In the realm of real estate and property law, a “deed in lieu of foreclosure” is a significant legal mechanism that allows a borrower to voluntarily transfer ownership of their property to the lender to avoid the more damaging consequences of a formal foreclosure process. This process is essentially a negotiated settlement between the borrower and the lender, where the borrower surrenders the property in exchange for the lender waiving the right to pursue a deficiency judgment. Understanding the intricacies of a deed in lieu is crucial for both borrowers facing financial distress and lenders seeking to mitigate losses.

The Genesis of Deed in Lieu: When Foreclosure Looms

Foreclosure is a legal process initiated by a lender when a borrower defaults on their mortgage payments. It typically involves the lender taking possession of the property and selling it to recoup their losses. This process can be lengthy, costly, and detrimental to all parties involved. For the borrower, foreclosure results in a severely damaged credit score, a permanent mark on their financial history, and the loss of their home. For the lender, foreclosure can entail substantial legal fees, property maintenance costs, and the risk of selling the property for less than the outstanding loan balance.

Recognizing the potential for mutual benefit in avoiding the full foreclosure process, the deed in lieu of foreclosure emerged as a more streamlined and less adversarial alternative. It provides a structured way for a borrower to exit a property they can no longer afford or manage, while simultaneously allowing the lender to regain possession of the property without the full legal and financial burden of a traditional foreclosure.

