The world of financial derivatives, particularly options trading, offers a complex yet powerful set of strategies for investors. Among these, the option strangle stands out as a popular, albeit sophisticated, approach. Understanding an option strangle requires delving into the fundamental concepts of options, their interplay, and the market conditions under which this particular strategy thrives. At its core, an option strangle is a neutral trading strategy that profits from a significant price movement in an underlying asset, regardless of the direction of that movement. It achieves this by simultaneously buying both a call and a put option on the same underlying asset, with the same expiration date, but different strike prices. This divergence in strike prices is the defining characteristic of a strangle, setting it apart from its close cousin, the straddle.

The Anatomy of an Option Strangle

To truly grasp the mechanics of an option strangle, it’s essential to break down its components and the rationale behind their selection. This strategy is not about predicting the precise direction of a stock or asset’s price, but rather about anticipating volatility.

Buying a Call and a Put

The foundation of an option strangle lies in the simultaneous purchase of two distinct option contracts: a call option and a put option.

The Call Option

A call option gives the buyer the right, but not the obligation, to purchase an underlying asset at a specified price (the strike price) on or before a certain date (the expiration date). When an investor buys a call option, they are generally anticipating that the price of the underlying asset will rise significantly above the strike price before the option expires. In the context of a strangle, the call option is typically bought with a strike price above the current market price of the underlying asset. This is known as buying an “out-of-the-money” (OTM) call. The expectation is that the asset’s price will surge past this higher strike price, making the call option valuable.

The Put Option

Conversely, a put option grants the buyer the right, but not the obligation, to sell an underlying asset at a specified strike price on or before its expiration date. Buying a put option is usually a bet on the price of the underlying asset falling. In a strangle, the put option is typically bought with a strike price below the current market price of the underlying asset. This is also an “out-of-the-money” (OTM) put. The investor holding the strangle expects the asset’s price to plummet below this lower strike price, thereby increasing the value of the put option.

Strike Price Divergence: The Defining Feature

The crucial element that distinguishes a strangle from a straddle is the difference in strike prices. In a strangle, the call option’s strike price is set higher than the current market price of the underlying asset, while the put option’s strike price is set lower than the current market price.

