The cryptic three or four-digit number gracing the back or front of your payment card, often referred to as the CVV (Card Verification Value), CVV2, CVC (Card Verification Code), or CID (Card Identification Number), plays a surprisingly significant role in the intricate ecosystem of online transactions. While it might seem like a mere alphanumeric sequence, its presence and function are fundamental to enhancing security and mitigating the risks associated with the burgeoning digital marketplace. Understanding the CVV is not just about knowing what it is, but also about appreciating its security implications and how it contributes to a safer online shopping experience.

The core purpose of the CVV is to act as a security measure, primarily to combat fraud in “card-not-present” (CNP) transactions. These are purchases made where the physical card isn’t swiped or inserted into a terminal, such as when buying goods or services online, over the phone, or through mail order. In these scenarios, the CVV provides an additional layer of verification that helps assure the merchant that the person making the purchase is in physical possession of the card. This is a crucial distinction, as unlike the magnetic stripe or chip, the CVV is not stored on the card’s data carriers for point-of-sale transactions. Instead, it’s a code generated by the card issuer and imprinted on the physical card itself.

The Genesis and Purpose of the CVV

The concept of the CVV emerged from a growing need to bolster the security of credit and debit card transactions. As e-commerce began its ascent, so too did the opportunities for fraudulent activities. Without a way to physically verify the cardholder, merchants were vulnerable to individuals who obtained card numbers through illicit means but did not possess the actual card. The CVV was developed as a response to this challenge, offering a dynamic security feature that, when combined with other cardholder data, could significantly reduce the likelihood of fraudulent transactions.

Card-Not-Present (CNP) Transactions: The CVV’s Primary Domain

The vast majority of CVV usage occurs within the realm of CNP transactions. When you enter your card details online, after the card number and expiration date, you’ll invariably be prompted for this three or four-digit code. The reason for this repeated request, even if you’ve shopped at the same merchant before, is that the CVV is intentionally not stored by merchants after the transaction is authorized. This is a critical security protocol mandated by the Payment Card Industry Data Security Standard (PCI DSS). By not storing this sensitive information, merchants significantly reduce their liability in the event of a data breach. If a merchant’s database is compromised, criminals would not find the CVV codes of past transactions, rendering them largely useless for further fraudulent CNP purchases.

Beyond CNP: Other Applications of the CVV

While CNP transactions are the most prominent use case, the CVV can also be employed in other verification scenarios. For instance, a customer service representative taking an order over the phone might ask for the CVV to confirm your identity as the legitimate cardholder. In some cases, it might be used for recurring billing setups to re-verify the cardholder’s intent to continue the subscription, though this is less common than its use in initial transaction authorization.

