The world of financial derivatives can often seem complex, a labyrinth of jargon and intricate mechanics. Among the most fundamental and widely discussed are options and futures contracts. While both are derivative instruments, meaning their value is derived from an underlying asset, they possess distinct characteristics, risk profiles, and strategic applications. Understanding these differences is crucial for anyone seeking to engage with financial markets, whether for hedging, speculation, or investment. This exploration delves into the core distinctions between options and futures, illuminating their unique features and how they are employed within the financial landscape.

The Fundamental Nature of Futures Contracts

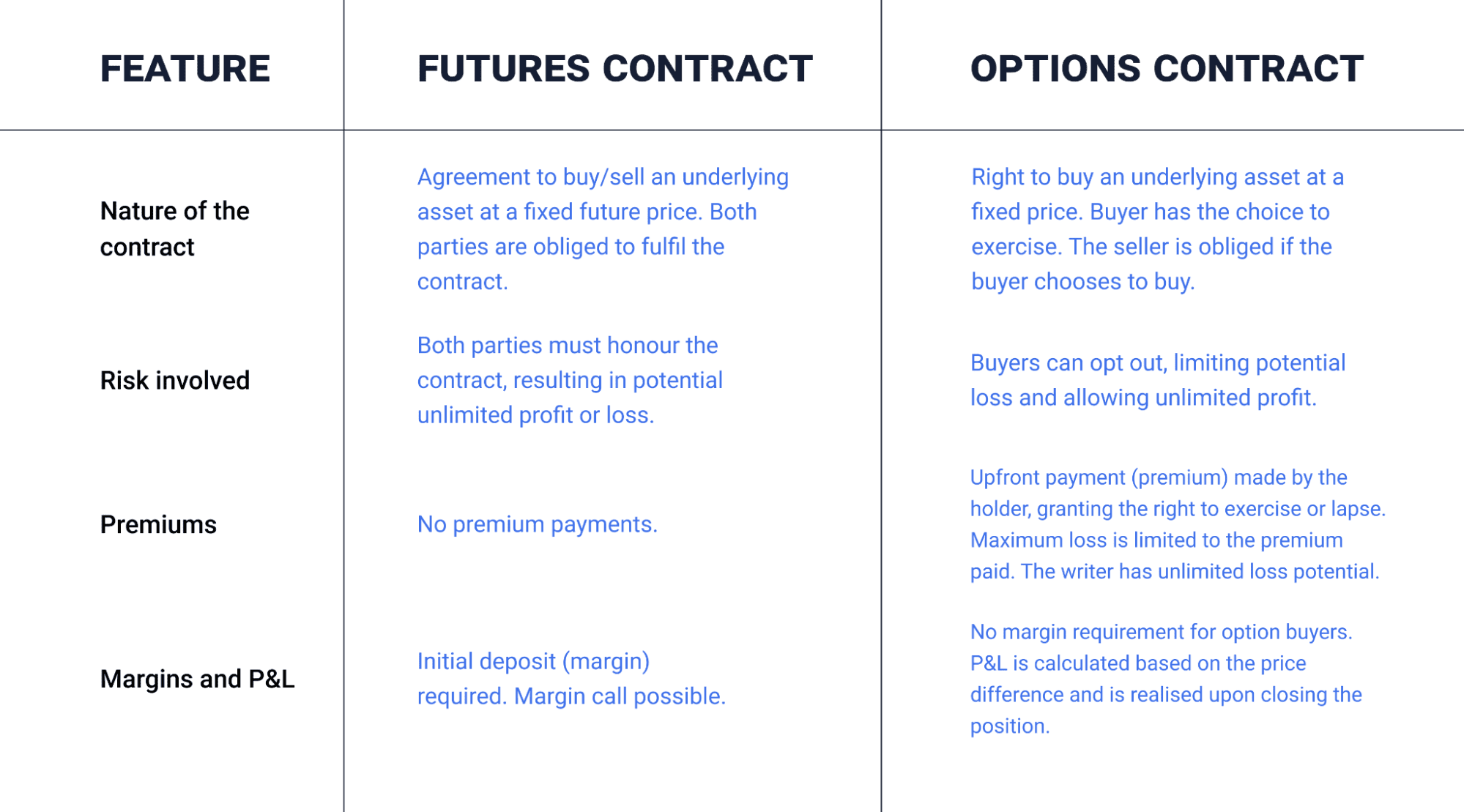

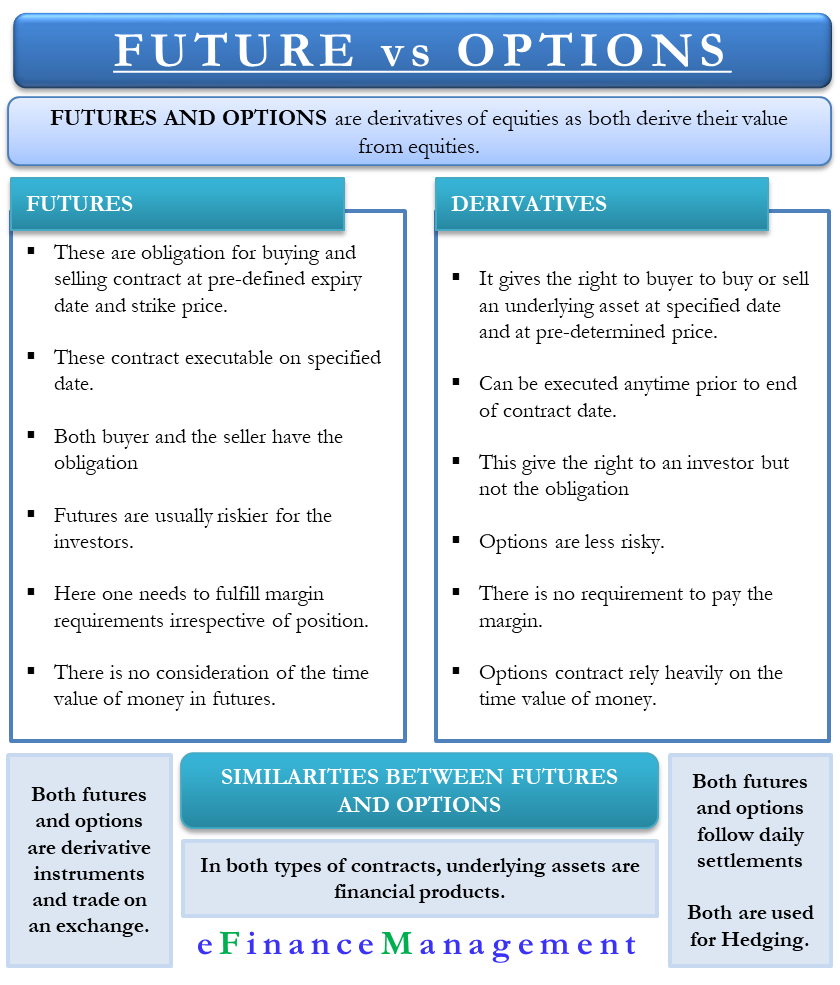

Futures contracts are standardized legal agreements to buy or sell a particular commodity or financial instrument at a predetermined price at a specified time in the future. These contracts are traded on organized exchanges, ensuring transparency and standardization. The underlying assets can range from agricultural products like corn and wheat to financial instruments such as stock indexes, currencies, and interest rates.

