The concept of an “external bank account” is often encountered in discussions surrounding financial management, business operations, and even personal finance strategies. While the term itself might sound straightforward, understanding its nuances and implications is crucial for anyone seeking to optimize their financial dealings. Fundamentally, an external bank account refers to any bank account that is not the primary, or default, operating account for an individual or an entity. This distinction is not merely semantic; it carries significant operational, security, and strategic weight.

Defining the Primary vs. External Distinction

To grasp the essence of an external bank account, it’s vital to first define what constitutes a “primary” or “internal” bank account. For an individual, this is typically the checking account where their salary is deposited, bills are paid, and everyday transactions occur. For a business, it’s the main operating account used for receiving revenue, disbursing payroll, paying vendors, and managing day-to-day expenses. This primary account is the central hub of financial activity.

An external bank account, in contrast, is any account held with a different financial institution or even a separate account within the same institution that is designated for purposes other than the primary operational flow. The “external” nature arises from its separation from the core financial ecosystem of the individual or business. This separation can be intentional, serving specific strategic objectives, or it can be a consequence of various financial arrangements.

Types of External Accounts

The nature of an external bank account can vary widely depending on the user’s needs and the specific financial products available. Some common types include:

Savings Accounts

While often held at the same institution as a checking account, a savings account maintained for a distinct purpose, such as an emergency fund or a down payment for a future purchase, can be considered external to the immediate transactional flow of the primary checking account. The intent here is to segregate funds for specific future needs, preventing accidental or impulsive spending from the main operating funds.

Investment Accounts

Brokerage accounts, money market accounts, and other investment vehicles, even if held with a traditional bank, are inherently external to the daily operational banking. These accounts are designed for wealth accumulation and capital growth, not for routine transactions. Funds are typically transferred in and out of these accounts with a more strategic intent, often involving larger sums and less frequent activity.

Business-Specific Accounts

For businesses, external accounts can manifest in several ways:

- Payroll Accounts: A separate account dedicated solely to processing payroll. This helps in isolating payroll expenses, simplifying reconciliation, and enhancing control over salary disbursements.

- Tax Accounts: Funds set aside specifically for tax obligations. This ensures that sufficient capital is available when tax payments are due, preventing disruptions to operational cash flow.

- Escrow Accounts: Used in real estate transactions, legal settlements, or other agreements where funds are held by a neutral third party (or a designated separate account) until specific conditions are met.

- Subsidiary Accounts: For larger corporations with multiple divisions or subsidiaries, each might maintain its own primary operating account, which, from the perspective of the parent company’s main account, would be considered external.

- Merchant Accounts: For businesses accepting credit card payments, a merchant account facilitates the transfer of funds from customer payments to the business’s operating account. While linked, it’s a distinct financial mechanism.

International Accounts

An external bank account can also refer to an account held with a bank in a different country. This is common for individuals or businesses with international dealings, investments, or aspirations. Managing finances across borders often necessitates separate accounts to handle currency exchange, specific country regulations, and localized banking services.

Dedicated Purpose Accounts

Beyond formal categories, individuals and businesses might establish external accounts for highly specific purposes:

- Vacation Fund: A savings account for accumulating funds for travel.

- Charitable Giving Account: Funds designated for philanthropic donations.

- Project-Specific Accounts: For businesses undertaking large, distinct projects, a separate account can track all project-related income and expenses, offering clear visibility into project profitability.

Strategic Advantages of External Bank Accounts

The use of external bank accounts is not arbitrary; it’s often driven by a desire to achieve specific strategic financial advantages. These advantages primarily revolve around enhanced control, improved security, better organization, and streamlined financial management.

Enhanced Financial Control and Segregation

The most significant advantage of external accounts is the ability to segregate funds. By moving money out of the primary operating account, individuals and businesses create clear boundaries for different financial purposes. This segregation prevents commingling of funds, which can lead to confusion, errors, and even legal complications, especially in business contexts. For example, using a separate account for payroll ensures that only authorized payroll transactions can occur from that account, reducing the risk of accidental diversion of funds meant for other operational needs.

Improved Security and Risk Mitigation

External accounts can act as a layer of security. If the primary operating account is compromised, the financial damage might be limited if significant funds have been strategically moved to external, less accessible accounts. This is particularly relevant for businesses that handle large volumes of transactions or sensitive data. Furthermore, by dedicating specific accounts to high-risk activities (like online transactions or international transfers), the overall exposure of the primary account is reduced.

Better Budgeting and Cash Flow Management

For individuals, an external savings account for a specific goal (like a house down payment or a new car) makes budgeting more tangible. Seeing the dedicated funds grow can be a powerful motivator. For businesses, external accounts for taxes or payroll provide a predictable buffer for these essential, often large, expenditures. This prevents last-minute scrambles for funds and allows for more accurate cash flow forecasting. It ensures that operational funds remain available for core business activities.

Operational Efficiency and Streamlining

While it might seem counterintuitive, using multiple accounts can sometimes improve operational efficiency. Dedicated accounts for specific functions, like processing a particular type of payment or managing a specific product line, can simplify accounting and reconciliation. For instance, a business might use an external account to manage payments for a subscription service. This simplifies tracking recurring revenue and expenses related to that service, making it easier to analyze its profitability without cluttering the main operating account.