Decoding the CVV: Where It’s Found and What It Means

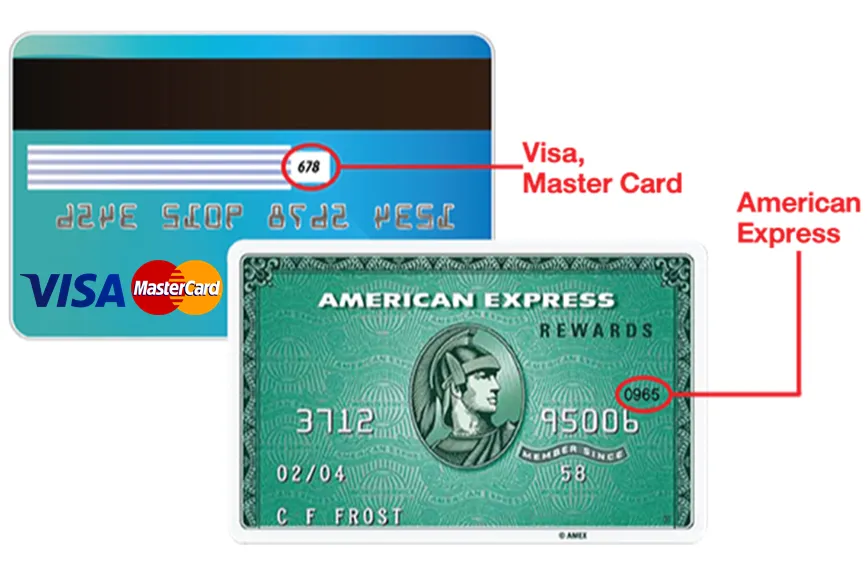

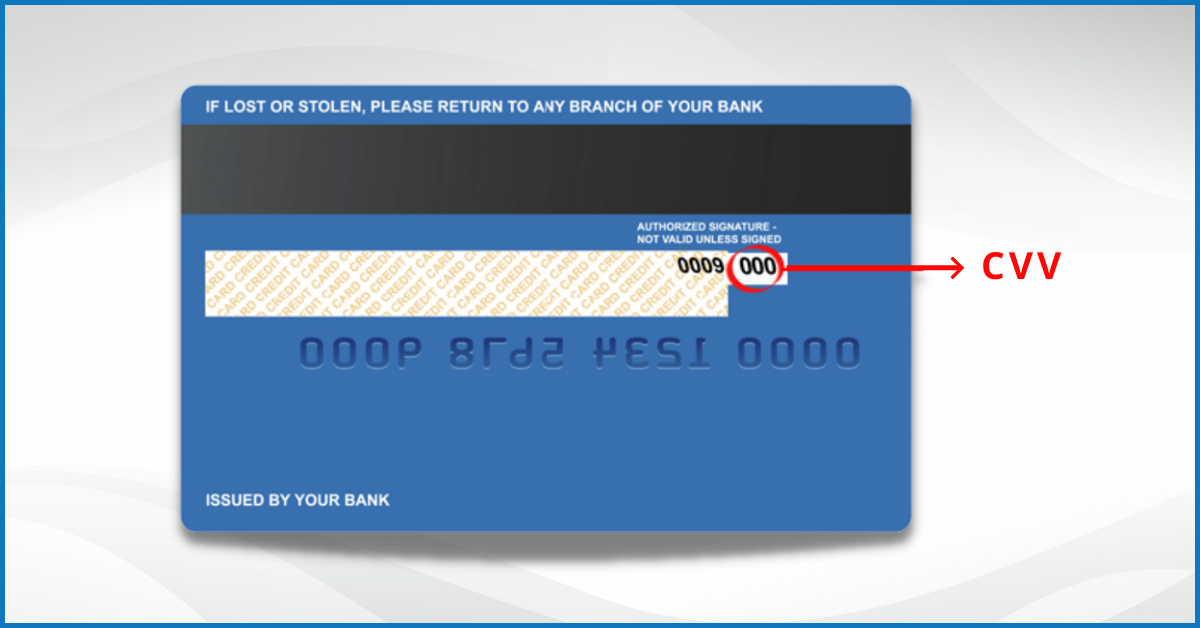

The physical location of the CVV depends on the type of card you possess. For most Visa, Discover, and Mastercard branded cards, the CVV is a three-digit number printed on the back of the card, typically in the signature area. American Express cards, however, are a notable exception. Their Card Identification Number (CID), which serves the same security purpose, is a four-digit code printed on the front of the card, above the embossed account number.

The Three-Digit CVV2 (Visa, Mastercard, Discover)

The most commonly encountered CVV is the three-digit code found on the back of Visa, Mastercard, and Discover cards. This number is not embossed like the card number or expiration date, which means it’s not part of the information captured by a physical card imprinter. This subtle but important difference further enhances its security, as it cannot be automatically duplicated during a standard physical transaction. The three digits are dynamically generated by the card issuer and are unique to each card.

The Four-Digit CID (American Express)

American Express employs a four-digit Card Identification Number (CID). Unlike the other major networks, this code is located on the front of the card. This placement is a design choice specific to American Express and does not diminish the security function of the number. It remains a critical component for verifying cardholder authenticity in CNP transactions.

