In the rapidly evolving landscape of financial transactions, the term “e-deposit” has become increasingly prevalent. While its core function is straightforward – depositing funds electronically – understanding the nuances, benefits, and different methods associated with e-deposits is crucial for both individuals and businesses navigating the modern financial world. This exploration delves into the intricacies of e-deposits, examining their various forms, the underlying technologies, and their significant impact on efficiency and accessibility.

Understanding the Fundamentals of E-Deposits

At its most basic, an e-deposit, or electronic deposit, is the transfer of funds from one account to another without the physical handling of cash or checks. This digital process leverages various technologies to ensure speed, security, and convenience. The “e” signifies its electronic nature, distinguishing it from traditional, in-person banking methods.

The Core Concept: Digital Fund Transfers

The fundamental principle behind any e-deposit is the digitization of financial information. Instead of a paper check being processed manually, or cash being physically counted and entered, all information is transmitted and processed digitally. This involves secure communication protocols and established banking infrastructure to facilitate the movement of money from one ledger to another. This digital transformation has been a cornerstone of modern banking, moving away from paper-based systems towards more efficient, real-time transactions.

Security and Verification Mechanisms

A critical aspect of e-deposits is their security. Banks and financial institutions employ a multi-layered approach to protect these transactions. This includes:

- Encryption: Sensitive data, such as account numbers and deposit amounts, are encrypted during transmission, making them unreadable to unauthorized parties. This ensures that even if data is intercepted, it remains unintelligible.

- Authentication: Before a deposit can be processed, the sender and often the recipient are authenticated through various methods, such as passwords, multi-factor authentication (MFA), or biometric verification. This confirms the identity of the individuals involved and prevents fraudulent activity.

- Fraud Detection Systems: Sophisticated algorithms and AI-powered systems continuously monitor transactions for suspicious patterns. These systems can flag unusual activity, such as large deposits from unknown sources or rapid, repeated transactions, to prevent financial crimes.

- Regulatory Compliance: Financial institutions adhere to strict regulations and compliance standards set by governing bodies to ensure the integrity and security of electronic transactions. This includes measures like Know Your Customer (KYC) and Anti-Money Laundering (AML) protocols.

Key Benefits of E-Deposits

The widespread adoption of e-deposits is driven by a compelling set of advantages:

- Speed and Efficiency: E-deposits are significantly faster than traditional methods. Funds can often be credited to an account within minutes or hours, compared to the days it might take for a physical check to clear. This accelerates cash flow for businesses and provides immediate access to funds for individuals.

- Convenience and Accessibility: Deposits can be made anytime, anywhere, from a computer or mobile device. This eliminates the need to visit a physical bank branch, saving time and effort. For individuals in remote locations or those with busy schedules, this accessibility is invaluable.

- Reduced Risk of Loss or Error: The elimination of physical checks reduces the risk of checks being lost in the mail, stolen, or damaged. Digital processing also minimizes the potential for human error in data entry.

- Cost Savings: For businesses, e-deposits can significantly reduce costs associated with processing paper checks, such as postage, stationery, and manual labor.

- Environmental Friendliness: By reducing the reliance on paper, e-deposits contribute to a more sustainable banking ecosystem, decreasing paper waste and its associated environmental impact.

Common Types of E-Deposits

The umbrella term “e-deposit” encompasses several specific methods, each offering unique features and use cases. Understanding these distinctions helps in choosing the most appropriate method for a given situation.