Obligation and Execution

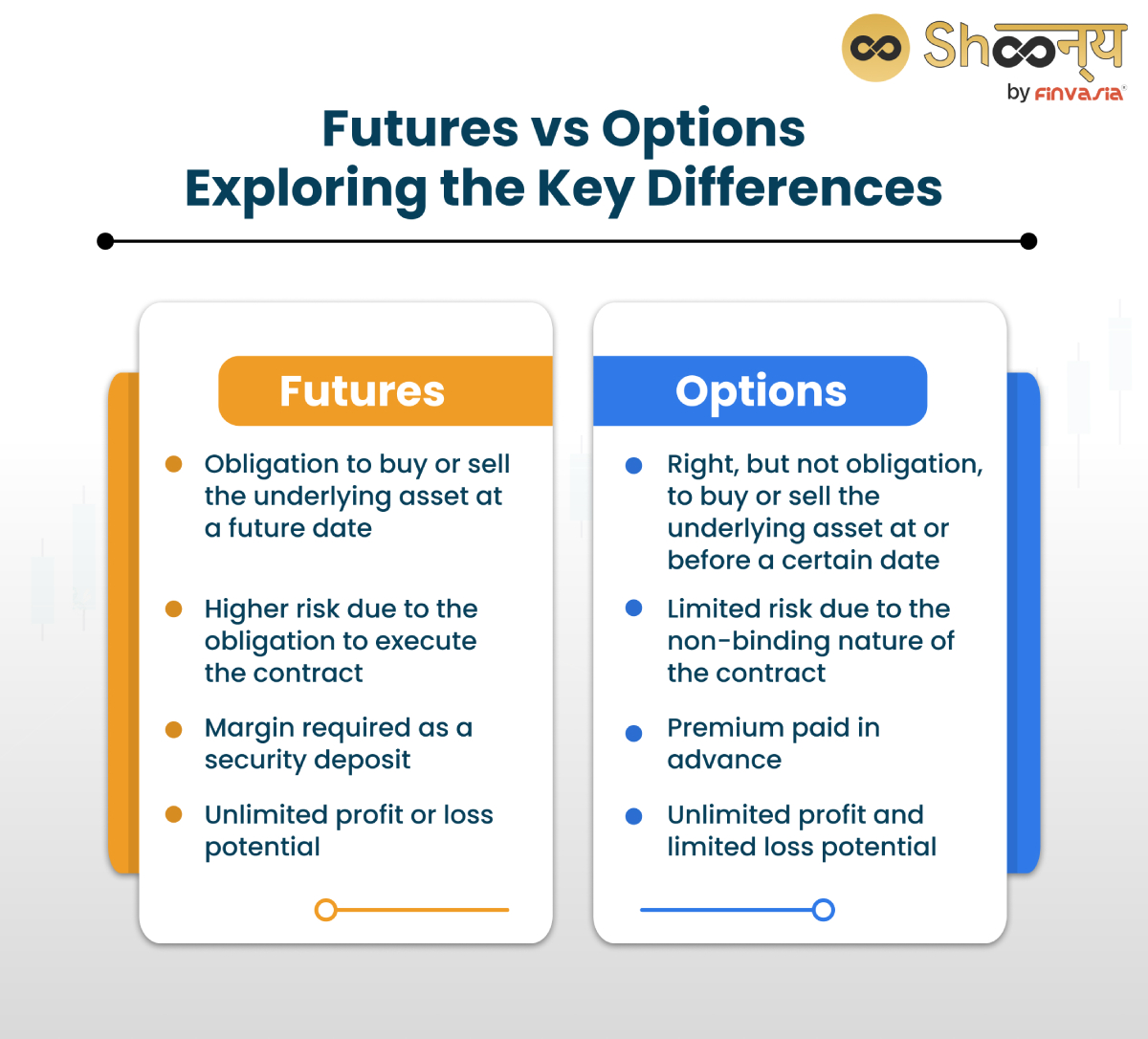

The defining characteristic of a futures contract is the obligation it imposes on both parties. The buyer, often referred to as the “long” position holder, is obligated to buy the underlying asset at the agreed-upon price on the expiration date. Conversely, the seller, or “short” position holder, is obligated to sell the underlying asset at that price. There is no choice in the matter; the contract must be executed.

Margin Requirements and Leverage

Futures trading involves margin requirements. A small percentage of the total contract value is deposited as collateral. This inherent leverage amplifies both potential gains and losses. For instance, if a trader puts up 10% margin for a contract, a 1% move in the underlying asset’s price can result in a 10% gain or loss on their initial capital. This high degree of leverage makes futures contracts attractive for speculators seeking significant returns but also exposes them to substantial risk.

Price Determination and Standardization

Futures prices are determined by supply and demand dynamics on the exchange, reflecting market expectations of future prices for the underlying asset. The standardization of contract size, quality, and delivery terms ensures that all contracts for a given underlying asset are fungible and can be traded interchangeably. This liquidity is a cornerstone of efficient futures markets.

Settlement

Futures contracts can be settled in two ways: physical delivery of the underlying asset (common for commodities) or cash settlement (common for financial futures). Cash settlement involves the difference in price being paid from the losing party to the winning party upon expiration.

The Distinctive World of Options Contracts

Options contracts, while also derived from an underlying asset, offer a different kind of flexibility and risk. An option contract grants the buyer the right, but not the obligation, to buy or sell the underlying asset at a specified price (the strike price) on or before a certain date (the expiration date).

Rights vs. Obligations

This fundamental difference – the right versus the obligation – is the most significant differentiator between options and futures. The buyer of an option pays a premium for this right. If the market moves unfavorably, the buyer can choose not to exercise the option, thereby limiting their loss to the premium paid. The seller of the option, conversely, receives the premium but is obligated to fulfill the contract if the buyer chooses to exercise it.

Types of Options

There are two primary types of options:

Call Options

A call option gives the buyer the right to buy the underlying asset at the strike price. Buyers of call options are generally bullish, expecting the price of the underlying asset to rise. Sellers of call options are typically bearish or neutral, expecting the price to stay below the strike price or fall.

Put Options

A put option gives the buyer the right to sell the underlying asset at the strike price. Buyers of put options are generally bearish, expecting the price of the underlying asset to fall. Sellers of put options are typically bullish or neutral, expecting the price to stay above the strike price or rise.

The Role of the Premium

The premium paid by the buyer to the seller for the option contract is a critical component. This premium is influenced by several factors, including the current price of the underlying asset, the strike price, the time to expiration, implied volatility of the underlying asset, and interest rates. For the seller, the premium represents their potential profit, while for the buyer, it represents the maximum potential loss.

