Understanding the typical credit score requirements for renting an apartment is crucial for any prospective renter. Landlords and property management companies use credit checks as a primary tool to assess a potential tenant’s financial responsibility. A good credit history generally indicates a person’s reliability in meeting financial obligations, including paying rent on time. While there isn’t a single, universally mandated credit score, a general range has become standard across the industry.

The Crucial Role of Credit Scores in Tenant Screening

Why Landlords Check Credit

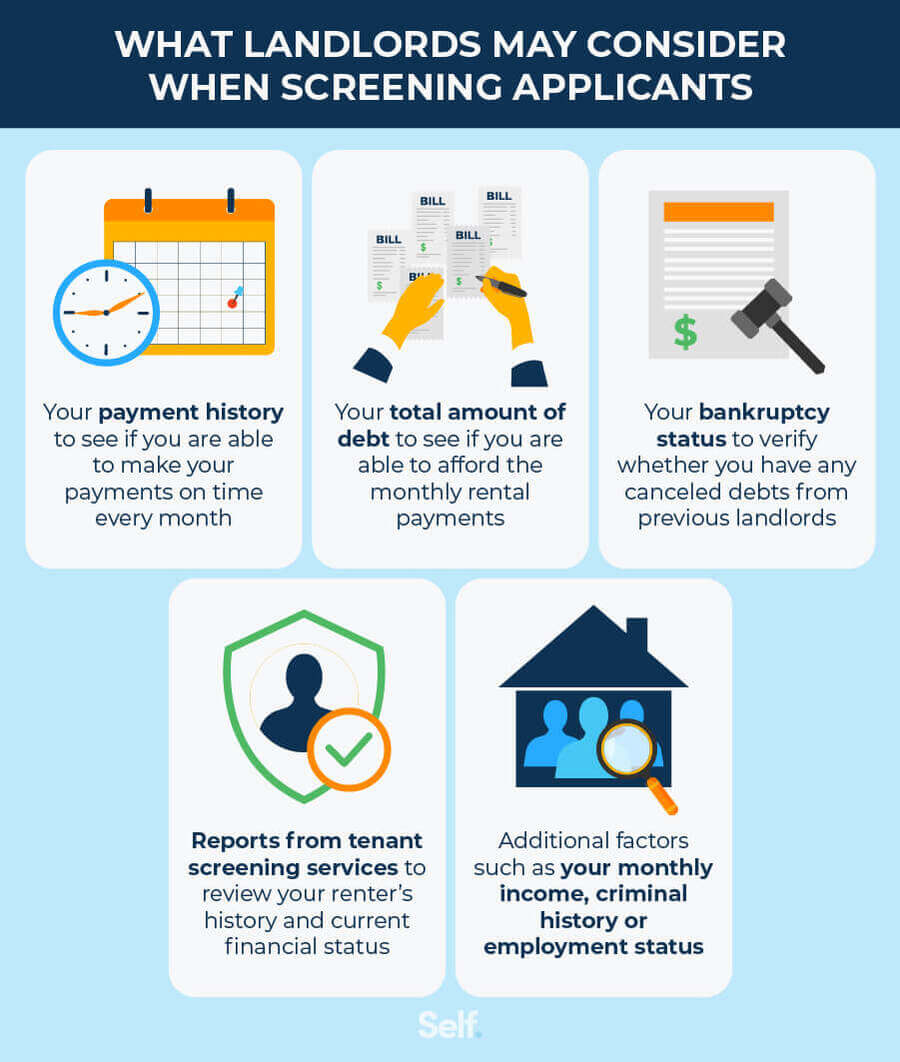

Landlords and property managers view credit scores as a strong predictor of a tenant’s ability to pay rent consistently and care for the property. A higher credit score suggests a history of responsible financial behavior, which translates to a lower perceived risk for the landlord. This risk assessment is vital because eviction proceedings can be costly and time-consuming. By screening for creditworthiness, landlords aim to secure reliable tenants who will fulfill their lease obligations.

