Processing costing is an accounting method used by businesses to account for the costs of manufacturing identical or very similar products in a continuous flow. Unlike job costing, where costs are tracked for individual, distinct jobs or products, processing costing groups similar costs over a specific period and allocates them to a large number of identical units. This method is particularly well-suited for industries where mass production of homogeneous goods is the norm, such as food and beverage, chemicals, textiles, and oil refining.

The fundamental principle of processing costing is that it averages costs over all units produced. This means that the cost per unit is not determined until the end of a production period when the total costs incurred are divided by the total number of units completed. This approach simplifies cost accumulation and allocation for high-volume, standardized production environments, providing valuable insights into the efficiency and profitability of manufacturing operations.

Key Principles and Applications of Processing Costing

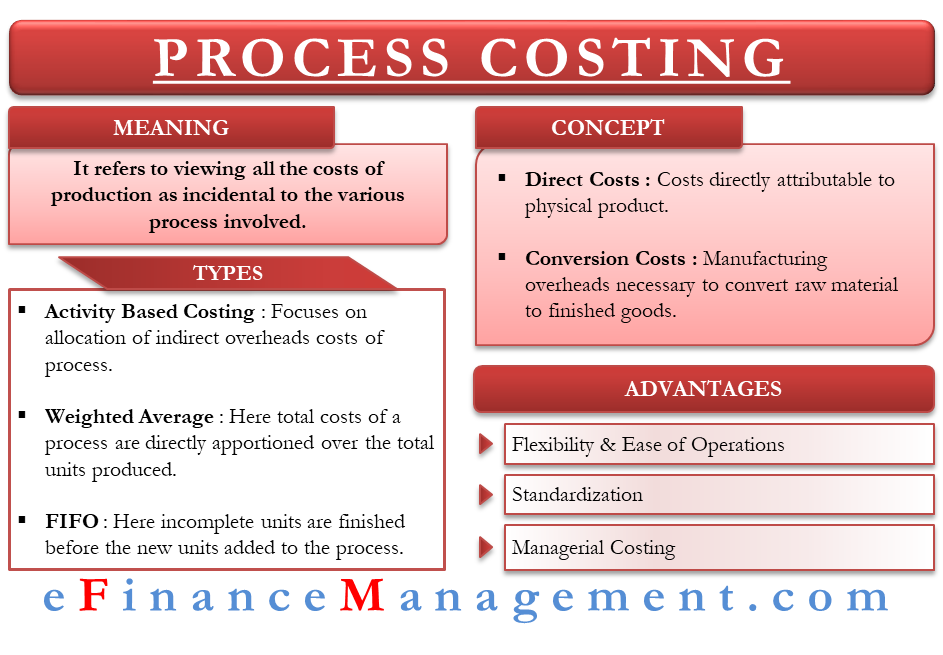

At its core, processing costing operates on the premise of cost averaging. All direct material, direct labor, and manufacturing overhead costs incurred during a specific period are aggregated. This total cost is then divided by the equivalent units produced during that same period to arrive at a cost per unit. Equivalent units are a crucial concept in processing costing, representing the number of fully completed units that could have been produced from the work performed on partially completed units.

This method is typically applied in departments or production processes that transform raw materials into finished goods through a series of continuous operations. For instance, in a bakery, flour, sugar, and other ingredients are processed through mixing, baking, and packaging stages. Each stage might be considered a cost center, and processing costing would be used to track and allocate costs within each department.

Cost Accumulation and Allocation

The process begins with accumulating all costs incurred within a specific production department or process for a given accounting period. This includes:

- Direct Materials: Costs of raw materials that become an integral part of the finished product. In processing costing, these are often added at the beginning of a process or at various stages.

- Direct Labor: Wages paid to workers directly involved in the production process.

- Manufacturing Overhead: Indirect costs associated with production, such as factory rent, utilities, depreciation of machinery, and indirect labor.

Once total costs are accumulated, they need to be allocated to the units produced. Since units may be at different stages of completion at the end of an accounting period, the concept of equivalent units becomes vital.

