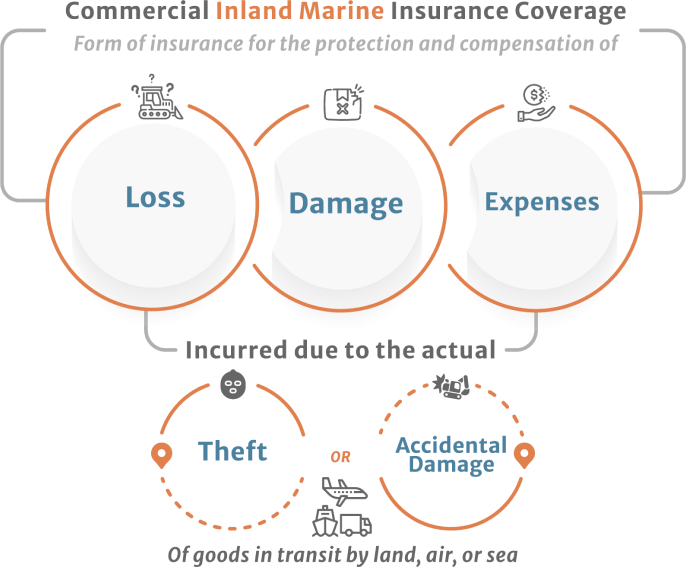

Commercial inland marine coverage is a specialized type of insurance designed to protect valuable property that is in transit over land or is temporarily held at locations away from the primary business premises. Unlike standard commercial property insurance, which typically covers assets fixed at a specific location, inland marine insurance addresses the unique risks associated with movable property. This broad category encompasses a diverse range of items and situations, making it an essential component of risk management for many businesses that deal with valuable goods, equipment, or materials outside their traditional brick-and-mortar facilities.

The “inland” in inland marine refers to property transported over land, as opposed to “ocean marine” insurance, which covers goods transported by sea. This distinction is crucial, as the risks and exposures differ significantly. Inland marine policies are highly customizable, allowing businesses to tailor coverage to their specific needs and the types of property they transport or store off-site. This flexibility makes it a vital tool for companies in sectors such as construction, technology, entertainment, and any industry that involves the movement or temporary storage of valuable assets.

Understanding the Scope of Inland Marine Coverage

Commercial inland marine coverage is not a single, monolithic policy. Instead, it is a collection of specialized coverages designed to address various risks associated with movable property. The common thread is the protection of assets while they are away from the insured’s primary business location, whether that means being transported across states, stored at a job site, or even at a customer’s premises.

Types of Property Covered

The breadth of property that can be insured under an inland marine policy is extensive. It generally falls into several broad categories:

Contractors’ Equipment Floaters

This is one of the most common types of inland marine coverage. It protects tools, machinery, and equipment owned or rented by contractors. This can include everything from small hand tools to large excavators, cranes, and specialized construction equipment. The coverage typically extends to the equipment while it is at a job site, in transit to or from a job site, or even stored temporarily at an off-site location. The policy usually covers perils such as theft, vandalism, fire, natural disasters, and damage occurring during transit. For businesses that move significant amounts of valuable equipment between project locations, this coverage is indispensable. It ensures that the business can replace or repair damaged or stolen equipment, minimizing costly project delays.

Builders’ Risk Insurance

While technically a form of inland marine, builders’ risk insurance is a distinct policy that covers buildings and structures under construction. It protects against damage to the building itself, as well as materials and equipment intended for installation, from various perils like fire, windstorms, vandalism, and theft. The coverage begins when the foundation is laid and ends when the project is completed and occupied or insured by a permanent property policy. This is critical for developers, general contractors, and subcontractors involved in new construction or significant renovations.

Motor Truck Cargo Insurance

This coverage is for businesses that transport goods for others. It protects the cargo being carried by a truck against loss or damage due to a covered peril. Common covered perils include fire, collision, overturning of the truck, theft of the entire shipment, and natural disasters. The policy typically specifies the types of goods being transported and the territorial limits. It’s essential for trucking companies, logistics providers, and any business that relies on third-party carriers to transport their goods and wants to ensure their clients’ property is protected.

Bailee’s Coverage

Bailee’s coverage protects property that is temporarily in the care, custody, or control of a business for servicing, repair, cleaning, or storage. Examples include dry cleaners, repair shops, or art conservators. If the property entrusted to them is damaged or lost due to a covered peril, the bailee’s policy will respond. This coverage is crucial for businesses that handle valuable property belonging to others, as it demonstrates a commitment to protecting customer assets and provides financial recourse if something goes wrong.

Electronic Data Processing (EDP) Coverage

This specialized inland marine policy covers computers, related hardware, software, and sometimes even the data itself. It can cover equipment on or off-premises, in transit, or during installation. This is particularly relevant for businesses that rely heavily on electronic equipment and data, covering risks such as power surges, fire, water damage, and theft. Given the increasing reliance on technology, EDP coverage has become a vital component of risk management for many modern enterprises.

Fine Arts Floaters

For businesses or individuals who own or transport valuable works of art, fine arts floaters provide specialized coverage. This can include paintings, sculptures, antiques, and other collectibles. The policy typically covers damage from fire, theft, accidental breakage, and transit damage. It can be scheduled to cover specific high-value items.