Defining the Deed in Lieu of Foreclosure

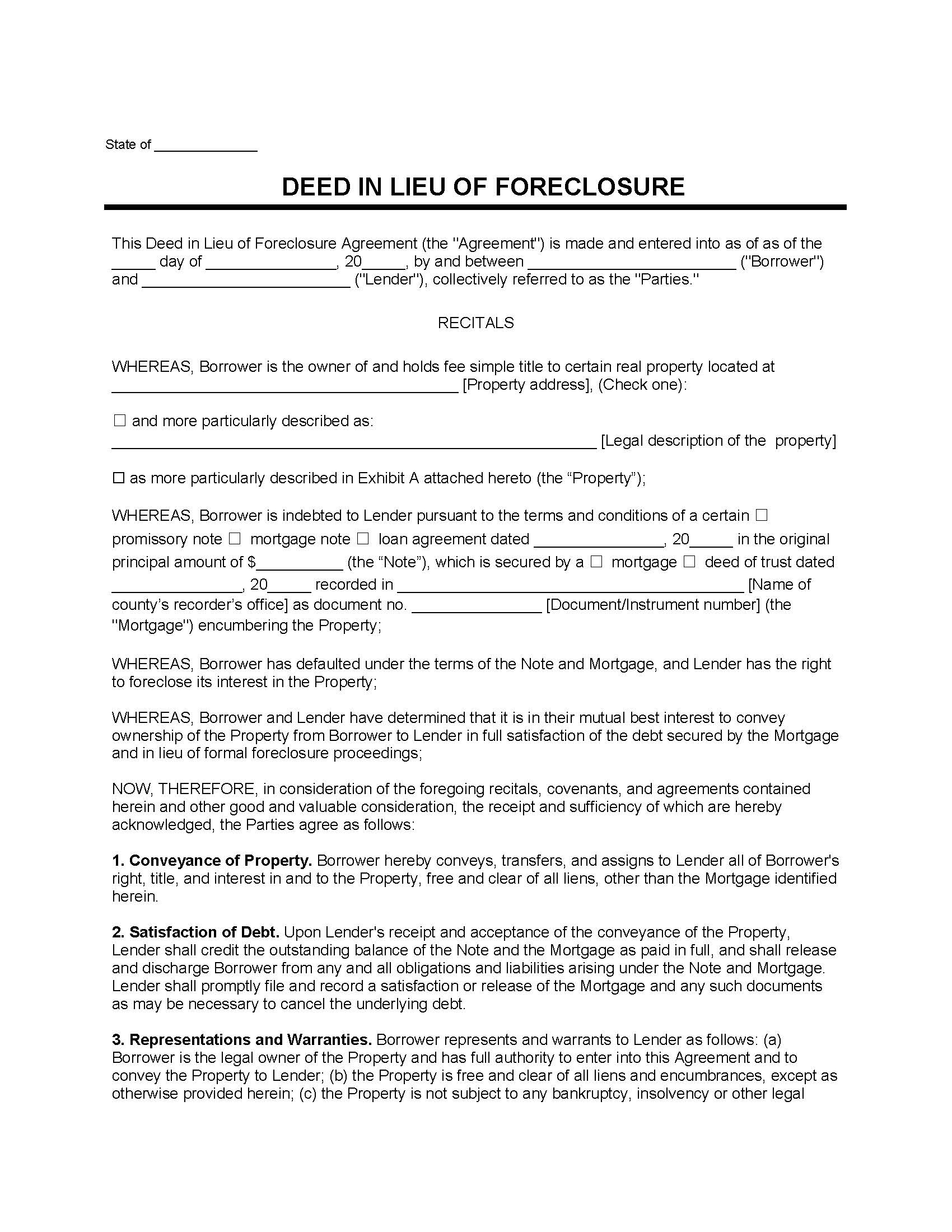

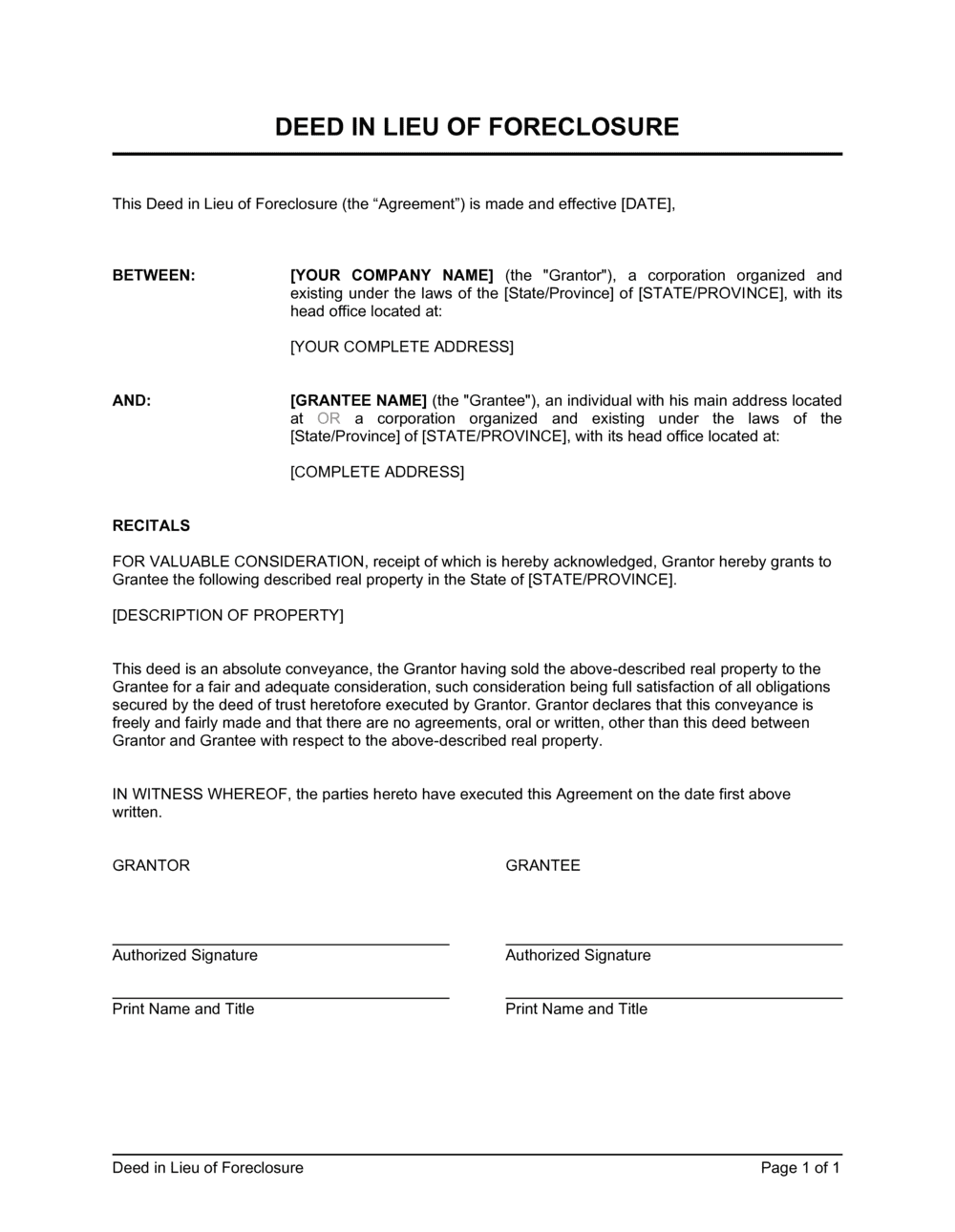

A deed in lieu of foreclosure, often shortened to “deed in lieu,” is a transaction where a borrower, facing or anticipating foreclosure, voluntarily conveys the title of the property to the mortgage lender. This transfer is made as an alternative to the lender initiating or continuing foreclosure proceedings. The fundamental agreement is that the lender accepts the deed and, in return, agrees not to pursue legal action against the borrower for any outstanding debt beyond the value of the property.

This means that if the property’s market value is less than the amount owed on the mortgage, the lender generally cannot sue the borrower for the difference – the “deficiency.” This waiver of the deficiency is a primary incentive for borrowers to consider this option.

Key Players and Their Motivations

The deed in lieu process involves two primary parties: the borrower (the homeowner) and the lender (typically a bank or financial institution).

-

Borrower’s Motivations:

- Credit Protection: A deed in lieu typically has a less severe impact on a borrower’s credit score than a foreclosure. While it will still be reported and affect creditworthiness, it is often viewed more favorably by future lenders than a foreclosure, which can remain on a credit report for seven to ten years.

- Avoiding Legal Action: It offers an escape from the stress and potential legal entanglements of a formal foreclosure.

- Faster Resolution: Compared to the drawn-out foreclosure process, a deed in lieu can often be completed more quickly.

- Emotional Relief: It can provide a sense of closure and relief from the burden of a property that has become financially unmanageable.

-

Lender’s Motivations:

- Reduced Costs: Lenders can save on legal fees, court costs, and other expenses associated with foreclosures.

- Faster Asset Recovery: The lender can take possession of the property sooner, allowing them to market and sell it more quickly, potentially minimizing further depreciation or damage.

- Avoiding Delays: Foreclosures can be subject to significant delays due to court backlogs, borrower defenses, and state-specific regulations.

- Mitigating Risk: It can be a way to avoid the uncertainty of a foreclosure sale, where the property might not fetch a satisfactory price.

The Deed in Lieu Process: A Step-by-Step Approach

While the specifics can vary, a deed in lieu transaction generally follows a defined sequence of events. It is a process that requires careful communication, documentation, and legal counsel.