Equivalent Units: The Cornerstone of Processing Costing

Equivalent units are a measure used to express the amount of work done on partially completed units in terms of fully completed units. The calculation of equivalent units acknowledges that some units may be partially finished in terms of materials, labor, or overhead.

There are two primary methods for calculating equivalent units:

-

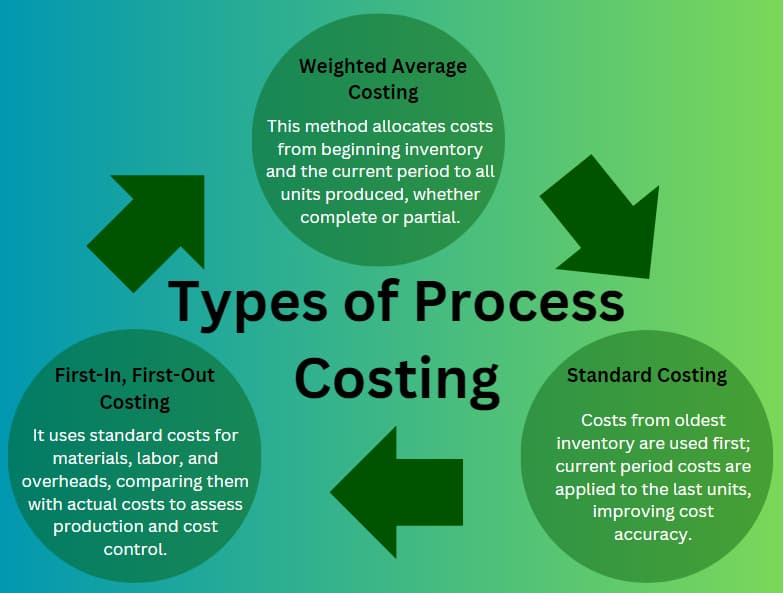

Weighted-Average Method: This method averages costs and equivalent units from both the beginning work-in-process inventory and the units completed during the current period. It treats all units as if they were completed during the current period, simplifying calculations by not distinguishing between beginning and current period work. The formula for equivalent units under the weighted-average method is:

- Equivalent Units = (Units Completed and Transferred Out) + (Equivalent Units in Ending Work-in-Process Inventory)

To calculate the equivalent units in ending work-in-process inventory, you multiply the number of partially completed units by the percentage of completion for each cost element (materials, labor, overhead).

-

First-In, First-Out (FIFO) Method: This method separates the work done on beginning inventory from the work done on units started and completed during the current period. It provides a more accurate measure of current period costs and performance by isolating the costs and effort associated with each batch of production. The FIFO method requires more detailed tracking. The formula for equivalent units under the FIFO method is:

- Equivalent Units = (Units Completed and Transferred Out from Beginning WIP) + (Units Started and Completed during the Period) + (Equivalent Units in Ending Work-in-Process Inventory)

For units transferred out from beginning WIP, you only calculate the equivalent units needed to complete those units. For units started and completed, it’s 100% of the units. For ending WIP, it’s the number of units multiplied by their percentage of completion.

The choice between the weighted-average and FIFO methods depends on the company’s preference and the level of detail required in cost reporting. The weighted-average method is generally simpler to implement, while FIFO offers a more refined view of current period costs.

Departments and Production Stages

Processing costing often involves multiple production departments or stages. Each department can be considered a separate cost center. Costs are accumulated in each department, and then the costs of completed units are transferred from one department to the next.

For example, in a soft drink manufacturing plant:

- Department 1: Mixing: Raw materials (syrup, water) are mixed. Costs of materials, labor, and overhead for mixing are accumulated here.

- Department 2: Bottling: Mixed liquid is bottled. Costs include materials (bottles, caps), labor for filling and capping, and overhead.

- Department 3: Packaging: Bottled drinks are packaged for shipment. Costs include packaging materials, labor, and overhead.

