In the dynamic world of financial management, understanding the different types of investment advisors is crucial for anyone seeking professional guidance. Among the various structures available, Registered Investment Advisors (RIAs) represent a significant and often preferred choice for individuals and institutions looking for fiduciary-level service. This article delves into the essence of what an RIA is, its regulatory framework, its fiduciary duty, and the advantages it offers investors.

Understanding the RIA Framework

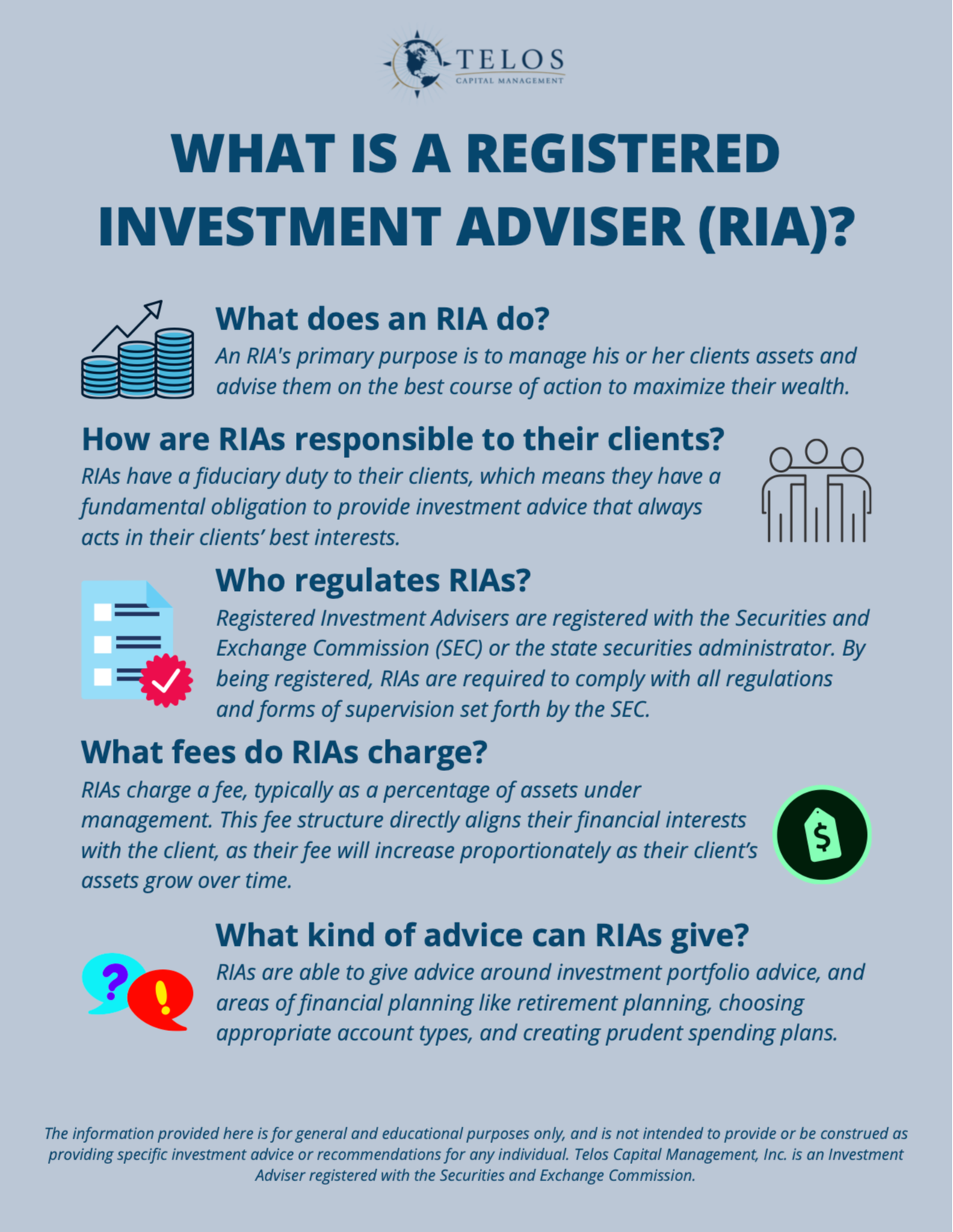

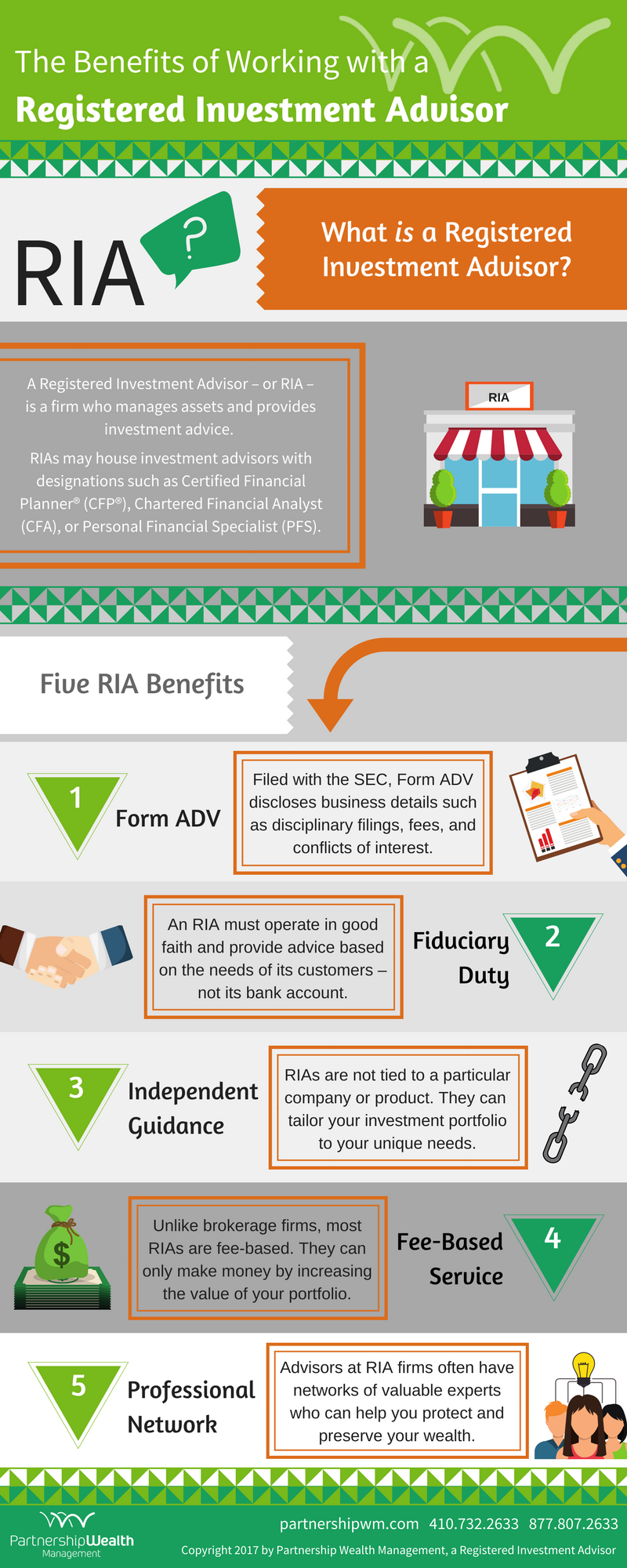

A Registered Investment Advisor (RIA) is an individual or firm that provides investment advice for compensation. The “registered” aspect is key, signifying that they are registered with either the Securities and Exchange Commission (SEC) or state securities authorities. This registration is not a mere formality; it subjects RIAs to a stringent regulatory regime designed to protect investors.

Who is an RIA?