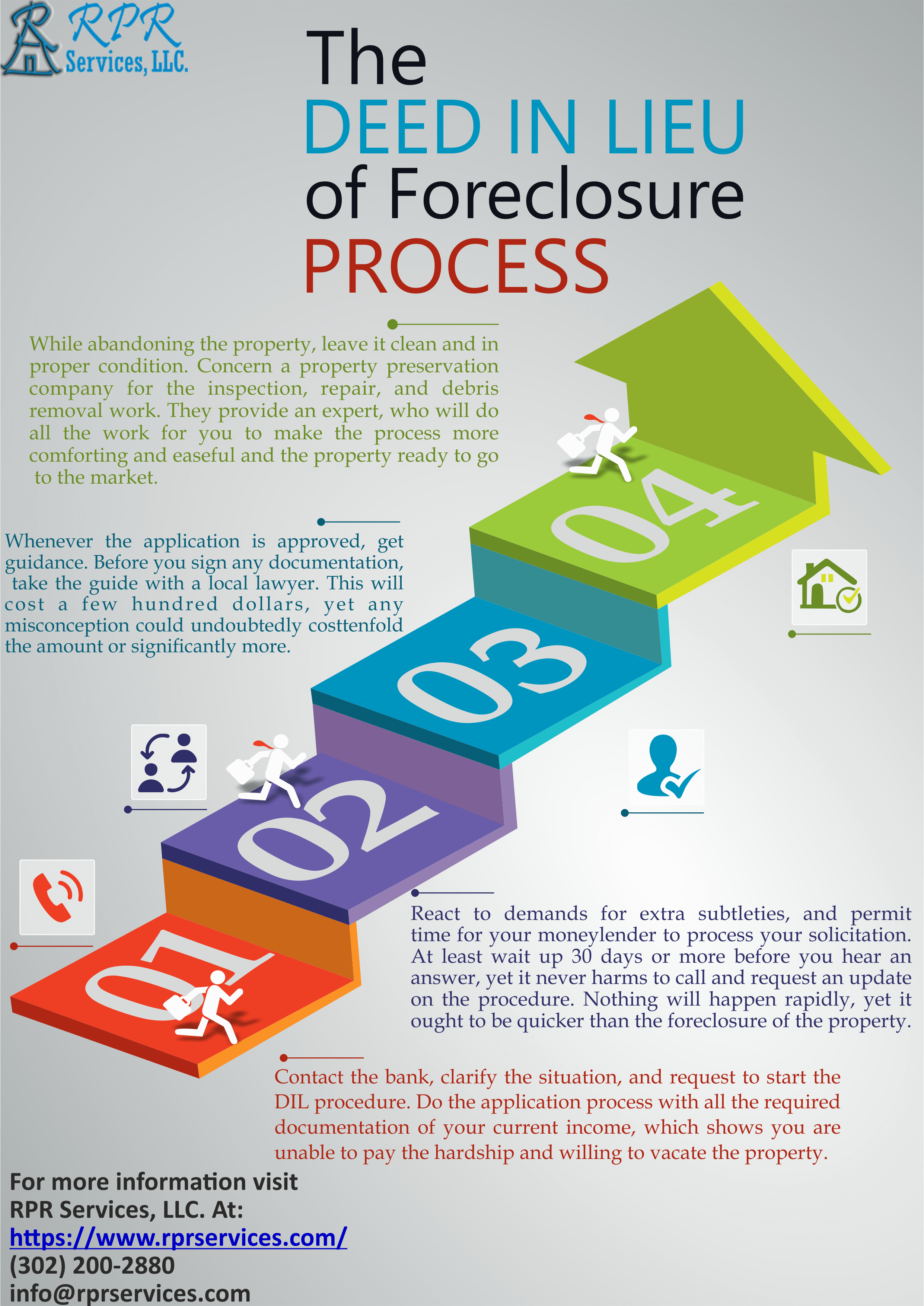

Initial Assessment and Negotiation

The process typically begins when a borrower realizes they cannot meet their mortgage obligations. They will usually contact their lender to discuss their situation and explore options. The lender will then assess the borrower’s financial standing and the property’s value.

- Financial Hardship Documentation: Borrowers are often required to provide detailed documentation of their financial hardship, such as proof of job loss, significant medical expenses, or a reduction in income. This demonstrates that the default is due to circumstances beyond their control.

- Property Valuation: The lender will order an appraisal or Broker Price Opinion (BPO) to determine the current market value of the property. This valuation is critical in determining if the deed in lieu is a viable option. If the property’s value significantly exceeds the outstanding loan balance, the lender may be less inclined to accept a deed in lieu, as they might still be able to recover a substantial portion of the debt through foreclosure.

Formal Agreement and Due Diligence

If both parties agree that a deed in lieu is a mutually beneficial solution, the process moves into more formal stages.

- Loan Modification or Forbearance Review: Before proceeding with a deed in lieu, lenders are often required (or choose) to explore other loss mitigation options, such as loan modification or forbearance, to see if the borrower can be helped to keep the property.

- Deed in Lieu Agreement: A formal agreement is drafted. This document outlines the terms of the transfer, including the waiver of deficiency, any conditions for the borrower to vacate the property, and the lender’s responsibilities. It’s crucial that this agreement clearly states the lender’s relinquishment of the right to pursue a deficiency judgment.

- Title Search and Encumbrance Review: The lender will conduct a thorough title search to ensure there are no other liens or claims against the property that could complicate the transfer or create future liabilities for the lender. Any junior liens (e.g., second mortgages, home equity lines of credit, tax liens) must typically be satisfied or subordinated for the deed in lieu to proceed. The borrower may need to negotiate with these junior lienholders.

Execution and Recording

The final stages involve the legal transfer of ownership.

- Execution of the Deed: The borrower signs a new deed, transferring ownership of the property to the lender. This deed is prepared by the lender’s attorney.

- Recording the Deed: The deed is then recorded with the local county recorder’s office. This public record officially signifies the transfer of ownership from the borrower to the lender.

- Property Vacancy: The borrower is typically required to vacate the property by a specified date, leaving it in good condition.

Conditions and Considerations for a Deed in Lieu

While a deed in lieu offers advantages, it is not always available or suitable for every situation. Several conditions and considerations must be met.

Borrower Eligibility Criteria

Lenders typically have specific criteria for borrowers to qualify for a deed in lieu.

