DuPont analysis, often referred to as the DuPont identity or DuPont model, is a powerful framework for dissecting a company’s financial performance. It breaks down Return on Equity (ROE) into its core components, providing deeper insights than a simple ROE calculation alone. Initially developed by the DuPont Corporation in the 1920s, this method has become a cornerstone of financial analysis for investors, managers, and analysts seeking to understand the drivers of profitability and identify areas for improvement.

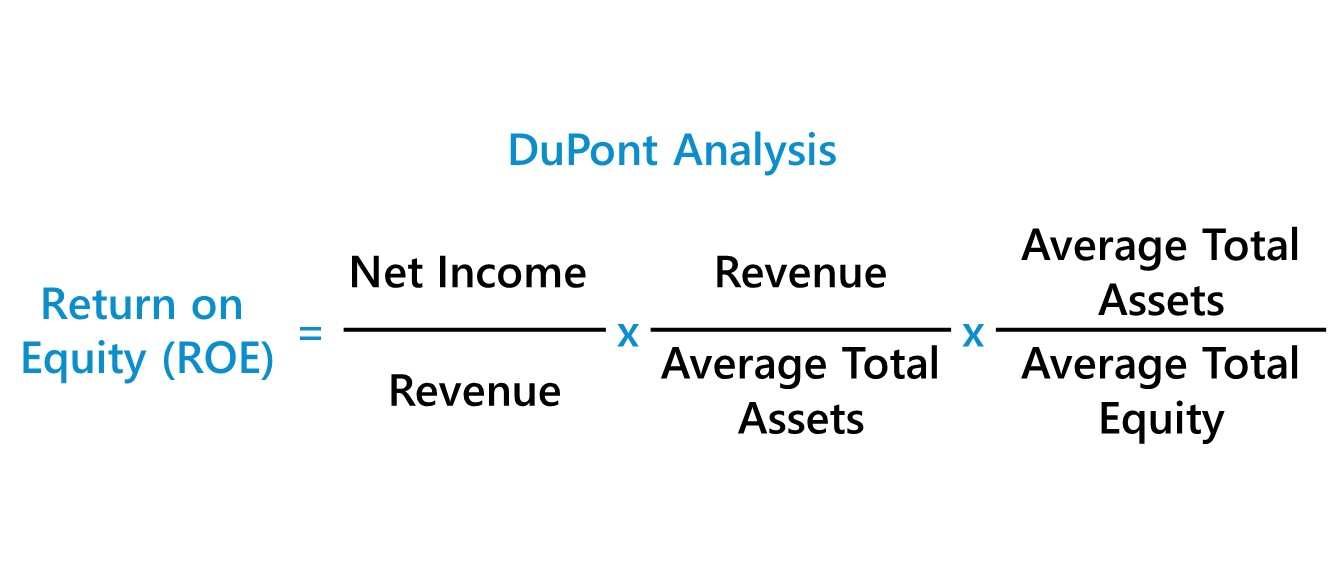

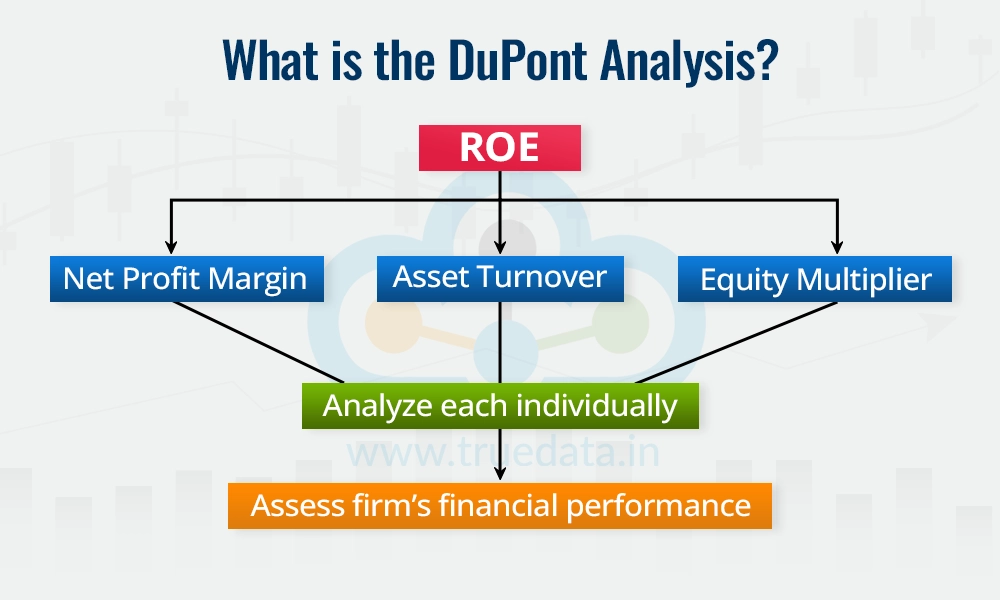

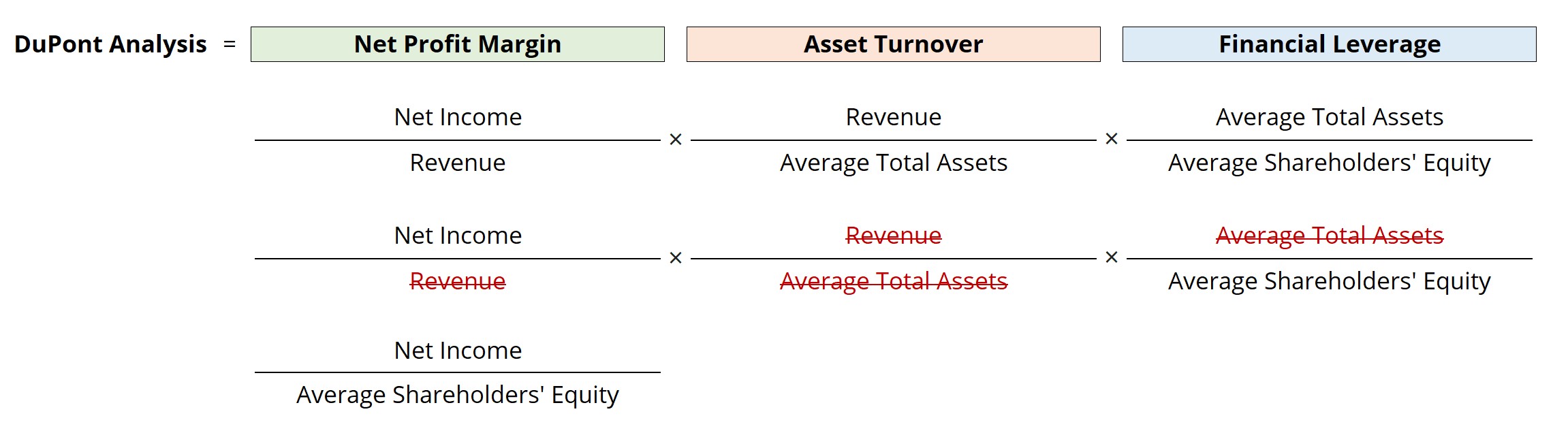

The traditional DuPont analysis expresses ROE as the product of three key financial ratios: Net Profit Margin, Asset Turnover, and Financial Leverage. By examining each of these components individually, stakeholders can pinpoint whether a company’s ROE is being driven by operational efficiency, asset utilization, or debt financing. This nuanced understanding is crucial for making informed strategic decisions and for conducting thorough competitive analysis.

Deconstructing Return on Equity: The Three Pillars of DuPont Analysis

At its heart, DuPont analysis seeks to answer the fundamental question: “What is driving our company’s return to shareholders?” It achieves this by breaking down ROE into a series of interconnected ratios, each revealing a distinct aspect of the business’s financial health and operational effectiveness.

Net Profit Margin: Operational Efficiency and Profitability

The first component of the DuPont analysis is the Net Profit Margin. This ratio measures how much net income is generated for every dollar of sales. It is calculated as:

Net Profit Margin = Net Income / Revenue

A higher net profit margin indicates that a company is more efficient at converting its sales into actual profit. This can be achieved through several avenues:

- Cost Management: Effective control over operating expenses, cost of goods sold, and administrative overhead directly contributes to a higher net profit margin. Companies that can negotiate better terms with suppliers, optimize their production processes, and manage their operational costs diligently will see this ratio improve.