Miscellaneous Articles Floaters

This is a broad category that can cover a wide array of other movable property not specifically covered by other inland marine forms. It can include things like musical instruments, sports equipment, signs, or any other valuable property that is regularly transported or stored off-premises.

Key Benefits and Considerations

Commercial inland marine coverage offers significant advantages for businesses, but it’s essential to understand its nuances and limitations.

Tailored Protection

One of the primary benefits of inland marine insurance is its ability to be tailored to specific business needs. Unlike more standardized policies, inland marine can be customized to cover particular types of property, specific risks, and various geographic territories. This allows businesses to avoid paying for coverage they don’t need while ensuring they are adequately protected against the risks they face.

Protection in Transit

The core function of many inland marine policies is to provide coverage while property is in transit. This is crucial for businesses that ship goods, transport equipment to job sites, or move valuable assets between locations. Standard property insurance often ceases to apply once property leaves the insured premises, creating a significant coverage gap that inland marine fills.

Coverage for Off-Premises Property

Beyond transit, inland marine coverage extends to property that is temporarily stored or used at locations away from the business’s primary facility. This can include property at a customer’s home or business, a rented storage unit, a temporary job site, or an exhibition venue.

Addressing Specific Perils

Inland marine policies often provide broader coverage for specific perils relevant to movable property. For example, they may offer more comprehensive protection against theft, vandalism, or damage occurring during loading and unloading operations, which are common risks for mobile assets.

Risk Management and Business Continuity

By covering valuable assets during transit and at off-site locations, inland marine insurance plays a vital role in business continuity. It ensures that if valuable property is damaged or lost, the business can replace or repair it without suffering catastrophic financial losses, allowing operations to continue with minimal disruption.

Deductibles and Limits

Like all insurance policies, inland marine coverage comes with deductibles and coverage limits. The deductible is the amount the insured business must pay out-of-pocket before the insurance coverage kicks in. Coverage limits are the maximum amounts the insurer will pay for a covered loss. Businesses must carefully consider these aspects to ensure the policy provides adequate protection at an affordable premium.

Valuation Methods

The way property is valued can significantly impact a claim. Inland marine policies may use different valuation methods, such as actual cash value (ACV), which accounts for depreciation, or replacement cost value (RCV), which covers the cost to replace the item with a new one of like kind and quality. Understanding the valuation method used in the policy is crucial for assessing the potential payout in the event of a loss.

When is Commercial Inland Marine Coverage Necessary?

Businesses that engage in activities involving movable property are prime candidates for commercial inland marine coverage.

Construction Companies

As mentioned, contractors’ equipment floaters are essential for construction firms that move expensive tools and machinery between job sites. Builders’ risk insurance is also critical for any project involving new construction or significant renovation.

Technology Companies

Businesses that transport or temporarily store sensitive and valuable electronic equipment, such as computers, servers, or specialized machinery, will benefit from EDP coverage. This is also relevant for companies that lease or rent out such equipment.

Transportation and Logistics Providers

For businesses that transport goods for others, motor truck cargo insurance is a fundamental requirement. This protects the cargo they carry and helps maintain their reputation for reliability.

Entertainment and Event Companies

Companies involved in staging events, providing audiovisual equipment, or transporting valuable performance assets can utilize inland marine policies to protect their gear while it’s on the move or set up at various venues.

Art Dealers and Galleries

Businesses that buy, sell, or exhibit valuable artwork require specialized fine arts floaters to protect these unique and often irreplaceable items during transit and at temporary exhibition spaces.

Any Business with Off-Premises Assets

In essence, any business that has valuable property that is not permanently affixed to its primary business location and is regularly moved or stored elsewhere should investigate inland marine coverage. This could include anything from specialized tools used by service technicians to valuable inventory temporarily stored at a third-party warehouse.

Choosing the Right Inland Marine Policy

Selecting the appropriate inland marine coverage requires a thorough assessment of a business’s operations and risk profile.

Assess Your Assets

Identify all types of valuable property that are regularly moved or stored off-premises. Categorize these assets and determine their approximate value.

Understand Your Risks

Consider the specific perils your property might be exposed to during transit, storage, or use at off-site locations. This includes risks of theft, damage, natural disasters, and accidental loss.

Consult with an Insurance Professional

An experienced insurance broker or agent specializing in commercial insurance can be invaluable. They can help you navigate the complexities of inland marine coverage, assess your needs accurately, and recommend appropriate policy options from reputable insurers.

Review Policy Wording

Carefully read and understand the policy documents, paying close attention to coverage definitions, exclusions, deductibles, limits, and any specific conditions or endorsements.

Consider Endorsements

Depending on your specific needs, you may require endorsements to broaden or narrow coverage. For example, an endorsement might be added to cover property while on exhibition or to extend coverage to property temporarily held by subcontractors.

In conclusion, commercial inland marine coverage is a critical, yet often overlooked, aspect of commercial insurance. It provides essential protection for movable property, addressing the unique risks associated with transit and off-premises storage. By understanding its scope, benefits, and when it is necessary, businesses can make informed decisions to safeguard their valuable assets and ensure operational resilience in an increasingly mobile business environment.