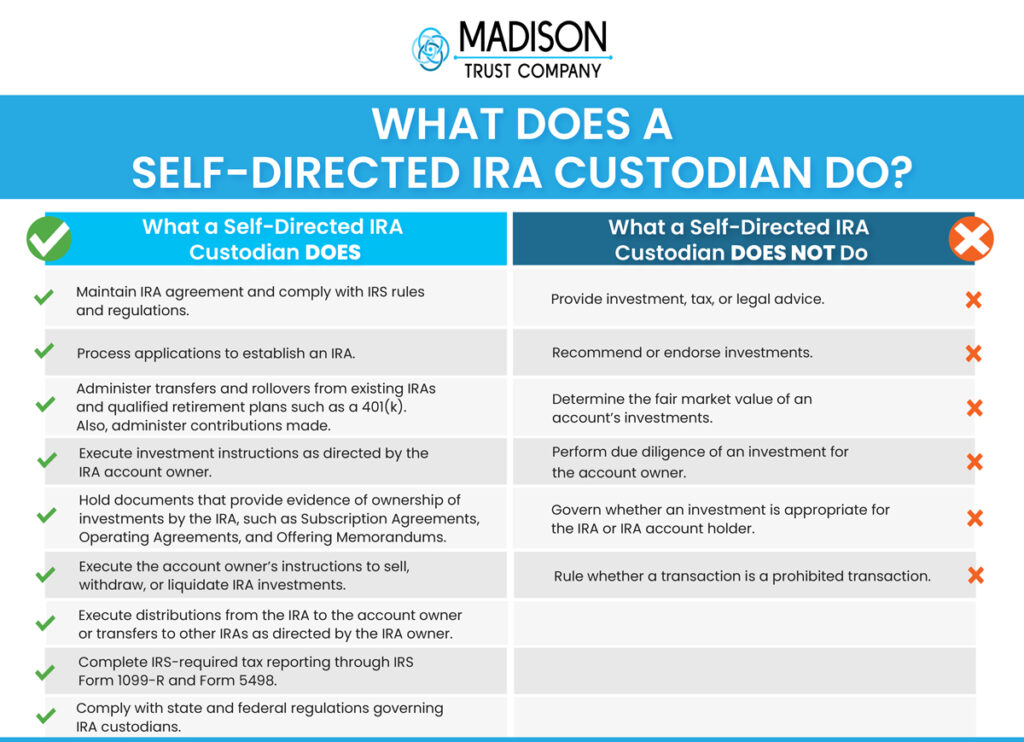

The primary responsibility of an IRA custodian is to physically hold and safeguard the assets within your IRA. This includes not just cash but also the various investment instruments you choose, such as stocks, bonds, mutual funds, exchange-traded funds (ETFs), and potentially alternative investments if the IRA structure allows. The custodian maintains ownership records, ensures that assets are properly registered, and prevents unauthorized access or transactions. This custodial role is critical for asset protection, providing a secure environment for your long-term retirement nest egg.

Facilitating Transactions

Custodians are the conduits through which all transactions within an IRA must flow. When you decide to buy or sell an investment, deposit funds, or withdraw money, these actions are executed through your custodian. They process buy and sell orders, ensure that funds are transferred correctly, and record all activity within your account. This oversight is essential for maintaining accurate accounting and for preventing any actions that would violate IRA rules.

Ensuring Regulatory Compliance

Navigating the intricate web of IRS regulations governing IRAs can be daunting for individual investors. IRA custodians are experts in these rules and are responsible for ensuring that your IRA remains compliant. This includes monitoring contributions to ensure they do not exceed annual limits, tracking distributions to ensure they comply with withdrawal rules (such as age requirements and required minimum distributions or RMDs), and preventing prohibited transactions that could result in severe penalties. Their vigilance helps prevent costly mistakes that could jeopardize your retirement savings.

Record Keeping and Reporting

A crucial function of an IRA custodian is maintaining meticulous records of all account activity. This includes contributions, distributions, investment gains and losses, fees, and any other relevant financial data. These records are essential for tax purposes and for providing you with a clear overview of your retirement portfolio’s performance. Custodians are also responsible for generating and sending out important tax forms, such as Form 5498 (IRA Contribution Information) and Form 1099-R (Distributions From Pensions, Annuities, Retirement Plans, etc.), to both the account holder and the IRS.

Types of IRA Custodians

While the core functions remain consistent, IRA custodians can vary in the services they offer and the types of IRAs they support. Understanding these distinctions can help investors choose the custodian best suited to their needs.

Traditional Brokerage Firms

Many of the largest and most well-known financial institutions operate as IRA custodians. These firms typically offer a wide range of investment products, including stocks, bonds, mutual funds, and ETFs. They often provide online platforms for account management, research tools, and educational resources. For investors who are comfortable making their own investment decisions and prefer a broad selection of publicly traded securities, a traditional brokerage firm can be an excellent choice.

Banks and Trust Companies

Banks and trust companies also serve as IRA custodians, often with a strong emphasis on financial planning and wealth management services. They may offer a more curated selection of investment options, sometimes including proprietary mutual funds or managed accounts. For individuals who value personalized advice and a more integrated approach to their financial planning, a bank or trust company might be a better fit. They often have a fiduciary duty to act in the best interests of their clients, which can provide an additional layer of assurance.