What Landlords Look For Beyond the Score

While the numerical score is a significant factor, landlords often consider the entire credit report. This includes:

- Payment History: The most critical element. Late payments, defaults, or collections on past debts are red flags.

- Credit Utilization: How much credit a person is using compared to their available credit. High utilization can indicate financial strain.

- Length of Credit History: A longer history of responsible credit use is generally viewed more favorably.

- Credit Mix: Having a mix of credit types (e.g., credit cards, installment loans) can demonstrate responsible management of different financial instruments.

- Public Records: Bankruptcies, liens, or judgments will significantly impact a rental application.

The Impact of a Low Credit Score

A low credit score can present a substantial barrier to renting. It may lead to:

- Application Denial: The most direct consequence.

- Higher Security Deposits: Landlords might request a larger security deposit to mitigate perceived risk.

- Requirement for a Co-signer: A co-signer with a strong credit history may be required to guarantee the rent payments.

- Limited Rental Options: Properties with stricter screening policies might be inaccessible.

Typical Credit Score Ranges for Renting

The General Benchmark: 600-650

Many landlords consider a credit score of 600 or higher as a baseline for a qualified applicant. However, this is often just the starting point, and many properties aim for tenants with scores closer to 650 and above. A score in this range suggests a reasonably responsible financial history.

Scores Between 700-750: The Ideal Tenant

Tenants with credit scores in the 700 to 750 range are generally considered highly desirable. They demonstrate a consistent track record of financial responsibility, making them low-risk applicants. Landlords are often eager to approve applications from individuals in this bracket.

Scores Above 750: Excellent Creditworthiness

Scores above 750 indicate excellent creditworthiness. Applicants with scores in this category are almost guaranteed to meet most rental requirements and may even be able to negotiate favorable terms.

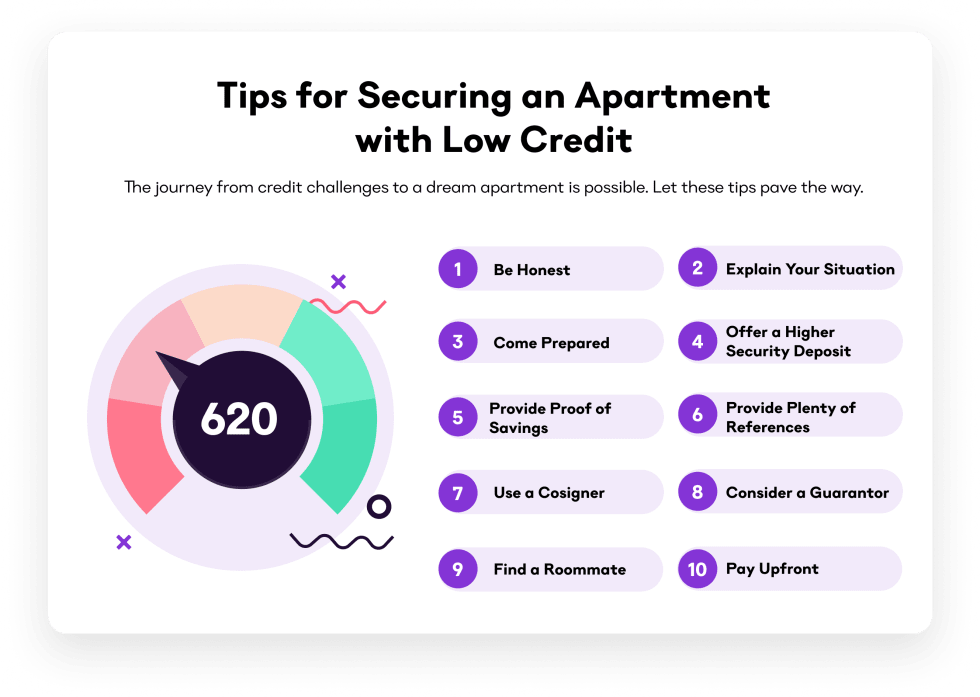

Scores Below 600: Challenges and Alternatives

Applicants with credit scores below 600 often face significant challenges when trying to rent. Many landlords will automatically deny applications with scores in this range. However, this doesn’t mean renting is impossible.

