In the realm of drone acquisition and financing, understanding the financial terminology is paramount. Two terms that frequently surface, often causing confusion, are “rate” and “APR” (Annual Percentage Rate). While both relate to the cost of borrowing money, they represent distinct concepts, and grasping their differences can significantly impact your financial decisions. This article will dissect these terms, focusing specifically on their implications within the drone industry, from purchasing personal FPV rigs to acquiring professional aerial surveying equipment.

Understanding the ‘Rate’: The Simple Interest Calculation

When you encounter the term “rate” in a loan or financing agreement for drone equipment, it most commonly refers to the nominal interest rate. This is the stated percentage of the principal loan amount that will be charged as interest over a specific period, typically annually. It’s the fundamental building block of any interest calculation.

Nominal vs. Effective Interest Rate

It’s important to distinguish between a nominal interest rate and an effective interest rate, though in many consumer-level drone financing scenarios, they are presented as one and the same, with the emphasis being on the stated annual figure.

- Nominal Interest Rate: This is the stated interest rate without considering the effect of compounding. If a loan has a 10% annual interest rate, the nominal rate is 10%.

- Effective Interest Rate: This rate takes into account the effects of compounding interest. If interest is compounded more frequently than annually (e.g., monthly or quarterly), the effective rate will be slightly higher than the nominal rate. For most consumer drone financing, the compounding is usually annual or simply calculated on the outstanding principal, making the nominal rate the primary figure presented.

How the Rate Impacts Drone Purchases

Imagine you’re eyeing a professional-grade cinema drone costing $10,000. A lender offers financing with a 5% annual interest rate. This 5% is the rate. If it’s a simple interest loan, you would calculate the annual interest as $10,000 * 0.05 = $500. Over a one-year term, you’d pay back $10,500.

However, the complexity arises when you consider the repayment schedule. If you’re making monthly payments, the calculation becomes more nuanced. The simple “rate” doesn’t fully encapsulate the total cost of borrowing, especially when fees are involved. This is where APR becomes crucial.

The Rate in Context: Equipment Loans and Leases

For businesses or serious hobbyists looking to acquire advanced drone technology, like high-end mapping drones or sophisticated FPV racing setups, financing options are abundant. These often come with a quoted interest rate. Understanding this rate is the first step in evaluating a loan or lease.

- Loan Interest Rate: This is the percentage charged on the outstanding principal balance of a loan taken out to purchase drone equipment.

- Lease Interest Rate: In a lease agreement, this is the implicit interest charged on the residual value of the drone and the financing of your payments. While not always explicitly stated as a percentage, it’s factored into the monthly lease payment.

The “rate” alone can be misleading if not considered alongside the loan term, repayment structure, and any associated fees. It’s a foundational piece of information but not the complete picture of borrowing costs.