Specialized Custodians for Alternative Investments

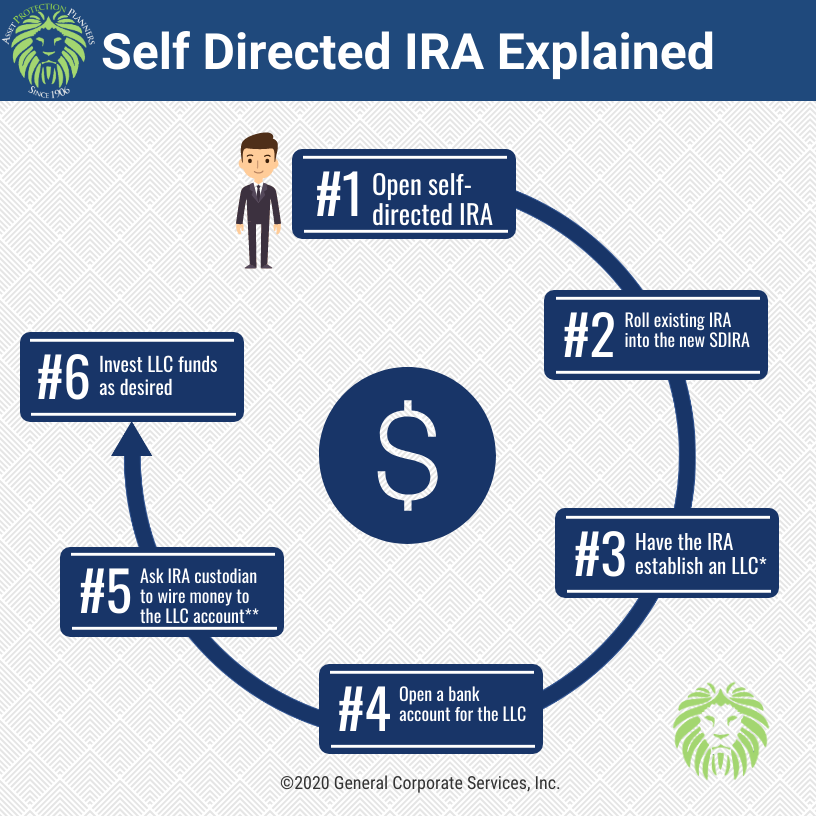

For investors interested in holding alternative assets within their IRA, such as real estate, precious metals, or private equity, specialized custodians are necessary. These custodians are equipped to handle the unique administrative and regulatory requirements associated with non-traditional assets. They will often work in conjunction with a self-directed IRA (SDIRA) administrator to ensure that all transactions and holdings comply with IRS regulations for these less common investment vehicles. It’s important to note that not all IRAs allow for alternative investments, and the fees and complexity associated with them can be higher.

Choosing the Right IRA Custodian

Selecting an IRA custodian is a significant decision that can impact the efficiency, cost, and overall management of your retirement savings. Several key factors should be considered:

Fees and Expenses

Custodial fees can vary widely. It’s crucial to understand the fee structure, which may include account maintenance fees, transaction fees, administrative fees, and fees for specific services. Compare these costs across different custodians to ensure you are getting competitive pricing. Some custodians may waive certain fees if you maintain a minimum balance or meet other criteria.

Investment Options

The range of investment products offered by a custodian is a critical consideration. If you have specific investment preferences, such as access to a particular type of mutual fund, ETF, or even alternative assets, ensure the custodian supports them. A limited investment menu might restrict your ability to diversify or pursue your investment strategy.

Account Minimums and Requirements

Some custodians have minimum deposit requirements to open an IRA or to avoid certain fees. Others may have specific requirements for account management, such as mandatory online access or limited customer service channels. Assess whether these requirements align with your financial situation and preferences.

Online Platform and Tools

For many investors, a robust and user-friendly online platform is essential. This includes ease of navigation, access to account information, trading capabilities, research resources, and educational materials. A well-designed platform can significantly enhance your ability to monitor and manage your investments effectively.

Customer Service and Support

When questions or issues arise, responsive and knowledgeable customer service is invaluable. Consider the availability of customer support (phone, email, chat), their expertise, and their reputation for resolving client issues efficiently. Some investors prefer dedicated financial advisors, while others are comfortable with self-service options.

Reputation and Security

Given that your IRA custodian holds your retirement assets, their trustworthiness, financial stability, and security protocols are paramount. Research the custodian’s history, regulatory standing, and the security measures they have in place to protect your data and assets. Ensure they are registered with relevant regulatory bodies like the SEC and FINRA.

The Custodian’s Role in Self-Directed IRAs (SDIRAs)

Self-Directed IRAs (SDIRAs) offer investors greater control over their investment choices, including the ability to invest in a broader range of assets beyond traditional stocks and bonds. While the investor makes the investment decisions, an SDIRA still requires a custodian to hold and administer the assets. In this context, the custodian’s role is often complemented by a third-party administrator.

The SDIRA custodian holds the assets and ensures that all transactions are properly recorded and that the IRA remains compliant with IRS regulations. However, they typically do not provide investment advice or guidance on alternative investments. The administrator, on the other hand, often handles the paperwork, facilitates transactions with third parties (like real estate agents or private companies), and ensures that the chosen investments are permissible within an IRA structure. The custodian and administrator work in tandem to manage the SDIRA effectively and compliantly.

Conclusion

The IRA custodian is an indispensable component of the retirement savings system. They provide the essential infrastructure for holding, managing, and safeguarding your IRA assets, while ensuring strict adherence to IRS regulations. By understanding the multifaceted responsibilities of an IRA custodian and carefully considering the factors involved in choosing one, investors can make informed decisions that contribute to the long-term security and growth of their retirement nest egg. Whether you are opening your first IRA or looking to transition an existing one, recognizing the vital role of the custodian is a crucial step towards achieving your financial goals.