The Significance of the Code’s Imprint

The fact that the CVV is typically printed and not embossed is a key security feature. Embossing is a raised print that allows for easy duplication with carbon paper or imprinting machines. Since the CVV is not embossed, it cannot be easily captured during traditional physical transactions where an imprinter might be used. This means that even if a criminal were to physically get their hands on your card and use an imprinter, they would not be able to obtain the CVV. This limitation forces fraudsters to rely on more sophisticated methods of data theft for CNP fraud.

The Technical Underpinnings of CVV Security

While the user sees the CVV as a simple number, its security is rooted in robust cryptographic principles and stringent industry standards. The process by which the CVV is generated, transmitted, and verified is designed to be highly secure, although no system is entirely impervious to all forms of attack.

Generation and Issuance by Card Networks and Banks

The CVV is generated by the card issuer (the bank or financial institution that issued the card) and is typically a service provided by the card networks like Visa or Mastercard. The algorithms used for generation are proprietary and complex, ensuring that the code is unique and not easily predictable. When a card is manufactured, this unique CVV is imprinted on the physical card. This process is carefully managed to ensure that the CVV is associated with the correct card number and expiration date.

The Verification Process: A Real-Time Exchange

During an online transaction, when a customer enters their card number, expiration date, and CVV, this information is sent to the acquiring bank, which then forwards it through the card network to the issuing bank for authorization. The issuing bank’s system then performs a critical check: it verifies that the provided CVV matches the one on file for that specific card number. If the CVVs match, and the other transaction details are valid, the transaction is approved. If they do not match, the transaction is typically declined. This real-time verification is the linchpin of CVV security.

PCI DSS: The Regulatory Backbone

The security protocols surrounding the CVV are heavily influenced by the Payment Card Industry Data Security Standard (PCI DSS). This set of security standards is designed to protect cardholder data. A key requirement of PCI DSS is that merchants are prohibited from storing CVV data after transaction authorization. This restriction is paramount because it means that if a merchant’s systems are compromised, the CVVs from previous transactions are not exposed. This significantly limits the usefulness of stolen card numbers in perpetrating further online fraud. Compliance with PCI DSS is mandatory for all entities that store, process, or transmit cardholder data.

Best Practices for Protecting Your CVV

While the CVV is a powerful security tool, its effectiveness relies on responsible usage and diligent protection by cardholders. Treat your CVV with the same level of caution you afford your card number and PIN.

Never Share Your CVV Unnecessarily

The cardinal rule of CVV security is to never share it with anyone who is not a trusted merchant or financial institution, and only when you are initiating a transaction. Be wary of unsolicited requests for your CVV, whether they come via email, text message, or phone call. Legitimate businesses will not ask for your CVV in these unsolicited ways. If you receive such a request, it is almost certainly a phishing attempt.

Be Cautious of Suspicious Websites and Emails

When shopping online, ensure that the website is legitimate and secure. Look for “https://” in the website’s URL and a padlock icon in your browser’s address bar, which indicates an encrypted connection. Phishing websites are designed to look like legitimate sites but are created to steal your personal and financial information, including your CVV. Similarly, be scrutinizing of emails that appear to be from your bank or a retailer; often, they contain links to fake login pages or requests for sensitive information.

Review Your Bank Statements Regularly

A proactive approach to financial security involves regularly reviewing your bank and credit card statements. Look for any unauthorized transactions, no matter how small. If you spot something suspicious, contact your bank or card issuer immediately. Early detection can significantly limit the damage caused by fraudulent activity.

Understand When CVV is Required

Remember that the CVV is primarily for “card-not-present” transactions. For in-person transactions, it is generally not required. If a merchant asks for your CVV for an in-person purchase, this could be a red flag. Similarly, for phone orders, ensure you are speaking to a legitimate representative of a company you trust.

The CVV, often an overlooked detail on our payment cards, is a critical component of modern transaction security. By understanding its purpose, how it’s used, and by diligently protecting it, cardholders contribute to a safer and more secure digital economy. It’s a small number with a significant impact, working silently to safeguard our financial information in an increasingly connected world.