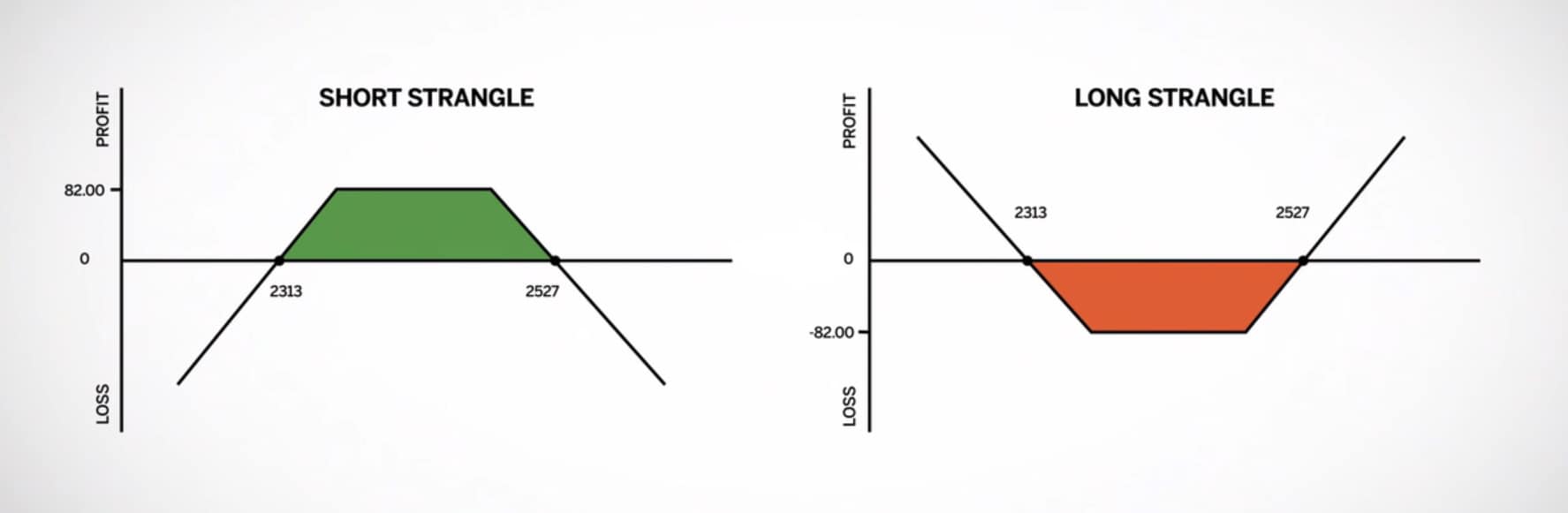

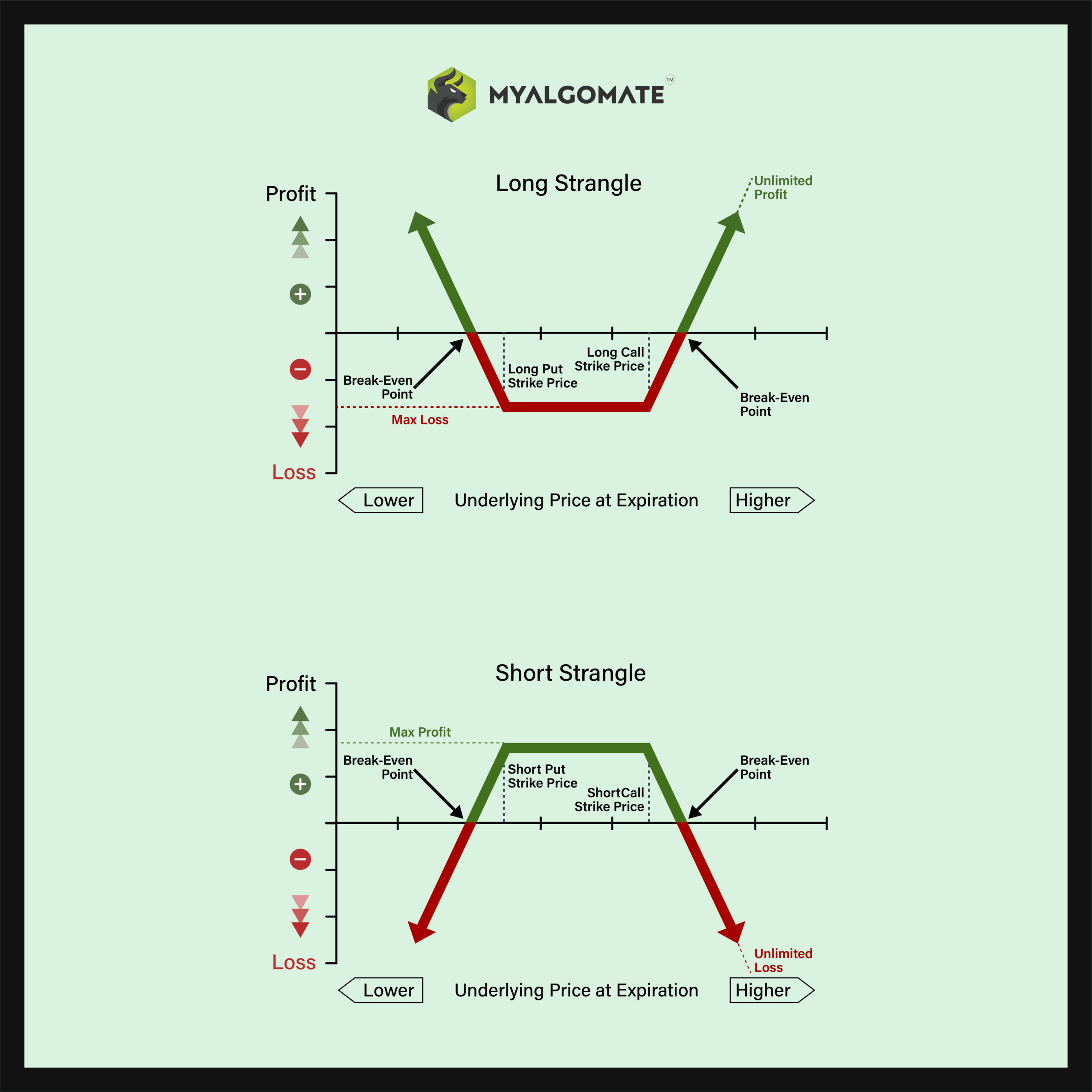

Long Strangle vs. Short Strangle

The discussion thus far has focused on a “long strangle,” where the investor buys both the call and the put options. This is the most common form of the strategy. However, there is also a “short strangle,” where the investor sells both an OTM call and an OTM put. This is a significantly riskier strategy, as it profits from low volatility and has potentially unlimited losses if the price moves significantly in either direction. For the purposes of this article, we will primarily focus on the long strangle, as it is the strategy most commonly referred to when discussing option strangulation in a neutral volatility context.

When to Employ an Option Strangle

The decision to implement an option strangle is driven by a specific set of market expectations. It is a strategy best suited for periods of anticipated high volatility, where a substantial price movement is expected, but the direction is uncertain.

Anticipating High Volatility

The primary catalyst for employing a long strangle is the expectation of a significant price swing in the underlying asset. This anticipation often arises before major events that could impact the asset’s value.

Earnings Announcements

One of the most common scenarios for using a strangle is around earnings reports. Companies often experience substantial price movements following the release of their quarterly or annual earnings. If an investor believes the market is underestimating the potential for a large price move, either up or down, a strangle can be an effective way to capitalize.

Major Economic Data Releases

Significant economic data, such as inflation reports, interest rate decisions by central banks, or employment figures, can trigger considerable market volatility. If an investor anticipates a dramatic reaction to such data but is unsure of the direction, a strangle can be a suitable strategy.

Geopolitical Events and News

Unforeseen geopolitical events or unexpected news can also lead to sharp price fluctuations. In such situations, where the market’s reaction is likely to be pronounced but the direction is unclear, a strangle can be considered.

Product Launches and Regulatory Decisions

For companies, major product launches or significant regulatory decisions can also be catalysts for volatility. If the outcome of these events is uncertain and could lead to a substantial price shift, a strangle might be employed.

The “Neutral” Aspect

While the strangle profits from volatility, it is considered a “neutral” strategy because it does not rely on a directional bias. The investor is not betting on the asset going up or down specifically; they are betting that it will move enough. This means that even if the price moves significantly against the investor’s initial intuition about direction, the strategy can still be profitable if the magnitude of the move is sufficient to overcome the cost of the premiums paid.

Profit and Loss Scenarios

Understanding the potential outcomes of an option strangle is crucial for effective risk management. The profitability of this strategy is directly tied to the magnitude of the price movement of the underlying asset relative to the strike prices and the premiums paid.