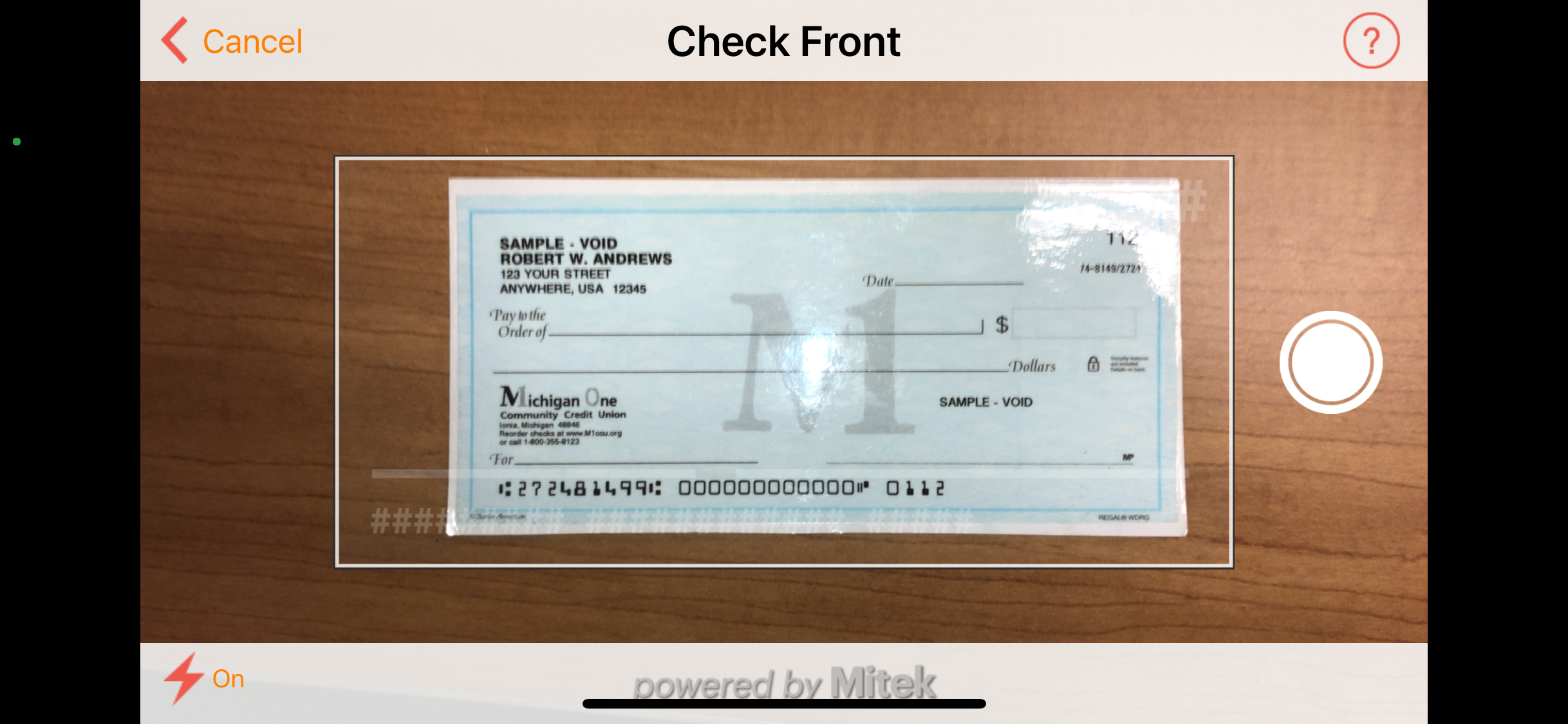

Mobile Check Deposit

One of the most popular forms of e-deposit, mobile check deposit allows users to deposit a physical check into their bank account using their smartphone or tablet. The process typically involves:

- Capturing Images: The user takes photos of the front and back of the endorsed check using their mobile banking app.

- Data Extraction: The app uses optical character recognition (OCR) technology to extract the necessary information from the check images, such as the routing and account numbers, and the amount.

- Verification: The app verifies the image quality and checks for any signs of tampering.

- Transmission: The digitized check information is securely transmitted to the bank for processing.

- Funds Availability: Funds are typically made available within a specified timeframe, often the next business day, subject to the bank’s policies.

This method has revolutionized personal banking, making check deposits as simple as taking a photo.

Direct Deposit

Direct deposit is a fundamental e-deposit method used for recurring payments, such as payroll, government benefits, and tax refunds. Instead of receiving a paper check, funds are automatically transferred from the payer’s account to the recipient’s account on a scheduled basis. This requires the recipient to provide their bank account and routing numbers to the payer.

- Employer Payroll: Most employees opt for direct deposit for their salaries, ensuring timely and secure payment.

- Government Payments: Social Security benefits, tax refunds, and other government payments are increasingly disbursed via direct deposit.

