When navigating the complex landscape of financial obligations, particularly in the realm of loans, understanding specific terminology is paramount. Two terms that frequently surface, often causing confusion, are “forbearance” and “deferment.” While both offer temporary relief from immediate repayment, their mechanisms, implications, and suitability for different financial situations diverge significantly. This distinction is crucial for borrowers seeking to manage their financial health proactively and make informed decisions that align with their long-term goals. This exploration delves into the core differences, practical applications, and potential consequences of each, providing a clear framework for understanding these vital financial tools.

Understanding Loan Repayment Options

At their core, both forbearance and deferment are lender-granted concessions that allow a borrower to temporarily pause or reduce their loan payments. They are typically offered when a borrower encounters financial hardship, such as job loss, illness, or other unforeseen circumstances that impact their ability to meet their regular payment obligations. However, the underlying mechanics and the impact on the loan’s total cost and repayment timeline are where the critical differences lie. Recognizing these nuances empowers borrowers to choose the option that best mitigates immediate financial strain without inadvertently exacerbating their long-term debt burden.

The Nature of Forbearance

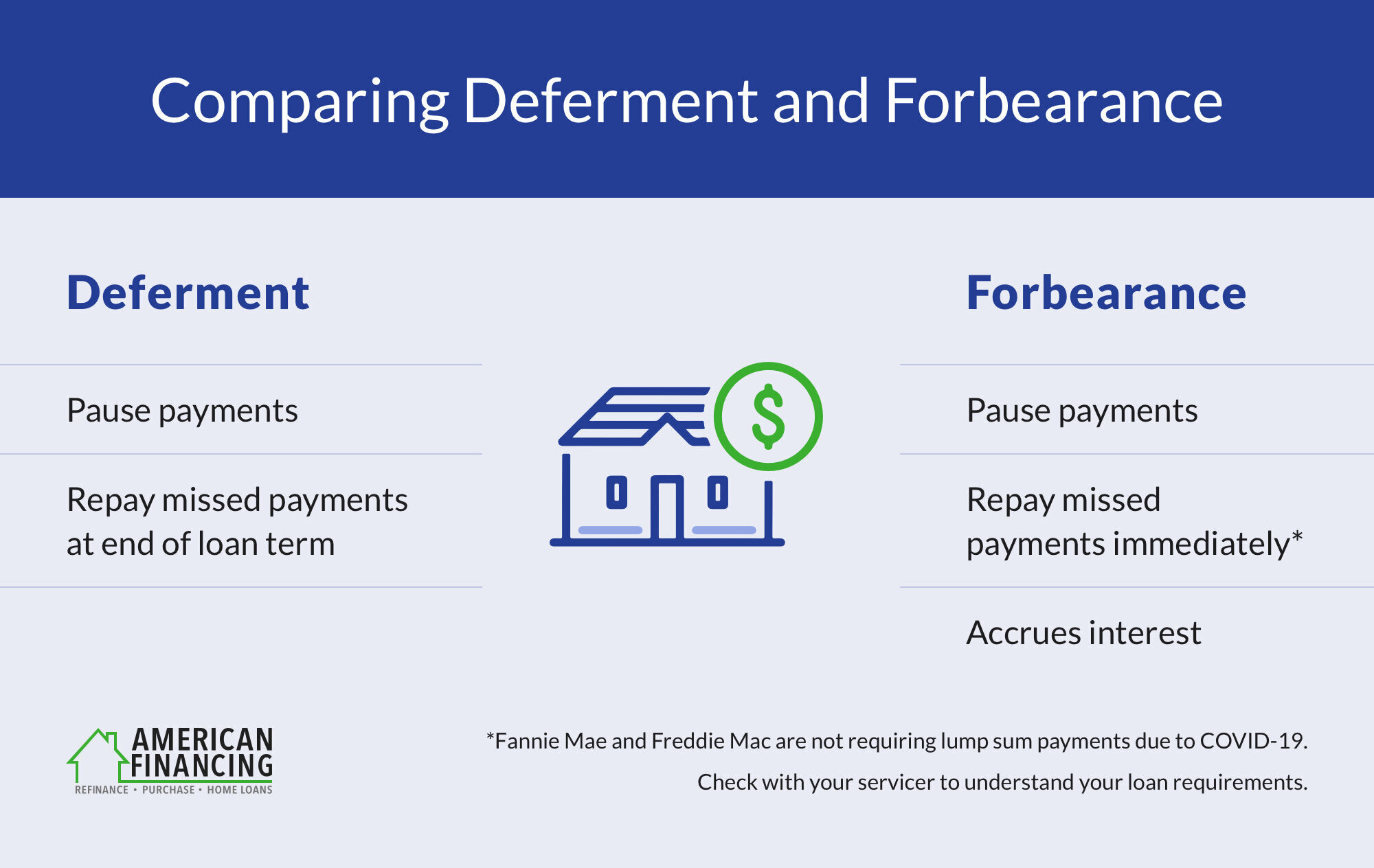

Forbearance is essentially a temporary suspension or reduction of loan payments. During a forbearance period, a borrower might be allowed to:

- Make reduced payments: Instead of the full monthly installment, the borrower might be permitted to pay a smaller amount.