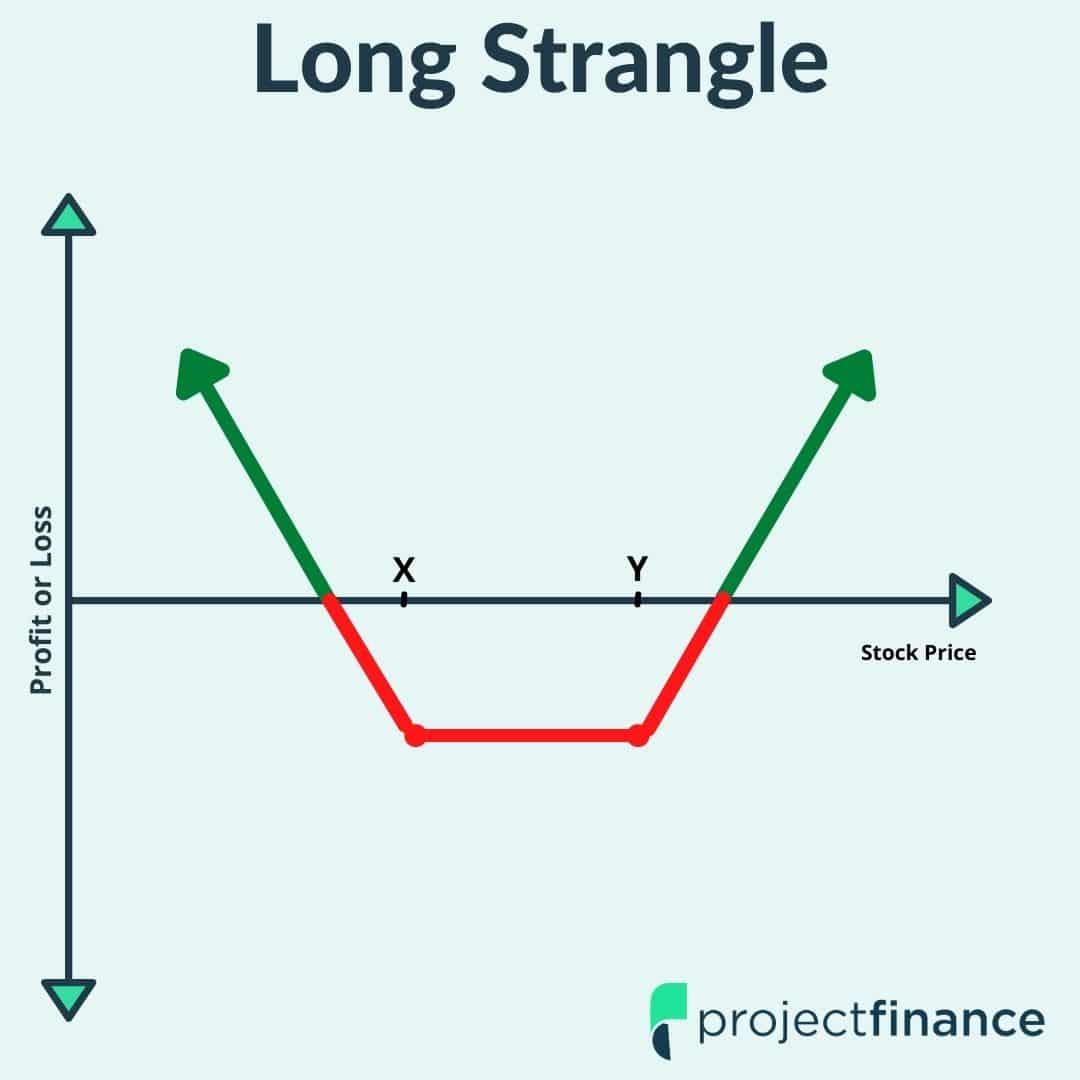

Maximum Profit

The theoretical maximum profit of a long strangle is unlimited. This occurs if the price of the underlying asset moves significantly higher, causing the call option to become highly profitable, or significantly lower, causing the put option to become highly profitable.

Scenario: Price Surges Upwards

If the price of the underlying asset rises dramatically above the strike price of the call option, the call option will gain substantial intrinsic value. While the put option will likely expire worthless (having been bought OTM), the gains from the call can outweigh the cost of both premiums. The higher the price goes, the greater the profit from the call option.

Scenario: Price Plummets Downwards

Conversely, if the price of the underlying asset falls sharply below the strike price of the put option, the put option will accrue significant intrinsic value. The call option will likely expire worthless, but the gains from the put can exceed the total premium paid for both options. The lower the price falls, the greater the profit from the put option.

Maximum Loss

The maximum loss on a long strangle is limited to the total cost of the premiums paid for both the call and the put options. This occurs if the price of the underlying asset at expiration is between the strike prices of the two options.

Breakeven Points

A strangle has two breakeven points:

- Upper Breakeven Point: This is calculated by taking the strike price of the call option and adding the total premium paid for both options. If the underlying asset’s price is at or above this point at expiration, the strategy will generate a profit.

- Lower Breakeven Point: This is calculated by taking the strike price of the put option and subtracting the total premium paid for both options. If the underlying asset’s price is at or below this point at expiration, the strategy will also generate a profit.

Any price movement of the underlying asset that results in its closing price falling between these two breakeven points at expiration will result in a loss for the strangle holder. The closer the price is to the middle of the two strike prices, the larger the loss, with the maximum loss occurring precisely at the midpoint between the two strike prices if both options expire worthless.

Factors Influencing Strangle Profitability

Several key factors can significantly impact the success or failure of an option strangle strategy. These include the volatility of the underlying asset, time decay, and the specific strike prices chosen.

