Understanding the Fundamentals of Credit Card Payments in the Digital Age

In today’s interconnected world, the ability to conduct transactions seamlessly and securely is paramount. From purchasing your next drone to acquiring essential accessories, the process of paying for goods and services has evolved dramatically. At the heart of many of these transactions lies the credit card payment system, a complex yet indispensable mechanism that underpins a significant portion of global commerce. Understanding “what is CC payment” involves delving into the technology, security protocols, and the journey of a transaction from initiation to completion.

Credit card payments, often abbreviated as “CC payment,” refer to the process by which a consumer uses a credit card to make a purchase. This involves authorizing a financial institution to extend credit to the consumer to cover the cost of the transaction. The credit card itself acts as a proxy for the consumer’s credit line, allowing for immediate purchase even if the consumer does not have sufficient funds readily available in their bank account. This system, while seemingly straightforward from the user’s perspective, is a sophisticated interplay of various parties, technologies, and security measures designed to facilitate commerce efficiently and safely.

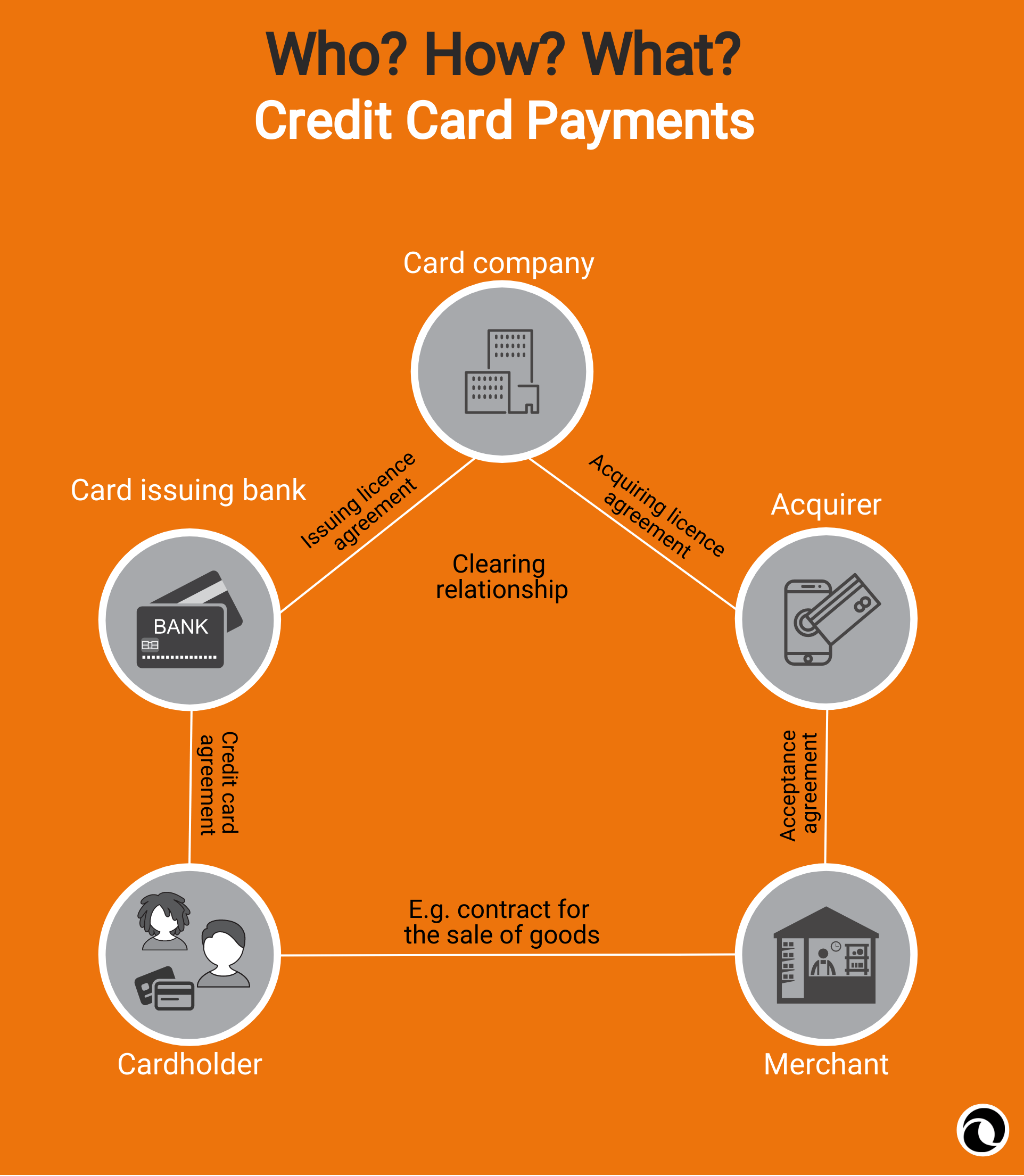

The Key Players in a Credit Card Transaction

Every credit card payment involves a cast of essential players, each with a distinct role:

The Cardholder