RIAs can be individuals, such as independent financial planners or investment managers, or they can be larger firms. These entities are broadly categorized based on their registration level. Those managing portfolios exceeding $110 million in assets under management (AUM) typically register with the SEC. Smaller advisors, or those whose AUM falls below this threshold, generally register with the securities authorities of the state(s) in which they operate. This tiered registration system ensures that all advisors providing investment advice are subject to oversight, regardless of their size.

The services offered by RIAs are diverse and can include:

- Financial Planning: Developing comprehensive financial strategies encompassing retirement planning, education savings, estate planning, and tax optimization.

- Investment Management: Actively managing client investment portfolios, making buy and sell decisions, and rebalancing assets to align with client goals and risk tolerance.

- Wealth Management: A holistic approach that integrates financial planning, investment management, and other financial services, often catering to high-net-worth individuals.

- Consulting Services: Providing expert advice on specific financial matters without necessarily managing assets directly.

Regulatory Oversight and Compliance

The registration process for an RIA involves meeting specific educational, experience, and ethical standards. Once registered, RIAs are subject to ongoing compliance requirements, including regular examinations by regulatory bodies like the SEC or state securities regulators. These examinations aim to ensure that the RIA is adhering to federal and state securities laws, maintaining accurate records, and fulfilling their obligations to clients.

Key regulations that govern RIAs include:

- The Investment Advisers Act of 1940: This landmark federal legislation established the framework for regulating investment advisors in the United States. It defines what constitutes an investment advisor and outlines their responsibilities.

- State Securities Laws: Each state has its own set of securities laws that RIAs must comply with, particularly concerning registration, record-keeping, and advertising.

- Form ADV: This is the uniform form that RIAs use to register with the SEC or state securities authorities. It provides detailed information about the RIA, its business practices, disciplinary history, and advisory personnel. It is publicly available, allowing investors to research advisors before engaging their services.

The rigorous oversight by regulatory bodies underscores the commitment to investor protection inherent in the RIA model.

The Fiduciary Duty: The Cornerstone of RIA Service

Perhaps the most distinguishing characteristic of an RIA is their fiduciary duty. This legal and ethical obligation requires RIAs to act in the absolute best interests of their clients at all times. Unlike brokers or dealers who operate under a “suitability standard” (meaning their recommendations must be suitable for the client, but not necessarily the absolute best option), RIAs must prioritize their clients’ interests above their own.

What Does Fiduciary Duty Entail?

The fiduciary duty encompasses several critical responsibilities:

- Loyalty: RIAs must place their client’s interests ahead of their own or the firm’s interests. This means avoiding conflicts of interest or, when unavoidable, fully disclosing them and obtaining client consent.

- Care: RIAs must provide advice that is well-researched, prudent, and informed. This involves understanding the client’s financial situation, goals, and risk tolerance, and then recommending investments and strategies that are appropriate for those circumstances.

- Good Faith: RIAs must act with honesty and integrity in all dealings with their clients.

- Disclosure: RIAs have a duty to disclose all material facts, including any conflicts of interest, fees, and the scope of services. Transparency is paramount.

Conflicts of Interest and How RIAs Address Them

Conflicts of interest can arise in various ways within the financial services industry. For example, a broker might recommend a product that earns them a higher commission, even if another product might be slightly more advantageous for the client. RIAs, bound by their fiduciary duty, are obligated to navigate these potential conflicts with utmost transparency.

Common conflicts of interest that RIAs must manage include:

- Proprietary Products: If an RIA’s firm offers its own investment products, they must ensure that recommending these products is genuinely in the client’s best interest and not simply a result of internal incentives.

- Commissions vs. Fees: RIAs are often compensated through fees based on a percentage of AUM, hourly rates, or flat fees. This fee-based compensation structure generally aligns better with client interests than commission-based models, as it reduces the incentive to churn accounts or sell products solely for commission. However, even fee-based advisors must be transparent about their compensation structure.

