Understanding Transaction Privilege Tax (TPT) in Business

Transaction Privilege Tax (TPT), often referred to as sales tax in many other states, is a privilege granted by the government to businesses to engage in retail sales, contracting, or other specified business activities within a jurisdiction. It is not a tax on the seller or the buyer directly, but rather a tax on the privilege of conducting business. The business then acts as a collector of this tax from the end consumer and remits it to the state and/or local government. Understanding TPT is crucial for any business operating within a TPT jurisdiction, as it impacts pricing, accounting, and compliance.

Core Concepts of Transaction Privilege Tax

At its heart, TPT is a tax levied on the gross receipts derived from certain business activities. Unlike a general income tax that targets profits, TPT is levied on the revenue generated from the sale of goods or services. This distinction is important for financial planning and tax strategy.

The “Privilege” Aspect

The term “privilege” signifies that the government is allowing a business to operate and generate revenue. In return for this privilege, the business is obligated to collect and remit a tax on its transactions. This can be viewed as a form of compensation to the government for providing the infrastructure, legal framework, and services that enable businesses to thrive.

Taxable Activities

The specific activities subject to TPT vary by jurisdiction. Common taxable activities include:

- Retail Sales: The sale of tangible personal property to the final consumer for consumption or use. This is the most common form of TPT.

- Construction Contracting: For businesses involved in the construction, alteration, or repair of real property. TPT often applies to materials used and sometimes to the labor involved in such projects.

- Services: A growing number of jurisdictions are taxing specific business or personal services, such as repair services, cleaning services, telecommunications, and amusement services.

- Wholesale Sales: In some instances, TPT may apply to wholesale sales, though often at a different rate or with specific exemptions.

Rate Structures

TPT rates are determined by the governing body, typically the state and local municipalities. These rates can vary significantly based on:

- Jurisdiction: Different states, counties, and cities will have their own unique TPT rates.

- Business Classification: Certain types of businesses or industries may be subject to different tax rates. For example, restaurants might have a different rate than a retail clothing store.

- Type of Transaction: The rate might differ depending on whether it’s a sale of goods, a service, or a construction contract.

Key Differences from Sales Tax

While often used interchangeably, there are nuances that differentiate TPT from the more commonly understood “sales tax.” The primary distinction lies in the legal framework. Sales tax is typically levied on the buyer at the point of sale. TPT, as mentioned, is levied on the business for the privilege of conducting business, with the expectation that the business will pass this cost on to the consumer.

Burden of Collection

In a sales tax system, the retailer collects the tax from the buyer. In a TPT system, the business is responsible for remitting the tax to the state, having collected it from the customer. The legal obligation to remit the tax ultimately rests with the business, even if the economic burden is intended to be borne by the consumer.

Exemptions and Deductions

Both sales tax and TPT systems have exemptions and deductions designed to promote certain economic activities or provide relief. These can include:

- Resale Exemptions: Sales made for the purpose of resale are typically exempt, as the tax will be collected at the next point of sale.

- Exemptions for Certain Goods/Services: Some jurisdictions exempt essential items like groceries or prescription drugs.

- Non-profit Exemptions: Charitable organizations or educational institutions may be exempt from paying or collecting TPT.

- Geographic Exemptions: Businesses operating in specific enterprise zones or redevelopment areas might receive tax incentives.

Navigating TPT Compliance for Businesses

For businesses, effective TPT management is not just about paying taxes; it’s about ensuring accurate record-keeping, proper collection, timely remittance, and staying abreast of evolving regulations. Non-compliance can lead to significant penalties, including interest, fines, and even business closure.