- Financial Hardship: As mentioned, demonstrable financial hardship is usually a prerequisite. This means the borrower can no longer afford the mortgage payments due to circumstances beyond their control, not simply a desire to exit an underwater property without consequence.

- Property Condition: The property must generally be in good condition and free from significant damage or required repairs that would make it unmarketable or undesirable to the lender. Lenders are not typically interested in taking on properties with extensive structural issues.

- No Other Liens (or Subordinated Liens): The existence of multiple liens on the property can make a deed in lieu complex. Lenders prefer a clear title. If there are junior liens, the borrower may need to negotiate with those creditors to release their claims or agree to be paid a small amount from the equity, if any, before the deed in lieu can be finalized.

- Borrower’s Willingness: The borrower must be willing to voluntarily sign over the property.

Lender Requirements and Agreements

Lenders also impose their own requirements and conditions.

- “Arm’s Length” Transaction: The transaction must be an “arm’s length” transaction, meaning it’s conducted fairly and without any undue influence or fraud. The borrower and lender should be acting in their own best interests, and the borrower should not be receiving any undisclosed compensation or benefit from the lender for signing the deed.

- Borrower’s Occupancy: In many cases, the borrower must have occupied the property as their primary residence at the time of the default or for a significant period. Some lenders may have different policies for investment properties.

- No Other Options Explored: Lenders often require proof that the borrower has explored all other loss mitigation options, such as loan modification, forbearance, or a short sale.

- Compliance with Regulations: Lenders must comply with federal and state regulations regarding foreclosure alternatives.

Alternatives to Deed in Lieu

It’s important for borrowers to understand that a deed in lieu is not the only option available when facing mortgage default.

Short Sale

A short sale is another foreclosure alternative where the borrower sells the property for less than the outstanding mortgage balance. The lender must approve the sale price, and in most cases, they agree to accept the proceeds as full satisfaction of the debt, waiving the deficiency. The key difference from a deed in lieu is that a short sale involves a third-party buyer, whereas a deed in lieu transfers ownership directly to the lender. Short sales can sometimes take longer to complete due to buyer negotiations and lender approval processes.

Loan Modification

A loan modification involves changing the terms of the original mortgage loan to make it more affordable for the borrower. This can include lowering the interest rate, extending the loan term, or reducing the principal balance (though this is less common). The goal of a loan modification is to help the borrower keep their home.

Forbearance Agreement

A forbearance agreement is a temporary arrangement where the lender agrees to reduce or suspend mortgage payments for a specified period. This is typically used when a borrower is experiencing a temporary financial setback, such as a short-term job loss or medical emergency. After the forbearance period ends, the borrower will need to resume their regular payments, and often, a repayment plan is established for the missed payments.

Legal and Financial Implications

Understanding the legal and financial ramifications of a deed in lieu is critical.

Credit Score Impact

While generally less damaging than a foreclosure, a deed in lieu will still negatively impact a borrower’s credit score. It will be reported to credit bureaus as a voluntary repossession or a settled loan. The specific impact can vary depending on the credit scoring model and the borrower’s overall credit profile. However, it is often seen as a more responsible action by lenders than simply abandoning the property.

Tax Consequences

The “forgiven” debt (the difference between the outstanding loan balance and the property’s fair market value) in a deed in lieu transaction may be considered taxable income by the IRS. However, there have been legislative provisions, such as the Mortgage Forgiveness Debt Relief Act, that have at times provided relief from this tax liability. It is crucial to consult with a tax professional to understand the specific tax implications in your situation.

Future Borrowing Capacity

A deed in lieu will make it more challenging to obtain new credit, including mortgages, for a period. Lenders will see it as a sign of past financial distress. However, the recovery period might be shorter and less arduous than after a foreclosure.

Conclusion

A deed in lieu of foreclosure represents a pragmatic and often mutually beneficial resolution when a borrower finds themselves unable to meet their mortgage obligations and foreclosure appears imminent. It allows for a more controlled exit from a property, offering significant advantages in terms of credit preservation and reduced legal stress compared to a full foreclosure. For lenders, it provides a more efficient way to regain possession of an asset and mitigate losses. However, it is not a decision to be taken lightly, and borrowers should thoroughly explore all available loss mitigation options and seek professional legal and financial advice before committing to this course of action. Understanding the nuances of this legal instrument is paramount for navigating the complexities of distressed real estate situations.