- Third-Party Payments: If an RIA receives payments from third parties for recommending specific products or services, this must be fully disclosed, and the recommendation must still prioritize the client’s best interests.

The fiduciary standard provides a significant level of assurance to investors that their advisor is committed to their financial well-being.

Advantages of Working with an RIA

The structure and regulatory framework of RIAs translate into several tangible benefits for investors seeking professional financial advice.

Investor Protection and Transparency

The rigorous registration process, ongoing compliance, and the inherent fiduciary duty of RIAs create a robust system of investor protection. Investors can feel more confident knowing that their advisor is legally bound to act in their best interests and is subject to oversight from regulatory bodies. The availability of Form ADV allows for due diligence, providing insights into an advisor’s background, services, and any disciplinary history.

Fee Structures and Alignment of Interests

RIAs often operate on a fee-based model, such as a percentage of assets under management (AUM). This fee structure creates a direct alignment of interests between the advisor and the client. As the client’s assets grow, the advisor’s fees increase, incentivizing the RIA to perform well and help the client achieve their financial goals. While other fee structures exist, such as hourly rates or flat fees for specific services, they are generally designed to be transparent and directly related to the value provided. This contrasts with commission-based models, where advisors may be incentivized to sell products that generate higher commissions, regardless of whether they are the optimal choice for the client.

Comprehensive and Personalized Advice

Because RIAs are fiduciaries, they are compelled to take a holistic view of their clients’ financial lives. This often leads to more comprehensive and personalized financial planning. They are not just recommending investments; they are helping clients build a roadmap to achieve their life goals, considering all aspects of their financial situation, including income, expenses, debt, insurance needs, tax implications, and estate planning.

Independence and Objectivity

Many RIAs operate as independent entities, free from the pressures of selling proprietary products or meeting specific sales quotas imposed by larger financial institutions. This independence allows them to offer objective advice and recommend a broader range of investment options from various providers, selecting those that are truly best suited to the client’s needs. This unbiased approach is a cornerstone of their value proposition.

Long-Term Relationship Focus

The fiduciary model and fee structures often foster a long-term, collaborative relationship between the RIA and the client. The advisor’s success is tied to the client’s long-term financial success, encouraging a partnership focused on consistent growth and achievement of financial objectives over time. This contrasts with transactional relationships that might be more common in other segments of the financial services industry.

Choosing an RIA: Key Considerations

When considering an RIA, prospective clients should engage in a thorough due diligence process.

Research and Due Diligence

- Check Registration: Verify the RIA’s registration status with the SEC’s Investment Adviser Public Disclosure (IAPD) database or the relevant state securities regulator.

- Review Form ADV: Carefully examine the RIA’s Form ADV Part 2 (the “brochure”), which details their services, fees, investment strategies, conflicts of interest, and disciplinary history.

- Assess Experience and Credentials: Look for advisors with relevant certifications such as Certified Financial Planner (CFP®), Chartered Financial Analyst (CFA®), or others that indicate a commitment to professional standards and ongoing education.

Understanding Fees and Services

- Clarify Compensation: Understand exactly how the RIA is compensated – AUM percentage, hourly, flat fee, etc. – and what services are included.

- Scope of Services: Ensure the RIA’s services align with your needs, whether it’s comprehensive financial planning, investment management, or specific advice.

Fiduciary Commitment

- Directly Ask: Confirm that the advisor operates as a fiduciary and is committed to acting in your best interests. While registration as an RIA implies this, direct confirmation is important.

- Ask About Conflicts: Inquire about any potential conflicts of interest and how they are managed.

In conclusion, Registered Investment Advisors (RIAs) play a vital role in the financial ecosystem by offering a regulated, fiduciary-based approach to investment advice. Their commitment to acting in the client’s best interests, coupled with transparency and comprehensive service, makes them a compelling choice for individuals and institutions seeking to navigate the complexities of wealth management and achieve their financial aspirations. Understanding the RIA framework empowers investors to make informed decisions about their financial future.