- Other Recurring Payments: This method can also be used for payments like insurance claims, vendor payments, and other forms of regular income.

Direct deposit is a cornerstone of modern payroll systems and a highly efficient way to manage regular financial inflows.

Wire Transfers

Wire transfers are electronic funds transfers that move money from one bank account to another through a network of banks. They are often used for larger or time-sensitive transactions, both domestically and internationally.

- Speed: Wire transfers are typically processed on the same day or within 24 hours, making them suitable for urgent payments.

- Security: The process involves stringent verification procedures to ensure the security of the funds.

- Fees: Wire transfers usually incur fees, which can vary depending on the amount and destination of the transfer.

- Information Required: To initiate a wire transfer, specific details are needed, including the recipient’s name and account number, the recipient’s bank’s routing number (for domestic transfers) or SWIFT/BIC code (for international transfers), and sometimes the bank’s address.

While more complex than mobile deposits or direct deposit, wire transfers remain a critical tool for high-value and urgent financial movements.

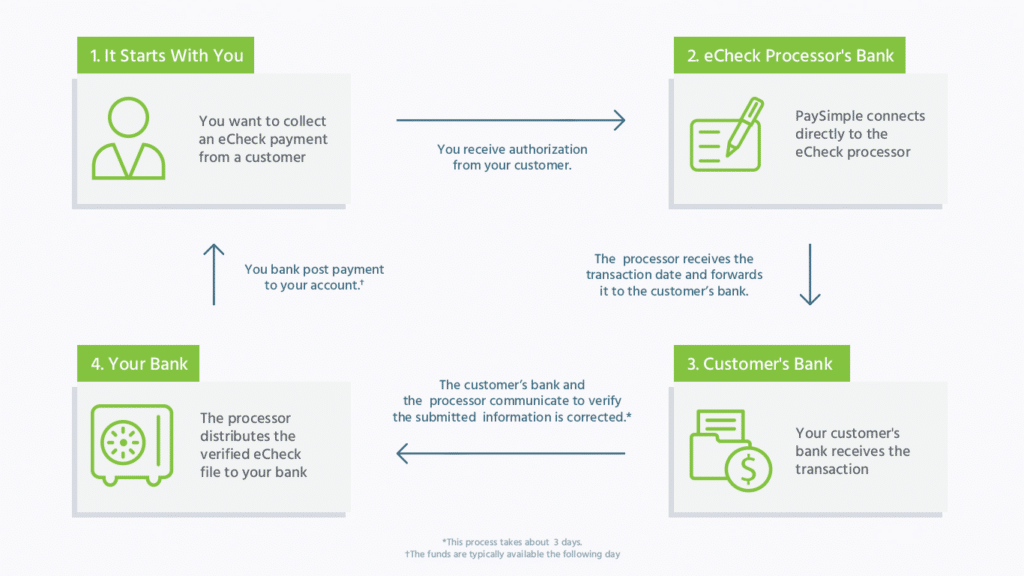

Electronic Funds Transfer (EFT)

EFT is a broad term that encompasses various electronic payment systems. It includes mechanisms for initiating payments and transfers between financial institutions. Direct deposit and wire transfers are specific types of EFT. Other examples include:

- ACH (Automated Clearing House) Network: This network facilitates bulk electronic payments, including direct deposit, business-to-business payments, and bill payments. It is highly efficient for processing a large volume of transactions.

- Online Bill Pay: When you use your bank’s online portal to pay a bill, you are often initiating an EFT. The bank electronically transfers the funds from your account to the biller’s account.

The ACH network, in particular, plays a pivotal role in the everyday functioning of the economy, handling millions of transactions daily.

Digital Wallets and Payment Apps

Platforms like PayPal, Venmo, Zelle, and others facilitate peer-to-peer (P2P) payments and online purchases. While not always directly referred to as “e-deposits” in the traditional banking sense, they function similarly by enabling the transfer of funds electronically between users and into linked bank accounts.

- P2P Transfers: Users can send money to friends and family quickly and easily.

- Online Purchases: These platforms are widely accepted for e-commerce transactions.

- Linking Bank Accounts: Funds can be transferred from the digital wallet to a linked bank account, effectively acting as a form of e-deposit.

These innovative platforms have democratized digital payments, making them accessible to a broader audience.