The costs of units completed and transferred out of the mixing department become the direct material costs for the bottling department, and so on. This sequential flow allows for a clear tracking of costs as products move through the manufacturing process.

Advantages and Disadvantages of Processing Costing

Like any accounting method, processing costing has its strengths and weaknesses, making it more suitable for certain industries and less so for others.

Advantages:

- Simplicity for Homogeneous Products: For businesses producing large volumes of identical items, processing costing is far simpler to implement and manage than job costing. It reduces the complexity of tracking individual costs for each unit.

- Cost Control and Efficiency Measurement: By averaging costs over large batches, management can easily identify trends in per-unit costs. Significant increases or decreases in per-unit costs can signal problems with efficiency, material usage, or overhead control, prompting investigations and corrective actions.

- Accurate Valuation of Inventory: Processing costing provides a systematic way to value both work-in-process and finished goods inventory, which is essential for accurate financial reporting.

- Ease of Reporting: The periodic reporting of costs per unit can be streamlined, providing management with regular insights into the financial performance of production processes.

Disadvantages:

- Lack of Specificity for Individual Units: The primary drawback is the inability to determine the exact cost of any single unit. Since costs are averaged, it’s impossible to pinpoint the cost of a specific batch or a particular item. This can be problematic if there are variations in material quality or production efficiency that affect individual units.

- Difficulty with Product Variety: If a company produces a wide variety of products, even within a seemingly homogeneous category, processing costing can become complex and less accurate. Job costing might be more appropriate in such scenarios.

- Potential for Inaccurate Cost Allocation with Fluctuating Production: In periods of significant changes in production levels or inventory, the averaging inherent in processing costing can sometimes distort per-unit costs, making it harder to interpret performance accurately.

- Complexity with Different Cost Addition Points: When materials, labor, and overhead are added at different stages of production, calculating equivalent units can become intricate, especially when using the FIFO method.

Comparison with Job Costing

Understanding processing costing is often best achieved by contrasting it with its alternative, job costing. The choice between these two methods hinges on the nature of the products being manufactured.

Job Costing

Job costing is used when products are unique, custom-made, or produced in distinct batches. Examples include custom furniture, construction projects, consulting services, or specialized equipment manufacturing. In job costing, costs (direct materials, direct labor, and allocated overhead) are tracked and accumulated for each specific job or order. A job cost sheet is maintained for each unique job, providing a detailed breakdown of all costs incurred. The primary advantage of job costing is its ability to determine the precise cost of each individual job, allowing for accurate pricing and profitability analysis for each project.

Key Differences:

| Feature | Processing Costing | Job Costing |

|---|---|---|

| Product Nature | Homogeneous, identical, or very similar products. | Unique, custom-made, or distinct batches of products. |

| Cost Object | Production department or process. | Individual job or order. |

| Cost Accumulation | Total costs for a period are accumulated by department. | Costs are accumulated for each specific job. |

| Cost per Unit | Calculated by averaging total costs over total equivalent units. | Calculated by summing costs for a job and dividing by units in that job. |

| Inventory Valuation | Based on equivalent units and average costs. | Based on actual costs incurred for each job. |

| Reporting | Periodic reports on departmental costs and efficiency. | Detailed cost sheets for each job. |

| Application | Mass production industries (food, chemicals, textiles). | Custom manufacturing, construction, services. |

In essence, processing costing focuses on the efficiency of an ongoing production system, while job costing focuses on the profitability and cost of individual customer orders or unique production runs.

Conclusion

Processing costing is an indispensable tool for businesses engaged in the mass production of standardized goods. Its emphasis on cost averaging and the calculation of equivalent units allows for simplified cost accumulation and allocation, providing management with vital information for controlling production costs and evaluating operational efficiency. While it may not offer the granular detail of job costing for individual units, its strengths in managing high-volume, homogeneous production make it a cornerstone of cost accounting in many essential industries. By understanding the principles of cost accumulation, equivalent units, and the distinction between the weighted-average and FIFO methods, businesses can effectively leverage processing costing to enhance their manufacturing operations and financial reporting.