Limited Risk for Buyers, Unlimited Risk for Sellers (Potentially)

For option buyers, the risk is limited to the premium paid. If the option expires worthless, the buyer loses only the premium. For option sellers, the risk can be more significant. A seller of a naked call option (without owning the underlying asset) faces potentially unlimited losses if the underlying asset’s price rises dramatically. Conversely, a seller of a naked put option faces losses up to the strike price if the underlying asset’s price falls to zero. Covered options strategies, where the seller has an offsetting position in the underlying asset, can mitigate some of this risk.

Expiration and Exercise

Options have an expiration date. If the option is “in-the-money” (meaning it would be profitable to exercise) at expiration, the buyer can choose to exercise their right. Otherwise, the option expires worthless, and the premium is lost. Some options are American-style, allowing exercise at any time up to expiration, while others are European-style, exercisable only on the expiration date.

Key Distinctions Summarized

The core differences between options and futures can be distilled into several key areas:

Obligation vs. Right

- Futures: Both buyer and seller have an obligation to the contract.

- Options: The buyer has the right, but not the obligation, to buy or sell. The seller has the obligation if the buyer exercises.

Risk Profile

- Futures: Symmetric risk and reward. Potential for unlimited gains and losses for both parties, amplified by leverage.

- Options: Asymmetric risk and reward.

- Buyers: Limited risk (premium paid), potentially unlimited reward.

- Sellers: Limited reward (premium received), potentially unlimited risk (especially with naked calls).

Initial Cost

- Futures: Involves margin requirements, a deposit to cover potential losses, not the full contract value.

- Options: Involves paying a premium upfront for the right. This premium is the cost of acquiring the option.

Flexibility

- Futures: Less flexible due to the obligation.

- Options: More flexible due to the buyer’s choice to exercise or let the option expire. This flexibility allows for a wider range of strategic applications.

Purpose and Strategy

Futures are often used for hedging price risk for producers and consumers of commodities, or for speculative bets on price movements. Options offer a broader spectrum of strategic uses, including:

- Hedging: Protecting existing positions against adverse price movements with a defined maximum loss.

- Speculation: Gaining leveraged exposure to price changes with a predetermined maximum risk.

- Income Generation: Selling options to collect premiums.

- Portfolio Enhancement: Creating complex strategies like collars or straddles for various market outlooks.

Understanding the Implications for Market Participants

The differing structures of options and futures dictate how they are employed by various market participants.

Hedging

For businesses involved in commodities, futures contracts are a primary tool for hedging. A farmer can sell futures to lock in a price for their crop, protecting against a price decline. An airline can buy oil futures to lock in fuel costs, shielding them from price spikes. Options can also be used for hedging, offering a way to limit downside risk while still participating in potential upside. For example, a company might buy put options on a commodity they need to purchase, protecting against price increases while allowing them to benefit if prices fall.

Speculation

Speculators utilize both instruments to bet on price movements. Futures offer a direct, leveraged play on directional price changes. Options, however, allow for more nuanced speculative strategies. A speculator might buy a call option if they believe a stock will rise significantly but want to limit their risk to the option’s premium. Alternatively, they might sell a put option if they believe a stock will not fall below a certain level, aiming to collect the premium. The flexibility of options allows for speculative strategies that profit from volatility, time decay, or a range-bound market, not just outright price direction.

Investment

While both can be part of an investment portfolio, options are often integrated more strategically. Investors might use options to generate income by selling covered calls on stocks they own, or to hedge against market downturns by buying put options. Futures are less commonly used by retail investors for long-term investment but can be employed by institutional investors for specific asset allocation or tactical trading purposes.

Conclusion: Complementary Tools in the Financial Arena

Options and futures are powerful financial instruments, each with its unique set of characteristics, risk profiles, and applications. Futures provide a direct, obligation-bound agreement for buying or selling an asset at a future date, often employed for straightforward hedging and speculation. Options, on the other hand, offer flexibility through the right, but not the obligation, to trade, empowering a wider array of hedging, speculative, and income-generating strategies with defined risk parameters for buyers.

The choice between employing options or futures—or a combination of both—depends heavily on an individual’s or institution’s specific financial goals, risk tolerance, market outlook, and the underlying asset in question. While futures offer a more direct and perhaps simpler approach to price exposure, options provide a sophisticated toolkit for navigating market uncertainties and constructing tailored financial strategies. Both are indispensable components of modern financial markets, facilitating price discovery, risk management, and capital allocation. A thorough understanding of their fundamental differences is not merely academic; it is essential for making informed decisions in the dynamic world of finance.