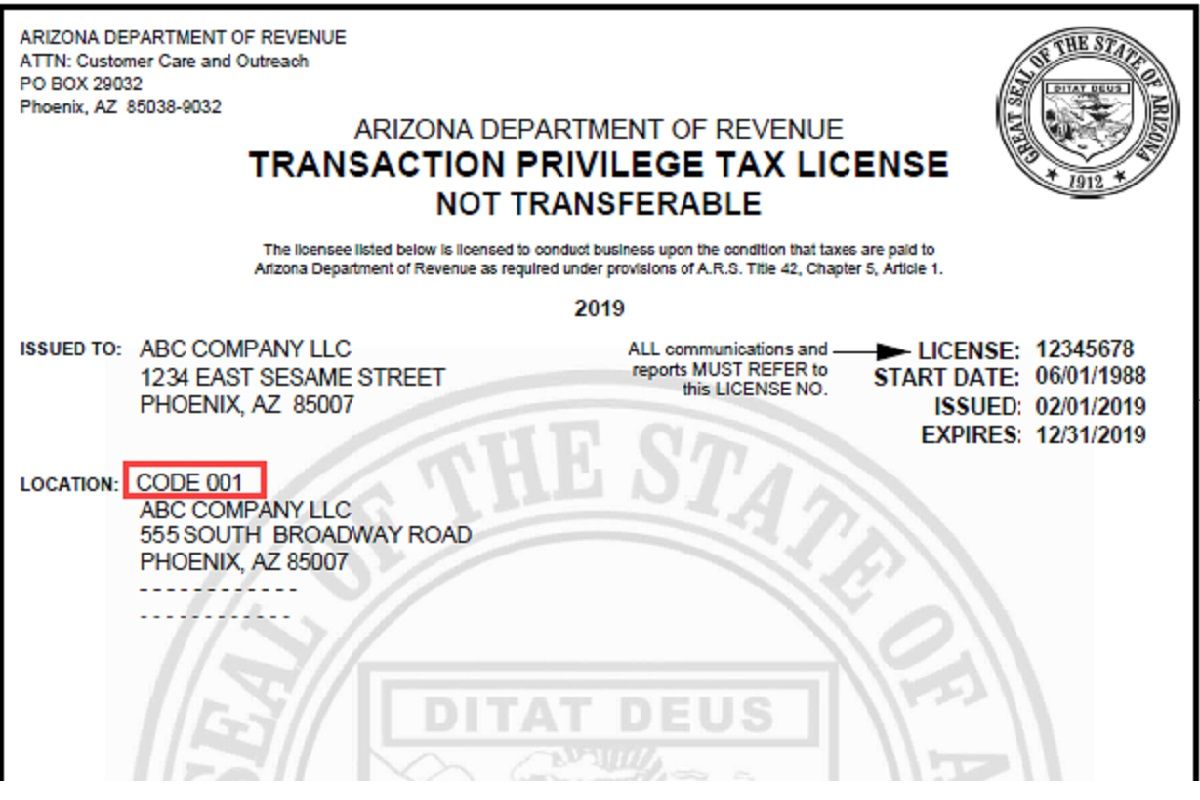

Registration and Licensing

The first step for any business operating in a TPT jurisdiction is to register with the relevant tax authority. This typically involves obtaining a TPT license or permit. This license often needs to be displayed prominently and used on all relevant business documentation.

Obtaining a TPT License

The process for obtaining a TPT license usually involves:

- Application: Completing an application form with details about the business, its owners, and its expected revenue.

- Business Structure: Providing information on the legal structure of the business (sole proprietorship, partnership, LLC, corporation).

- Tax Identification Numbers: Supplying federal and state tax identification numbers.

- Fees: Paying any required licensing fees.

Renewals and Updates

TPT licenses often require periodic renewal. It’s also crucial to update the licensing authority with any changes to the business, such as a change in ownership, business address, or primary business activities.

Record-Keeping and Documentation

Meticulous record-keeping is the bedrock of TPT compliance. Businesses must maintain detailed records of all sales, purchases, and tax collected.

Essential Records to Maintain

- Sales Invoices: Detailed invoices showing the itemized price of goods or services, applicable tax rates, and the total amount of TPT collected.

- Purchase Records: Documentation for items purchased for resale, including resale certificates if applicable.

- Exemption Certificates: Properly completed exemption certificates from customers who claim an exemption from TPT.

- Tax Return Filings: Copies of all filed TPT returns and proof of payment.

- Bank Statements: Records that can reconcile tax collections with remittances.

The Importance of Resale Certificates

Resale certificates are a critical tool for businesses that sell goods to other businesses for resale. By obtaining a valid resale certificate, a business can exempt the sale from TPT. However, it is the responsibility of the seller to ensure the certificate is valid and that the buyer is genuinely purchasing for resale. Misuse of resale certificates can result in penalties for both parties.

Filing and Remittance

TPT returns are typically filed on a periodic basis, most commonly monthly or quarterly. The frequency is often determined by the business’s gross sales volume.

Filing Methods

Tax authorities usually offer multiple filing methods, including:

- Online Filing: Many jurisdictions provide online portals for electronic filing and payment, which is often the most efficient and accurate method.

- Paper Filing: While less common, some businesses may still be able to file paper returns.

Payment Options

Payment of TPT can typically be made through various channels:

- Electronic Funds Transfer (EFT): Direct withdrawal from a business bank account.

- Online Payment: Via credit card or e-check through the tax authority’s portal.

- Mail: Sending a check or money order with the filed return.

Deadlines and Penalties

Strict adherence to filing and payment deadlines is paramount. Missing a deadline can trigger penalties and interest charges, which can quickly accumulate. It is advisable for businesses to establish internal systems that ensure timely remittance, perhaps well in advance of the actual due date.

Impact of TPT on Business Operations and Pricing

TPT has a direct influence on a business’s financial health, pricing strategies, and customer interactions. Understanding these impacts allows businesses to mitigate potential negative effects and leverage TPT knowledge to their advantage.