Delving into APR: The True Cost of Borrowing

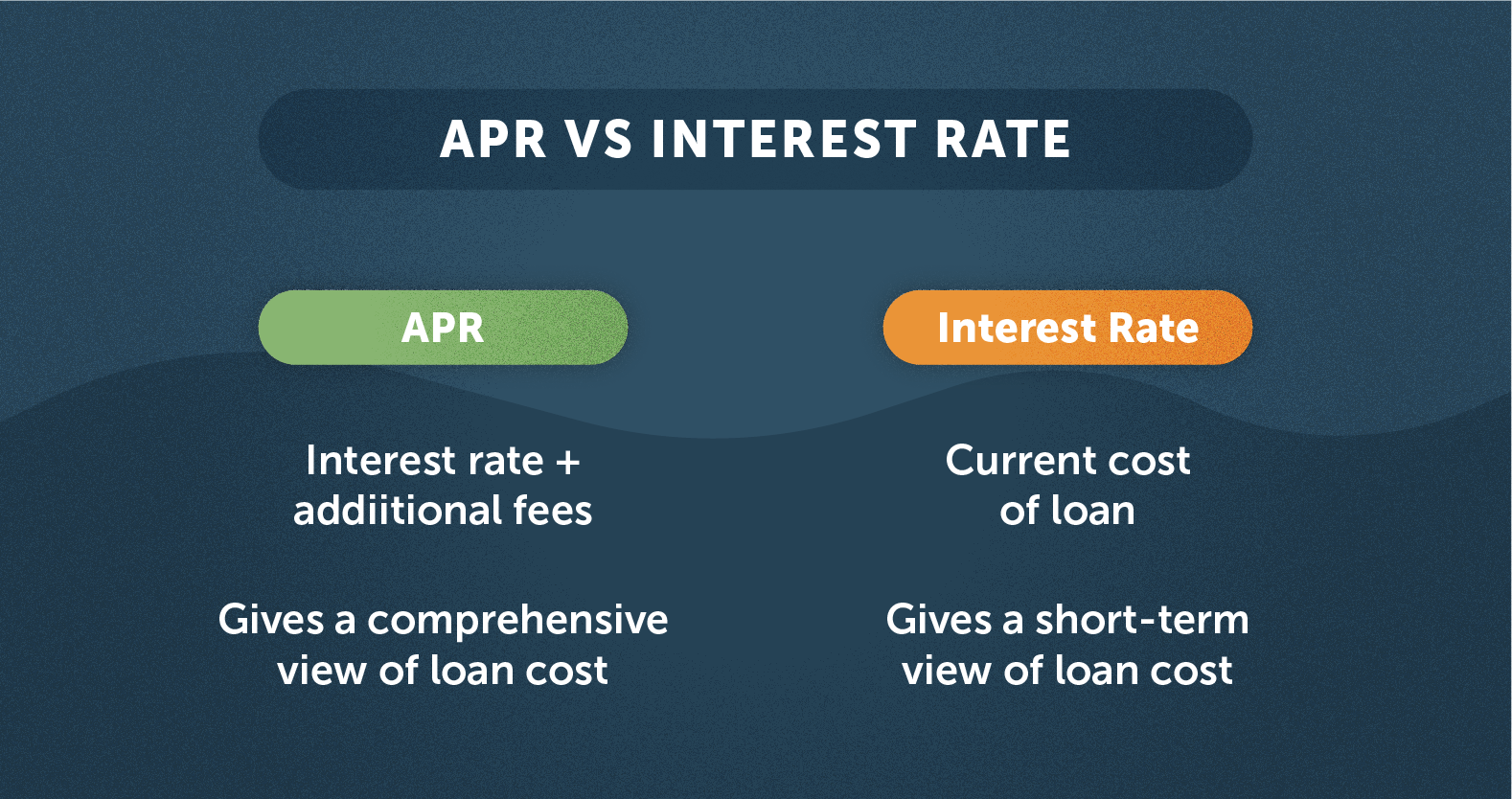

APR, or Annual Percentage Rate, is a more comprehensive measure of the cost of borrowing. It takes the simple interest rate and adds to it most of the fees and other charges associated with obtaining a loan or credit. This provides a more accurate representation of the total expense you’ll incur to finance your drone purchase.

Components of APR

The specific fees included in APR can vary slightly by lender and jurisdiction, but generally, they encompass:

- Interest: The core cost of borrowing, calculated based on the nominal interest rate.

- Origination Fees: Fees charged by the lender to process the loan application.

- Discount Points: Fees paid directly to the lender at closing in exchange for a reduced interest rate. (Less common in consumer drone financing but possible for large commercial acquisitions).

- Underwriting Fees: Costs associated with evaluating the borrower’s creditworthiness.

- Processing Fees: Charges for administrative tasks related to the loan.

- Mortgage Broker Fees: If a broker is involved in arranging the financing.

- Certain Closing Costs: Specific costs related to the loan closing that are mandated by the lender.

It’s crucial to note that not all costs are included in APR. For example, late payment fees, annual fees (on credit cards that might be used for purchase), or costs associated with default are typically excluded.