- Pricing Strategies: Strategic pricing, where a company can command higher prices for its products or services without significantly impacting sales volume, will also boost the net profit margin. This is often a reflection of strong brand equity, product differentiation, or a unique value proposition.

- Revenue Enhancement: While seemingly straightforward, efforts to increase revenue through expanded sales channels, new product development, or improved marketing can indirectly impact the net profit margin if the associated costs are managed effectively.

A declining net profit margin, conversely, can signal rising costs, increased competition leading to price pressures, or inefficiencies in operations. It prompts a deeper investigation into the specific cost drivers and revenue streams to identify the root cause of the erosion in profitability.

Asset Turnover: Efficient Use of Resources

The second critical component of the DuPont analysis is Asset Turnover. This ratio measures how effectively a company uses its assets to generate sales. It is calculated as:

Asset Turnover = Revenue / Average Total Assets

A higher asset turnover ratio suggests that a company is generating more sales from its investments in assets. This implies efficient asset utilization and operational agility. Key factors influencing asset turnover include:

- Inventory Management: Companies with lean inventory practices and efficient supply chains can minimize the amount of capital tied up in inventory, thereby increasing their asset turnover. Slow-moving or obsolete inventory can significantly depress this ratio.

- Accounts Receivable Management: Prompt collection of payments from customers reduces the amount of capital tied up in receivables, contributing to a higher asset turnover. Effective credit policies and diligent collection efforts are crucial here.

- Fixed Asset Utilization: Companies that can generate high sales volumes from their existing plant, property, and equipment demonstrate strong asset utilization. This could involve optimizing production schedules, running facilities at higher capacities, or divesting underutilized assets.

Low asset turnover might indicate that a company is holding too much in unproductive assets or that its sales volume is not commensurate with its asset base. This could be a sign of over-investment in assets or a struggling sales department.

Financial Leverage: The Role of Debt

The third component of the DuPont analysis is Financial Leverage, often represented by the Equity Multiplier. This ratio indicates the extent to which a company uses debt to finance its assets. It is calculated as:

Financial Leverage (Equity Multiplier) = Average Total Assets / Average Shareholders’ Equity

This ratio essentially tells us how many dollars of assets are supported by each dollar of shareholder equity. A higher financial leverage ratio signifies that a company is using more debt relative to equity to finance its operations. While debt can amplify returns when a company is performing well, it also magnifies losses and increases financial risk during downturns.

- Amplification of Returns: When a company earns a return on its assets that is higher than the cost of its debt, using debt can significantly boost the Return on Equity. For instance, if a company can borrow at 5% and earn 10% on the borrowed funds, the difference accrues to the equity holders.

- Increased Financial Risk: Conversely, high financial leverage means a company has significant interest obligations. If revenues decline, these fixed interest payments can quickly erode profits and even lead to insolvency. Lenders also view highly leveraged companies as riskier, potentially leading to higher borrowing costs or difficulty in obtaining further financing.

The DuPont analysis highlights the interplay between these three ratios. A company might achieve a high ROE through aggressive debt financing (high leverage), but if its profit margins are thin and asset turnover is low, it might be a precarious situation.

The Expanded DuPont Analysis: A Deeper Dive into Profitability

While the three-component DuPont analysis provides valuable insights, a more detailed version, often referred to as the five-component DuPont analysis, breaks down the Net Profit Margin further. This expanded model offers an even more granular understanding of a company’s operational efficiency.

The Five-Component DuPont Model

The five-component DuPont analysis decomposes ROE as follows:

ROE = (Net Income / Sales) × (Sales / Average Total Assets) × (Average Total Assets / Average Shareholders’ Equity)

The expansion focuses on the Net Profit Margin (Net Income / Sales) by breaking it down into:

- Tax Burden: Net Income / Pretax Income

- Interest Burden: Pretax Income / Operating Income (EBIT)

- Operating Profit Margin (EBIT Margin): Operating Income (EBIT) / Sales

Therefore, the five-component DuPont identity becomes:

ROE = (Net Income / Pretax Income) × (Pretax Income / Operating Income) × (Operating Income / Sales) × (Sales / Average Total Assets) × (Average Total Assets / Average Shareholders’ Equity)

Let’s examine the additional components:

- Tax Burden (Net Income / Pretax Income): This ratio measures the proportion of pretax profit that is kept by the company after taxes. A higher tax burden (closer to 1) means less of the pretax profit is paid in taxes. Factors influencing this include the company’s tax jurisdiction, available tax credits, and tax planning strategies.