- Temporarily suspend payments altogether: In some cases, payments can be halted for a specified duration.

The key characteristic of forbearance is that interest typically continues to accrue on the outstanding loan balance during the forbearance period, even if no payments are being made. This is a critical point that distinguishes it from deferment in many scenarios. The accrued interest may then be added to the principal balance (capitalized) at the end of the forbearance, leading to a higher overall debt amount and potentially increased monthly payments once repayment resumes.

Forbearance is often a more flexible option, allowing for a degree of payment reduction rather than a complete halt. This can be beneficial for individuals who can afford to make some payment, even if it’s less than their usual amount, thereby slowing down the accumulation of interest compared to a full pause. Lenders may grant forbearance for various reasons, and the terms can be negotiated to some extent, although the overarching principle of continued interest accrual usually remains.

The Nature of Deferment

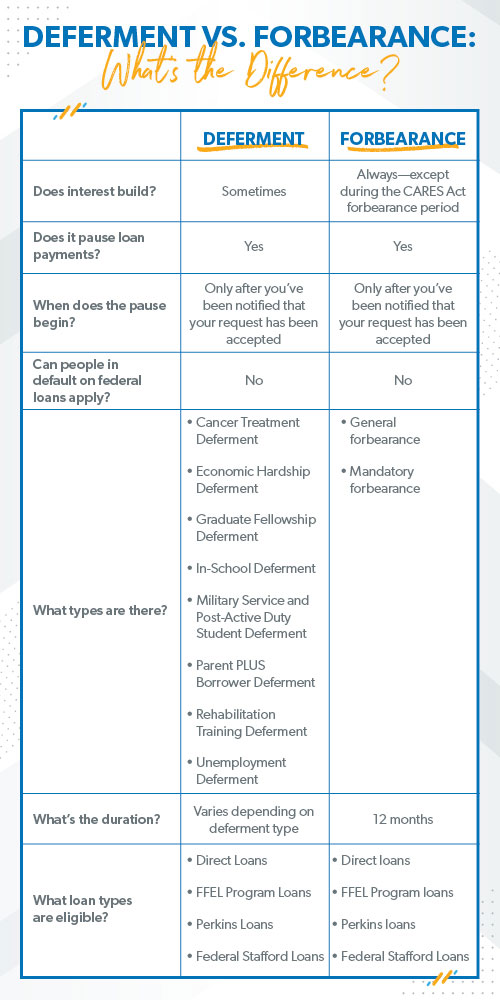

Deferment, on the other hand, is a period during which a borrower is granted a formal postponement of loan payments. Unlike forbearance, in many types of deferment, interest may not accrue on the loan balance during the deferment period. This is particularly common for certain types of federal student loans, where the government subsidizes the interest during periods of deferment. However, it’s crucial to note that this is not universally true for all loans; some deferments may still accrue interest, which is then capitalized at the end of the deferment period.

During a deferment, the borrower is explicitly not required to make any payments for a specified timeframe. This provides a more complete break from immediate financial obligations. Deferment is typically offered for specific qualifying circumstances, such as:

- Enrollment in school: For student loans, returning to school at least half-time often qualifies for deferment.

- Unemployment: Periods of joblessness can be grounds for deferment.

- Economic hardship: Certain documented financial difficulties may lead to deferment.

- Military service: Active duty service can qualify for deferment.

The primary advantage of deferment, especially when interest is not accruing, is that it prevents the loan balance from increasing due to unpaid interest during the pause. This can significantly impact the total amount repaid over the life of the loan.

Key Distinctions and Implications

The divergence between forbearance and deferment becomes most apparent when examining their impact on the loan’s total cost and the borrower’s future repayment obligations.

Interest Accrual: The Defining Factor

The most significant difference lies in how interest is handled.

- Forbearance: Interest generally continues to accrue on the outstanding principal balance. At the end of the forbearance period, this accrued interest is often added to the principal, increasing the total amount owed and potentially leading to higher future payments.

- Deferment: For many types of loans, particularly federal student loans, interest may not accrue during the deferment period. If interest does accrue, it might be subsidized by the government or the lender, or it might be capitalized at the end, similar to forbearance, depending on the loan type and specific agreement. The key is that the borrower is not required to pay this interest during the deferment, and in many cases, it is not added to the principal balance.

Impact on Loan Balance and Future Payments

The treatment of interest directly affects the loan balance.