This is the individual who owns and uses the credit card to make a purchase. The cardholder is responsible for repaying the credit extended by the issuing bank. Their engagement with the CC payment system begins when they present their card (physically or digitally) at the point of sale.

The Merchant

The merchant is the business or individual selling goods or services. They accept credit cards as a form of payment, typically in exchange for a fee charged by the payment processor. The merchant’s primary goal is to receive payment promptly and securely for the goods or services rendered.

The Acquiring Bank (Merchant’s Bank)

This financial institution provides the merchant with the ability to accept credit card payments. The acquiring bank processes the credit card transactions on behalf of the merchant, deposits the funds into the merchant’s account, and handles the communication with the card networks. They are responsible for approving or declining transactions based on the information received.

The Issuing Bank (Cardholder’s Bank)

This is the financial institution that issued the credit card to the cardholder. The issuing bank extends the credit line to the cardholder and is responsible for billing the cardholder and managing their account. They authorize or decline transactions based on the cardholder’s credit limit, account status, and fraud detection systems.

The Card Network (e.g., Visa, Mastercard, American Express)

Card networks act as intermediaries, connecting the acquiring and issuing banks. They establish the rules and infrastructure for processing credit card transactions, ensuring interoperability between different banks and financial institutions. They are responsible for moving transaction data securely and efficiently between all parties involved.