Facilitating Specialized Financial Activities

Certain financial activities necessitate external accounts by their very nature. Investment management, for instance, requires dedicated brokerage accounts. International trade often involves correspondent banking relationships and accounts held in foreign currencies. Escrow services are inherently about holding funds separate from the parties involved until a transaction is complete. In these scenarios, the external account is not just a convenience but a fundamental requirement.

Considerations When Establishing an External Bank Account

While the benefits are clear, establishing and managing external bank accounts requires careful consideration and strategic planning.

Choosing the Right Financial Institution

The choice of bank or credit union for an external account depends on its intended purpose. For international transactions, a bank with a strong global presence and competitive exchange rates is crucial. For investment purposes, a brokerage firm with a wide range of investment options and robust trading platforms is ideal. For simple savings, a high-yield savings account at an institution offering competitive interest rates might be the priority.

Understanding Fees and Charges

Each bank account comes with its own set of fees, including monthly maintenance fees, transaction fees, wire transfer fees, and ATM fees. It’s essential to understand these charges for each external account to ensure they don’t erode the benefits of segregation or create unexpected costs. Some accounts might have minimum balance requirements to waive fees.

Regulatory Compliance

For businesses, especially those operating in regulated industries or across different jurisdictions, establishing and managing external accounts must comply with various banking regulations, anti-money laundering (AML) laws, and know-your-customer (KYC) requirements. Understanding these regulations is paramount to avoid penalties.

Managing Multiple Accounts

The complexity of managing multiple bank accounts, even if they are external to each other, can increase. This requires robust record-keeping, regular reconciliation, and potentially the use of accounting software. For businesses, this might involve dedicated accounting staff or outsourcing.