- Forbearance: Because interest accrues and may be capitalized, a forbearance typically results in a higher total loan balance at the end of the relief period. This can translate into higher monthly payments when repayment resumes or a longer repayment term.

- Deferment: When interest is not accrued or is subsidized, a deferment generally has a less detrimental impact on the overall loan balance. The loan balance may remain static or increase minimally, leading to more predictable future payments.

Eligibility and Application

The criteria for obtaining forbearance and deferment can also differ.

- Forbearance: Often more readily available and may require less stringent documentation. Lenders might offer forbearance as a more immediate solution to temporary cash flow issues.

- Deferment: Typically has more specific eligibility requirements tied to particular life events or statuses, such as being enrolled in school or experiencing prolonged unemployment. The application process might involve providing proof to satisfy these conditions.

Loan Types

It’s important to recognize that the availability and specific terms of forbearance and deferment are heavily dependent on the type of loan.

- Federal Student Loans: These loans often have clearly defined options for both forbearance and deferment, with specific rules regarding interest accrual and eligibility. For instance, subsidized federal loans may have interest covered during deferment, while unsubsidized loans might accrue interest that is then capitalized.

- Private Loans: Forbearance and deferment options for private loans can vary significantly by lender and loan agreement. They may be less standardized and could be more negotiable, but often come with a higher likelihood of continued interest accrual.

- Mortgages: Forbearance programs for mortgages, especially those established under government initiatives (like during economic crises), allow homeowners to temporarily pause or reduce payments. Interest typically continues to accrue, and the missed payments are often added to the end of the loan term or repaid over time.

- Auto Loans: Similar to mortgages, auto loan forbearance typically allows for a temporary pause or reduction in payments, with interest usually continuing to accrue.

Strategic Considerations for Borrowers

When facing financial strain, the choice between forbearance and deferment is not merely a matter of temporary relief but a strategic decision with long-term financial consequences.

When to Consider Forbearance

Forbearance might be the preferred option in situations where:

- Short-term, predictable hardship: If the financial difficulty is expected to be short-lived and the borrower anticipates being able to resume full payments relatively soon.

- Ability to make partial payments: If the borrower can afford to make some payment, even if it’s reduced, this can help mitigate the accumulation of interest compared to a complete payment halt.

- Limited deferment options: If the borrower does not meet the specific eligibility criteria for deferment for their particular loan type.

- Need for immediate flexibility: Forbearance can sometimes be obtained more quickly than deferment, providing faster relief in urgent situations.

However, borrowers must be acutely aware of the potential for increased total debt due to capitalized interest. It is essential to understand the exact terms of the forbearance, including how interest will be handled and what the repayment will look like afterward.

When to Consider Deferment

Deferment is often the more advantageous choice when:

- Eligibility criteria are met: If the borrower qualifies for deferment based on specific circumstances (e.g., returning to school, unemployment).

- Interest is not accruing or is subsidized: This is the primary benefit, as it prevents the loan balance from growing during the pause.

- Longer-term financial challenges: If the financial hardship is anticipated to last for a more extended period, deferment provides a more substantial break from repayment obligations.

- Minimizing total loan cost: For loans where deferment avoids interest accrual, it is generally the more cost-effective option in the long run.

Borrowers should always confirm the specific conditions of the deferment, particularly regarding interest accrual and any grace periods or repayment adjustments that may occur upon its conclusion.

Navigating the Process and Seeking Advice

Regardless of whether forbearance or deferment is being considered, thorough understanding and proactive communication with the lender are essential.

The Application and Approval Process

- Contact Your Lender: The first step is always to reach out to your loan servicer or lender to discuss your financial situation.

- Inquire About Options: Clearly ask about both forbearance and deferment options available for your specific loan.

- Understand the Terms: Do not agree to any arrangement without fully understanding the terms, including the duration, payment amounts (if any), interest accrual, and what happens when the period ends.

- Provide Documentation: Be prepared to provide any necessary documentation to support your request, such as proof of income loss, school enrollment, or medical condition.

- Get it in Writing: Ensure all agreed-upon terms are provided in writing.

The Importance of Professional Guidance

Given the intricate nature of loan terms and their long-term implications, seeking professional financial advice can be invaluable.

- Financial Advisors: A qualified financial advisor can help assess your overall financial picture, evaluate the potential impact of forbearance versus deferment on your long-term financial health, and guide you toward the most prudent decision.

- Credit Counselors: Non-profit credit counseling agencies can offer guidance on managing debt, understanding loan options, and navigating the complexities of financial hardship.

- Loan Servicer Representatives: While lenders’ representatives can explain their products, remember they are employed by the lender. It’s wise to cross-reference information and seek independent advice to ensure your interests are fully considered.

By understanding the fundamental differences between forbearance and deferment, borrowers can make more informed choices during challenging financial times, safeguarding their financial future and navigating the path to responsible debt management with clarity and confidence.