Pricing Strategies

The most immediate impact of TPT is on pricing. Businesses must factor the TPT rate into their product or service pricing to ensure they can cover the tax obligation without eroding their profit margins.

Incorporating TPT into Price Calculations

- Gross vs. Net Pricing: Businesses must decide whether to advertise prices that include TPT or if TPT will be added at the point of sale. Advertising gross prices (including TPT) can be appealing to consumers but requires careful internal calculation to ensure profitability.

- Competitive Analysis: Understanding how competitors price their goods and services, especially in relation to TPT, is crucial.

- Round Numbers and Psychological Pricing: Businesses may adjust their base prices to result in rounder TPT-inclusive totals for customer convenience.

Impact on Profit Margins

If a business fails to accurately account for TPT in its pricing, its profit margins will shrink. For example, if a business assumes a 5% TPT and the actual rate is 7%, the business will have to absorb the additional 2% from its own profits if it doesn’t adjust its pricing.

Customer Perception and Transparency

How TPT is presented to the customer can significantly affect their perception of value and trust.

Clear Communication

Transparency is key. Clearly itemizing TPT on receipts and sales documents helps customers understand what they are paying. Vague or hidden TPT charges can lead to dissatisfaction and distrust.

The Role of TPT in Economic Development

While TPT is a revenue source for governments, its implementation can also have broader economic implications. Some jurisdictions use TPT as a funding mechanism for local infrastructure projects, public services, or business development initiatives. This can, in turn, create a more favorable business environment in the long run. However, high TPT rates can sometimes deter consumers and businesses, potentially impacting economic growth.

Record-Keeping and Accounting Systems

Robust accounting systems are essential for managing TPT accurately. This involves not only tracking sales but also properly categorizing transactions and applying the correct tax rates.

Software Solutions

Many accounting software packages are designed to handle TPT calculations automatically. These systems can:

- Track Tax Rates: Store and apply different TPT rates based on location and transaction type.

- Generate Reports: Produce detailed reports for tax filing and auditing purposes.

- Manage Exemptions: Facilitate the tracking and application of exemption certificates.

Internal Controls

Implementing strong internal controls ensures that TPT is collected and remitted correctly. This might involve segregation of duties, regular audits of sales records, and mandatory training for staff involved in sales and customer service.

Common TPT Challenges and Best Practices

Businesses operating under TPT regimes often encounter a range of challenges. Proactive planning and adherence to best practices can significantly mitigate these issues.

Understanding Complex Tax Laws

TPT laws can be intricate and subject to frequent changes. Keeping up with these amendments requires ongoing vigilance.

Staying Informed

- Tax Authority Websites: Regularly monitoring the websites of state and local tax authorities for updates, bulletins, and revised regulations.

- Professional Advisors: Engaging with tax professionals (accountants, tax attorneys) who specialize in TPT can provide invaluable guidance and ensure compliance.

- Industry Associations: Many industry associations offer resources and training on tax compliance specific to their sector.

Audits and Compliance Reviews

Tax authorities conduct audits to ensure businesses are correctly collecting and remitting TPT. A well-prepared business can navigate an audit smoothly.

Preparing for an Audit

- Organized Records: Ensure all financial and tax records are meticulously organized and readily accessible.

- Knowledge of TPT Laws: Have a thorough understanding of the TPT laws applicable to your business.

- Professional Assistance: Have your tax advisor present during the audit.

Multijurisdictional Operations

For businesses operating in multiple cities, counties, or states with different TPT rules, compliance becomes significantly more complex.

Strategies for Multijurisdictional Businesses

- Tax Matrix: Develop a comprehensive tax matrix that outlines all applicable TPT rates, rules, and filing requirements for each jurisdiction.

- Nexus Determination: Understand the concept of “nexus” – the sufficient connection a business has with a state that requires it to collect and remit taxes there. This can be physical presence or economic activity.

- Specialized Software: Utilize accounting or tax software that can manage complex, multijurisdictional TPT requirements.

![]()

Best Practices for TPT Management

- Accurate Tax Rate Determination: Ensure you are using the correct TPT rates for all your sales, considering the specific location of the transaction and the nature of the goods or services.

- Prompt Filing and Payment: Never miss a filing deadline. Automate reminders and, if possible, set up electronic payments in advance.

- Continuous Training: Regularly train employees on TPT collection procedures, the importance of exemption certificates, and customer interaction protocols.

- Regular Review: Periodically review your TPT collection and remittance processes to identify any inefficiencies or potential errors.

By embracing a proactive and informed approach, businesses can effectively manage their Transaction Privilege Tax obligations, ensuring compliance, safeguarding their financial health, and fostering stronger customer relationships.