Implied Volatility (IV)

Implied volatility is a crucial factor in option pricing and, by extension, in the profitability of a strangle.

Buying Volatility

A long strangle is a strategy that benefits from an increase in implied volatility. When IV is high, option premiums (the price of buying options) are also high. If an investor expects IV to increase even further after they have purchased the strangle, this can contribute to potential profits, as the value of their options may rise due to the increased volatility expectation, even before a significant price move occurs. Conversely, if IV decreases after buying the strangle, it can erode the value of the options, leading to losses.

The Role of Historical Volatility vs. Implied Volatility

It’s important to distinguish between historical volatility (how much the price has moved in the past) and implied volatility (the market’s expectation of future volatility). A strangle is a play on implied volatility. Investors often use a strangle when they believe implied volatility is too low and that actual price movement will exceed the market’s expectations.

Time Decay (Theta)

Option premiums are eroded by time decay, also known as theta. As an option approaches its expiration date, its time value diminishes, assuming all other factors remain constant. For a long strangle, time decay works against the investor. Both the bought call and the bought put are subject to time decay.

Impact on OTM Options

Since strangulation involves buying out-of-the-money options, these options have a higher proportion of time value compared to at-the-money or in-the-money options. This means they are more susceptible to rapid erosion of value as expiration approaches. If the underlying asset’s price does not move sufficiently to offset the effects of time decay, the strangle can become unprofitable. This underscores the importance of the anticipated price movement being substantial and occurring in a timely manner.

Strike Price Selection

The choice of strike prices for the call and put options is critical in determining the risk and reward profile of a strangle.

Wider Strikes = Higher Cost, Greater Potential Profit

Choosing strike prices that are further away from the current market price of the underlying asset (i.e., wider strikes) will result in lower premiums for each option because they are more out-of-the-money. However, this also means that the underlying asset’s price will need to move further to reach the breakeven points, and the potential profit, while theoretically unlimited, will require a larger price excursion to become significantly profitable. The total cost of the strangle will be lower, but the probability of reaching profitability may also decrease.

Narrower Strikes = Lower Cost, Smaller Potential Profit

Conversely, selecting strike prices that are closer to the current market price (i.e., narrower strikes) will result in higher premiums for each option as they are closer to being at-the-money. The breakeven points will be closer to the current price, making it easier for the underlying asset to move beyond them. This increases the probability of reaching a profitable trade, but the potential profit may be capped by the cost of the higher premiums and the fact that the underlying asset has less room to move before one of the options becomes significantly profitable.

Advantages and Disadvantages of an Option Strangle

Like any trading strategy, the option strangle comes with its own set of benefits and drawbacks. Understanding these can help an investor decide if it aligns with their trading style and risk tolerance.

Advantages

- Profit from Volatility: The primary advantage is the ability to profit from significant price movements, regardless of direction. This is particularly useful when a major event is anticipated but the market’s reaction is uncertain.

- Defined Maximum Loss: In a long strangle, the maximum potential loss is strictly limited to the total premiums paid for the options. This provides a clear risk management boundary.

- Unlimited Profit Potential: Theoretically, the profit potential is unlimited if the underlying asset experiences a substantial price move in either direction.

- Flexibility: Can be applied to various underlying assets like stocks, indices, ETFs, and commodities.

Disadvantages

- Requires Significant Price Movement: The underlying asset must move substantially beyond the breakeven points to generate a profit. A modest move, or no move at all, will result in a loss.

- Time Decay (Theta) is Detrimental: Time decay works against the buyer of a long strangle, eroding the value of the options as expiration approaches.

- Higher Premium Cost: Compared to other strategies, a strangle often requires a higher initial investment due to the purchase of two options, particularly if the strike prices are relatively close to the current market price.

- Sensitivity to Implied Volatility Changes: A decrease in implied volatility after initiating a long strangle can lead to losses, even if the price of the underlying asset moves favorably.

In conclusion, the option strangle is a potent strategy for traders who anticipate significant volatility in an underlying asset but are uncertain about the direction of the price movement. It requires a thorough understanding of options, volatility, and time decay, and is best employed when there is a clear catalyst for a substantial price swing. By carefully selecting strike prices and managing the trade through its lifecycle, investors can leverage this strategy to potentially capitalize on dramatic market shifts.