Strategies for Renters with Low Credit Scores

- Find a Co-signer: A person with good credit who is willing to co-sign the lease can significantly improve the chances of approval.

- Offer a Larger Security Deposit: Proposing to pay several months’ rent upfront or a larger security deposit can demonstrate financial commitment and mitigate the landlord’s risk.

- Provide Proof of Income and Savings: Strong evidence of stable employment and substantial savings can help offset concerns about credit history.

- Seek Out Landlords with More Flexible Policies: Some smaller, independent landlords may be more willing to consider the overall picture rather than relying solely on a credit score.

- Consider Renting a Room: Renting a room in a shared house or apartment often involves less stringent screening.

- Improve Your Credit Score: Actively working to improve your credit score over time is the most sustainable long-term solution.

Factors Influencing Rental Credit Score Requirements

Location and Market Demand

Credit score requirements can vary significantly based on the rental market. In highly competitive urban areas with high demand and limited supply, landlords may impose stricter credit score minimums. Conversely, in slower markets, requirements might be more flexible. For instance, a desirable neighborhood in a major city might require a minimum score of 700, while a less competitive area might accept scores as low as 620.

Type of Property and Landlord

The type of rental property and the nature of the landlord also play a role.

- Large Property Management Companies: These organizations typically have standardized, data-driven screening processes, often relying heavily on credit scores. Their minimums tend to be higher and less negotiable.

- Individual Landlords: Smaller landlords, perhaps renting out a single-family home or a duplex, might have more discretion. They may be more inclined to look beyond the score and consider factors like personal references, proof of income, and a well-explained reason for any past credit issues.

Economic Conditions

Broader economic conditions can influence rental market dynamics. During economic downturns, unemployment rates may rise, leading some landlords to become more cautious and potentially raise credit score expectations to ensure rent payment. Conversely, a booming economy with low unemployment might see landlords become more accommodating.

The Application Process: What to Expect

The Rental Application Form

Once you’ve found a potential apartment, you’ll typically be asked to complete a rental application. This form will request personal information, employment history, income details, and references.

The Credit Check Fee

Most landlords charge an application fee, which often covers the cost of running a credit check and background screening. This fee is usually non-refundable, regardless of the outcome of the application. It’s important to be aware of these costs when budgeting for your move.

What Happens After the Credit Check

- Approval: If your credit score and overall application meet the landlord’s criteria, you’ll receive an offer to rent the apartment.

- Conditional Approval: You might be approved, but with certain conditions, such as a higher security deposit or a co-signer.

- Denial: If your application is denied due to your credit score or other screening factors, the landlord is required to provide you with an “adverse action notice.” This notice will explain the reasons for denial and often include information on how to obtain a free copy of your credit report to review for errors.

Improving Your Credit Score for Future Rentals

If your current credit score is not where you’d like it to be for renting, there are proactive steps you can take to improve it.

Key Strategies for Credit Score Improvement

- Pay Bills On Time, Every Time: Payment history is the most significant factor in credit scoring. Set up automatic payments or reminders to ensure you never miss a due date.

- Reduce Credit Utilization: Aim to keep your credit card balances low, ideally below 30% of your credit limit. Paying down existing balances can have a quick positive impact.

- Check Your Credit Report for Errors: Obtain free copies of your credit reports from the three major credit bureaus (Equifax, Experian, and TransUnion) annually. Dispute any inaccuracies you find, as these can unfairly lower your score.

- Avoid Opening Too Many New Credit Accounts at Once: Each new credit application can result in a hard inquiry, which can temporarily lower your score.

- Don’t Close Old, Unused Credit Accounts: The length of your credit history is a factor. Keeping older accounts open (provided they have no annual fees) can help maintain a longer average account age.

- Consider a Secured Credit Card: If you have limited credit history or are rebuilding your credit, a secured credit card (where you provide a cash deposit as collateral) can be a good way to establish a positive payment record.

By understanding the importance of credit scores in the rental process and by taking steps to maintain or improve your financial standing, you can significantly increase your chances of securing the apartment you desire.