The Journey of a CC Payment: A Step-by-Step Breakdown

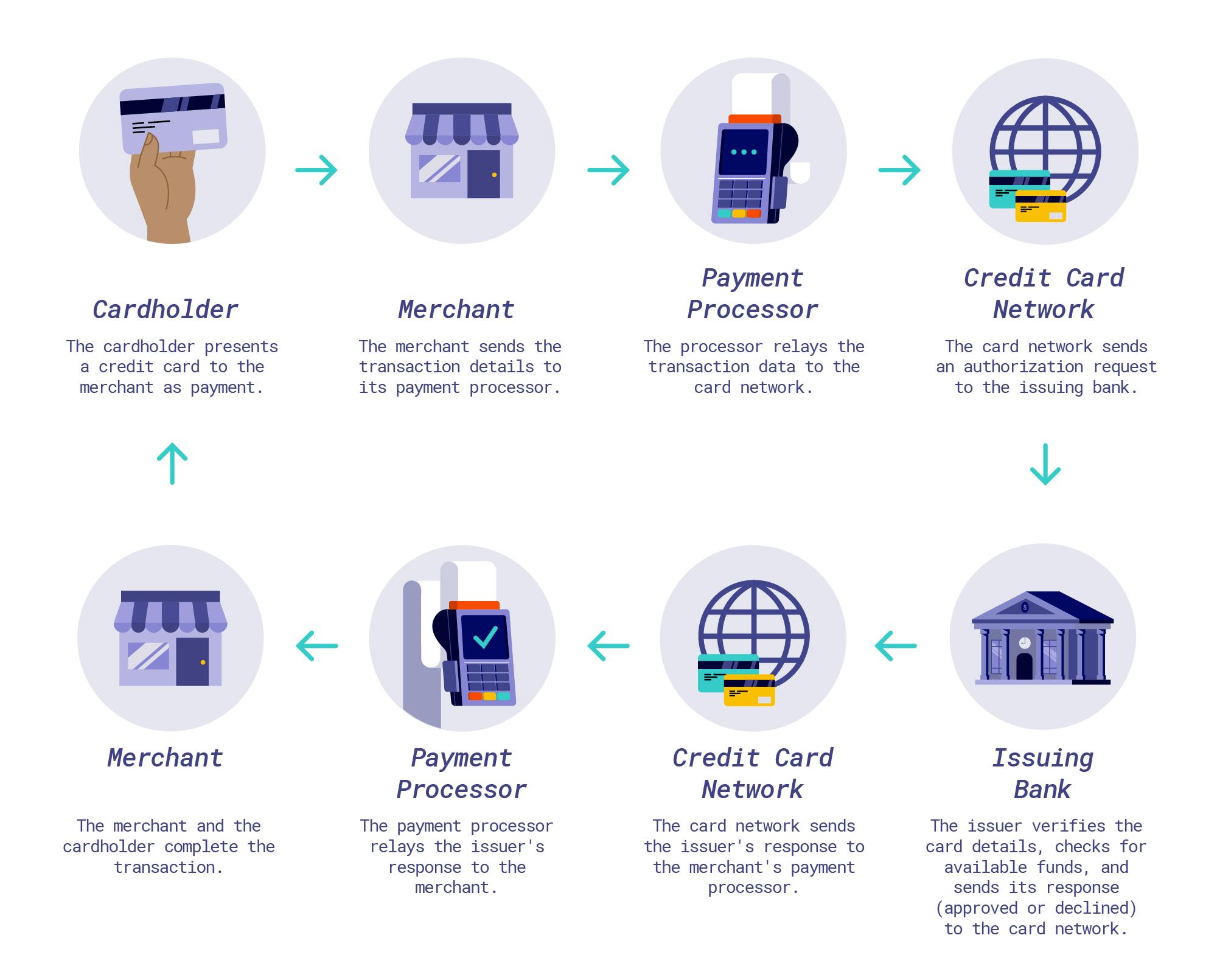

When you swipe your credit card at a drone shop, enter your card details on an e-commerce site, or tap your card for a contactless purchase, a complex sequence of events unfolds in mere seconds.

Authorization: The Initial Approval

- Initiation: The cardholder presents their credit card to the merchant. This can be done physically by swiping or inserting the card into a Point-of-Sale (POS) terminal, or digitally by entering card details on a website or app.

- Data Capture: The POS terminal or online payment gateway captures the cardholder’s information, including the card number, expiration date, CVV code, and billing address. For contactless payments, Near Field Communication (NFC) technology transmits this data wirelessly.

- Information Transmission: The merchant’s acquiring bank receives this transaction data.

- Network Routing: The acquiring bank forwards the transaction details to the appropriate card network (e.g., Visa, Mastercard).

- Issuing Bank Verification: The card network routes the transaction to the cardholder’s issuing bank. The issuing bank performs a series of checks:

- Card Validity: Is the card active and not reported lost or stolen?

- Account Status: Is the account in good standing?

- Credit Limit: Does the cardholder have sufficient credit available to cover the purchase?

- Fraud Detection: Are there any suspicious patterns or indicators of fraud associated with this transaction?

- Authorization Response: Based on these checks, the issuing bank sends an authorization response (approval or decline) back through the card network to the acquiring bank, and finally to the merchant’s POS terminal or gateway.

Clearing and Settlement: The Financial Exchange

If the transaction is approved, the process doesn’t end there. The funds need to be transferred between the banks. This typically occurs in batches at the end of the day or at regular intervals.

- Batch Processing: Merchants group all their approved transactions from a specific period into a batch.

- Clearing: The acquiring bank sends this batch of transactions to the card network for clearing. The card network verifies the details and debits the issuing bank for the total transaction amount.