Why APR Matters for Drone Financing

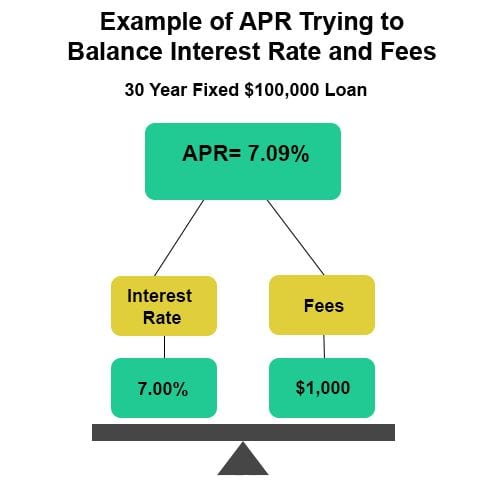

Let’s revisit our $10,000 drone example. Suppose the lender quotes a 5% interest rate. However, they also charge a $200 origination fee and a $50 processing fee. If the loan term is one year, these fees, when spread over the year, will increase the overall cost of borrowing beyond just the 5% interest.

The APR calculation attempts to annualize these upfront fees and divide them by the amount borrowed. While the precise calculation can be complex, the result is a single percentage that reflects the true annual cost of the loan, including these additional charges. If the APR comes out to be 7%, it means that after accounting for the interest and fees, the loan is effectively costing you 7% per year.

APR in Different Drone Financing Scenarios

- Consumer Loans for Hobby Drones: When purchasing a consumer-grade drone for personal use, you might encounter personal loans or even credit card financing. The APR on these will reflect the interest rate plus any associated account fees. A credit card with a high APR might make financing a $1,000 drone very expensive over time.

- Business Loans for Commercial Drones: For businesses acquiring expensive aerial photography drones, mapping drones, or delivery drones, commercial loans will have an APR that includes not just the interest but also origination fees, underwriting charges, and other administrative costs associated with securing a significant business loan.

- Leasing Agreements: While leases often present a monthly payment, the underlying financing costs are factored into the lease’s effective APR. Understanding this helps compare leasing versus buying.

The APR provides a standardized metric for comparing different loan offers. If Lender A offers a loan with a 5% rate and $500 in fees, and Lender B offers a 6% rate with $100 in fees, comparing their APRs will reveal which is truly the cheaper option.

The Interplay Between Rate and APR

The nominal interest rate is a component of APR. Think of the rate as the base price, and APR as the all-in price after adding mandatory service charges and taxes. The APR will always be equal to or higher than the nominal interest rate.

When the Rate and APR are Similar

In some straightforward loan structures, particularly those with minimal fees or where fees are very small relative to the loan amount and term, the APR might be very close to the nominal interest rate. For instance, a personal loan for a small drone with no origination or processing fees might have an APR that is almost identical to its stated interest rate.

When the Difference Becomes Significant

The divergence between the rate and APR becomes more pronounced in loans with:

- Higher Fees: Larger origination fees, underwriting charges, or processing costs will inflate the APR.

- Shorter Loan Terms: Fees are spread over fewer payments, making their annual impact greater.

- Smaller Loan Amounts: The fixed cost of fees represents a larger percentage of a smaller principal.

For example, financing a $500 drone with a $100 origination fee and a 6% nominal interest rate over one year will result in a significantly higher APR than if the same loan were for $10,000. The $100 fee, which is 20% of the loan amount, will substantially boost the APR beyond the 6% interest.

Navigating Drone Financing with APR

When evaluating financing options for any drone-related purchase, from a beginner drone to a complex industrial UAV system, always prioritize the APR.

Key Takeaways for Drone Buyers:

- Always Ask for the APR: Don’t just focus on the stated interest rate. Request the APR for any loan or credit offer.

- Compare APRs: Use APR as your primary tool for comparing different financing deals from various lenders or providers.

- Read the Fine Print: Understand what fees are included in the APR and what potential costs are excluded.

- Consider the Loan Term: A lower rate or APR might not always be the best deal if the loan term is excessively long, leading to more interest paid over time.

- Factor in Your Financial Goals: Are you looking for the lowest monthly payment, or the lowest total cost of borrowing? APR helps with the latter.

By understanding the distinction between rate and APR, and consistently using APR as your benchmark, you can make more informed and cost-effective decisions when financing your next drone purchase, ensuring you invest wisely in the technology that powers your aerial ambitions.