The Technological Backbone of E-Deposits

The seamless operation of e-deposits relies on a sophisticated interplay of various technologies, primarily within the financial technology (FinTech) sector. These technologies ensure that transactions are processed accurately, securely, and efficiently.

The Role of Banking Networks and Protocols

At the heart of all e-deposits are the secure banking networks that connect financial institutions. These networks facilitate the exchange of financial data and instructions for transferring funds.

- ACH Network: As mentioned, the Automated Clearing House (ACH) network is a critical infrastructure for many types of EFTs in the United States, managed by Nacha. It enables batch processing of transactions.

- SWIFT (Society for Worldwide Interbank Financial Telecommunication): For international wire transfers, SWIFT provides a secure messaging system used by banks worldwide to communicate financial transaction information.

- Proprietary Networks: Banks also utilize their own internal systems and networks to manage transactions between their customers.

These networks are designed with robust security features and protocols to prevent unauthorized access and ensure data integrity.

Data Encryption and Cybersecurity

Cybersecurity is paramount in the realm of e-deposits. Various encryption techniques and cybersecurity measures are employed to safeguard sensitive financial information:

- SSL/TLS Encryption: Secure Sockets Layer (SSL) and Transport Layer Security (TLS) protocols are used to encrypt data transmitted between a user’s device and the bank’s servers, particularly during online and mobile banking sessions.

- Tokenization: This process replaces sensitive data with unique identifiers (tokens). If a token is compromised, it is essentially useless without the corresponding key to de-tokenize it. This is commonly used in mobile payment systems.

- Firewalls and Intrusion Detection Systems: These technologies act as barriers to prevent unauthorized access to banking systems and monitor for suspicious activity.

The continuous advancement of cybersecurity threats necessitates ongoing investment and innovation in these protective measures.

Artificial Intelligence and Machine Learning in Fraud Prevention

AI and machine learning are increasingly integral to e-deposit security. These technologies analyze vast datasets to identify and prevent fraudulent transactions:

- Behavioral Analysis: AI can learn normal transaction patterns for individual users and flag deviations that might indicate fraud.

- Anomaly Detection: ML algorithms can identify unusual transaction amounts, locations, or frequencies that fall outside typical parameters.

- Risk Scoring: Transactions are often assigned a risk score based on various factors, allowing banks to prioritize scrutiny on higher-risk transactions.

The proactive nature of AI in fraud detection significantly enhances the security of e-deposits.

The Future of E-Deposits

The evolution of e-deposits is far from over. Innovations in financial technology continue to push the boundaries of speed, security, and convenience, promising even more integrated and seamless financial experiences.

Real-Time Payments and Faster Funds Availability

The trend towards real-time payments is a significant development. Systems like The Clearing House’s RTP® network and FedNow® Service in the United States are enabling instant settlement of funds, making e-deposits available in seconds rather than hours or days. This will dramatically improve liquidity for businesses and individuals, enabling more dynamic financial management.

Blockchain and Distributed Ledger Technology (DLT)

While still in its nascent stages for mainstream banking, blockchain technology holds the potential to revolutionize e-deposits by offering enhanced security, transparency, and immutability. DLT could enable more direct and secure peer-to-peer transfers without intermediaries, potentially reducing transaction costs and settlement times.

Biometric Authentication and Enhanced Security

The integration of advanced biometric authentication methods, such as facial recognition, fingerprint scanning, and voice recognition, will further enhance the security of e-deposits. These methods offer a more secure and user-friendly alternative to traditional passwords and PINs.

Increased Integration with Digital Ecosystems

E-deposits will become even more deeply embedded within broader digital ecosystems. This includes seamless integration with e-commerce platforms, investment apps, and other financial management tools, creating a more unified and intuitive financial experience for users.

In conclusion, e-deposits represent a fundamental shift in how financial transactions are conducted, moving towards a more digital, efficient, and accessible future. From the convenience of mobile check deposit to the speed of real-time payments, these electronic transfers are reshaping personal and business finance, underpinned by robust security measures and continuous technological innovation. As technology advances, the scope and sophistication of e-deposits will only continue to grow, further solidifying their position as an indispensable component of modern financial infrastructure.