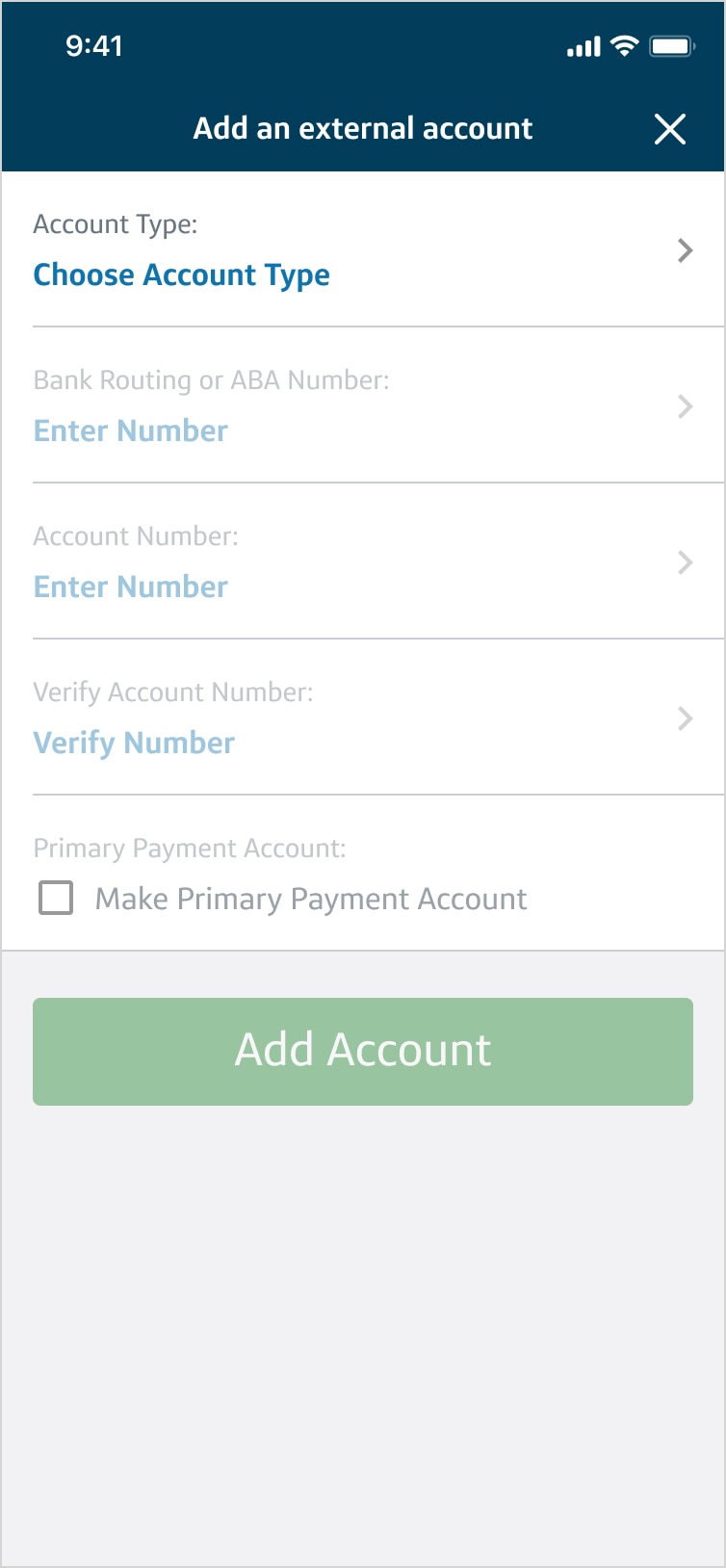

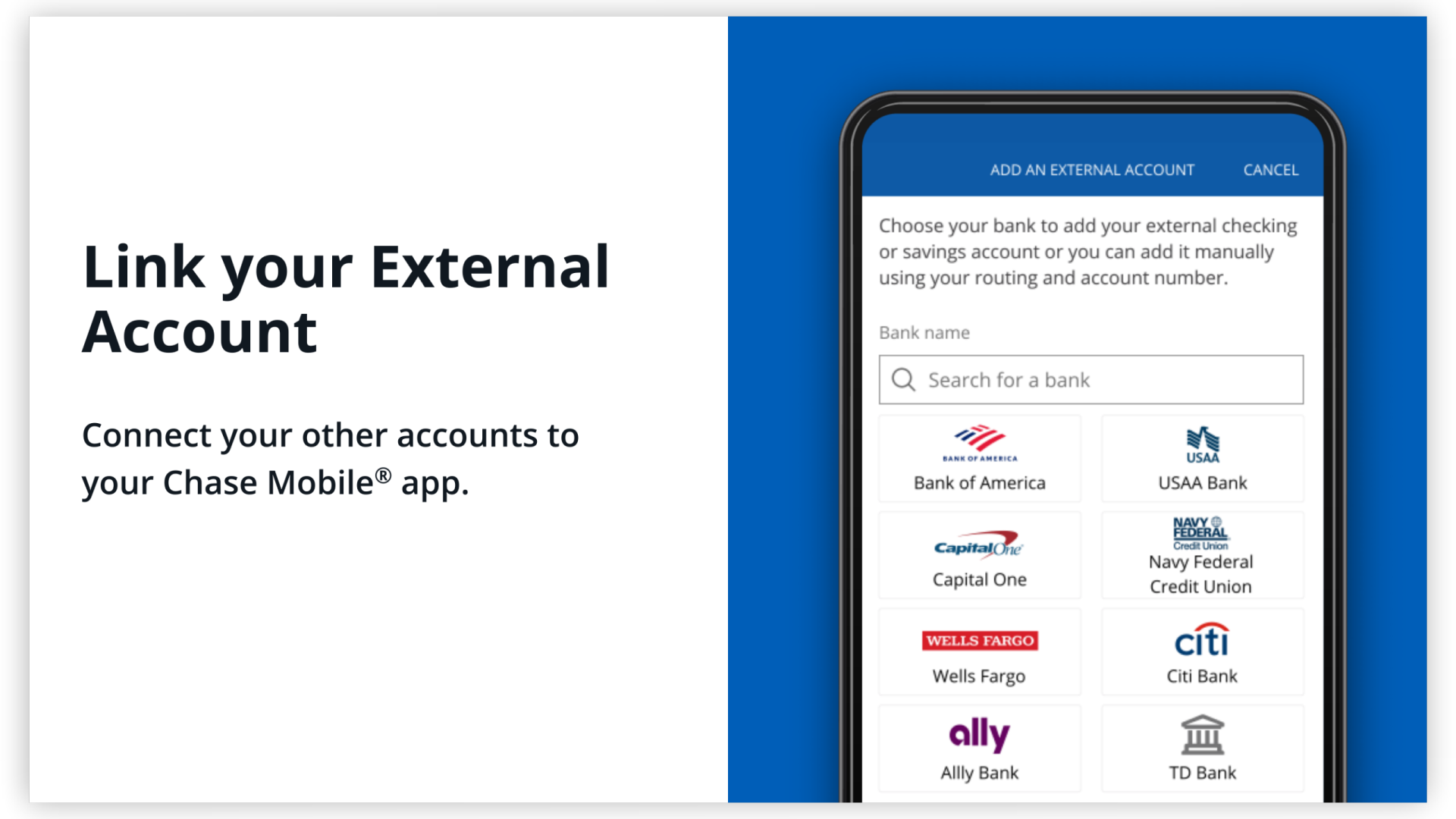

Linking and Transferring Funds

Consider how funds will be transferred between the primary account and external accounts. Many banks offer easy online transfers, but it’s important to understand the speed of these transfers and any associated limits or fees. For businesses, direct deposit and automated clearing house (ACH) payments are common methods.

Conclusion

In essence, an external bank account is a financial tool that provides a strategic separation from an individual’s or entity’s primary banking operations. Whether for enhanced security, improved financial control, specialized investment, or streamlined business processes, the judicious use of external accounts can significantly contribute to robust financial management. Understanding the different types of external accounts and their associated advantages and considerations empowers individuals and businesses to make informed decisions that align with their unique financial goals and operational needs. The concept underscores a mature approach to finance, moving beyond a single point of interaction with a financial institution to a more nuanced and diversified financial architecture.