- Interest Burden (Pretax Income / Operating Income): This ratio indicates the extent to which operating income is eroded by interest expenses. A higher interest burden (closer to 1) means less of the operating income is consumed by interest payments. This is a direct reflection of the company’s debt levels and the associated interest costs. Companies with lower debt or lower interest rates will have a higher interest burden.

- Operating Profit Margin (EBIT Margin): This is the profit generated from a company’s core business operations before interest and taxes. It is a crucial indicator of the fundamental profitability of the company’s products and services, independent of its financing and tax structure.

By disaggregating the Net Profit Margin, the expanded DuPont analysis allows stakeholders to discern whether improvements or declines in profitability are due to better cost management within operations, more favorable tax treatments, or reduced interest expenses due to lower debt levels.

Applications and Benefits of DuPont Analysis

DuPont analysis is a versatile tool with numerous applications in financial management and investment analysis.

For Management: Strategic Decision-Making and Performance Measurement

- Identifying Strengths and Weaknesses: Management can use DuPont analysis to understand which specific areas of the business are contributing most to ROE and which require attention. If asset turnover is low, management might focus on improving inventory management or divesting underperforming assets. If net profit margin is weak, they might explore cost reduction initiatives or pricing strategies.

- Setting Performance Benchmarks: Companies can use historical DuPont ratios as benchmarks for future performance or compare their ratios against industry peers. This helps in setting realistic targets and identifying areas where the company lags behind competitors.

- Evaluating Strategic Initiatives: Before embarking on new strategies, management can use DuPont analysis to model the potential impact on ROE. For instance, a strategy to increase debt financing would be analyzed for its potential to boost ROE through leverage, balanced against the increased financial risk.

For Investors: Deeper Valuation and Risk Assessment

- Understanding Profitability Drivers: Investors can use DuPont analysis to move beyond superficial ROE figures and understand the quality of a company’s earnings. A high ROE driven by sustainable operational efficiency and asset utilization is generally viewed more favorably than one driven by excessive leverage.

- Comparing Companies: When comparing companies within the same industry, DuPont analysis can reveal fundamental differences in their business models and financial strategies. A company with a lower profit margin but higher asset turnover might be a high-volume, low-margin business, while another might be a low-volume, high-margin business.

- Assessing Financial Risk: The leverage component of DuPont analysis directly highlights a company’s reliance on debt. Investors can use this to assess the financial risk associated with an investment.

Limitations of DuPont Analysis

While powerful, DuPont analysis is not without its limitations:

- Historical Data: The analysis relies on historical financial statements. While useful for understanding past performance, it does not guarantee future results.

- Accounting Methods: The choice of accounting methods (e.g., inventory valuation, depreciation) can influence the ratios, making comparisons between companies that use different methods more challenging.

- Industry Specifics: What constitutes a “good” ratio varies significantly by industry. A high asset turnover might be typical in retail but very low in capital-intensive industries like utilities.

- Focus on Financial Ratios: DuPont analysis primarily focuses on financial ratios. It does not directly incorporate qualitative factors such as management quality, brand reputation, or competitive landscape, which are also crucial for long-term success.

Conclusion

DuPont analysis is an indispensable tool for anyone seeking to gain a comprehensive understanding of a company’s financial performance. By dissecting Return on Equity into its constituent parts – Net Profit Margin, Asset Turnover, and Financial Leverage – it offers a level of insight far beyond simple ratio calculations. The expanded five-component model further refines this analysis, providing a granular view of operational profitability, tax efficiency, and the impact of financing decisions. For both corporate management aiming to drive strategic decisions and investors seeking to make informed choices, DuPont analysis provides a structured and insightful framework for evaluating and understanding the complex drivers of shareholder value. Mastering this analytical approach is a key step in navigating the intricacies of financial statement analysis and achieving a deeper appreciation for corporate financial health.