- Settlement: The card network then instructs the acquiring bank to credit the merchant’s account with the total value of the approved transactions, minus any processing fees. Simultaneously, the issuing bank debits the cardholder’s account for the amount of the purchase, adding it to their credit card statement.

This clearing and settlement process ensures that the merchant receives their funds and the cardholder is correctly billed for their purchase.

Security: The Cornerstone of CC Payment

Given the sensitive nature of financial data, security is a paramount concern in CC payment systems. Numerous measures are in place to protect cardholders and merchants from fraud and data breaches.

Key Security Features and Protocols

EMV Chip Technology

Enhanced security is provided by the EMV chip (Europay, Mastercard, and Visa) embedded in most modern credit cards. Unlike magnetic stripe cards, which store static data, EMV chips generate a unique transaction code for each purchase, making it significantly harder for counterfeit cards to be used successfully.

CVV/CVC Codes

The Card Verification Value (CVV) or Card Verification Code (CVC) is a three or four-digit security code found on the back of most credit cards. It is used as an additional layer of verification during card-not-present transactions (online or by phone) to help confirm that the cardholder is in physical possession of the card.

Tokenization

Tokenization is a security technology that replaces sensitive credit card data with a unique, randomly generated string of characters called a “token.” This token has no exploitable value if intercepted. When a payment is processed, the token is used instead of the actual card number. This is particularly prevalent in mobile payment systems and for storing card details for recurring billing.

Encryption

Data transmitted during a credit card transaction is encrypted, meaning it is converted into a coded format that can only be deciphered with a specific key. This protects the data from being read by unauthorized parties if intercepted during transmission.

PCI DSS Compliance

The Payment Card Industry Data Security Standard (PCI DSS) is a set of security standards designed to ensure that all companies that accept, process, store, or transmit credit card information maintain a secure environment. Merchants handling credit card data must adhere to these strict requirements to protect cardholder information.

Fraud Monitoring Systems

Issuing banks and card networks employ sophisticated fraud detection systems that utilize artificial intelligence and machine learning to analyze transaction patterns in real-time. These systems can flag suspicious activities, such as unusually large purchases, transactions in foreign locations, or multiple attempts in a short period, prompting further verification or blocking the transaction to prevent fraud.

The Evolving Landscape of CC Payments

The world of CC payments is not static; it’s constantly evolving with technological advancements and changing consumer behaviors.

Contactless Payments

The rise of contactless payment methods, enabled by NFC technology, has made transactions faster and more convenient. With a simple tap of a card or smartphone, users can complete purchases, reducing the need for physical card insertion or swiping. This technology is increasingly integrated into mobile wallets like Apple Pay and Google Pay, which often use tokenization for enhanced security.

Mobile Wallets and Digital Payments

Mobile wallets consolidate various payment methods, including credit cards, into a digital format accessible via a smartphone or smartwatch. These platforms offer a secure and streamlined payment experience, often leveraging tokenization and biometric authentication (fingerprint or facial recognition) for added security.

Recurring Billing and Subscriptions

Many services, especially in the digital realm, rely on recurring billing models. CC payments are fundamental to these subscription services, where card details are securely stored and automatically charged at predetermined intervals. This requires robust systems for managing subscription data and ensuring ongoing authorization.

The Future of CC Payments

As we look ahead, we can expect further integration of AI in fraud detection and personalization of payment experiences. Biometric authentication is likely to become more widespread, and the lines between traditional banking and digital payment platforms will continue to blur. For businesses, particularly those in niche markets like drone technology, understanding and optimizing their CC payment processing is crucial for customer satisfaction and operational efficiency. A smooth and secure payment experience can be the deciding factor for a customer looking to purchase a new aerial photography drone or a set of specialized propellers.

In conclusion, “what is CC payment” encompasses a robust system designed to facilitate secure and efficient commerce. From the initial authorization request to the final settlement of funds, each step involves a complex network of participants and sophisticated technologies working in concert. As technology advances, the CC payment landscape will undoubtedly continue to adapt, offering even greater convenience and security for consumers and merchants alike.