Convertible loans represent a fascinating and flexible financing instrument, particularly prevalent in the startup and early-stage company ecosystem. They offer a bridge between traditional debt and equity financing, providing capital to businesses while deferring the complex and often contentious valuation discussions that come with a direct equity investment. For founders navigating the early stages of growth, understanding convertible loans is crucial for strategic fundraising and financial planning. For investors, they offer a way to enter promising ventures with a degree of downside protection while retaining the potential for significant upside.

The Mechanics of a Convertible Loan

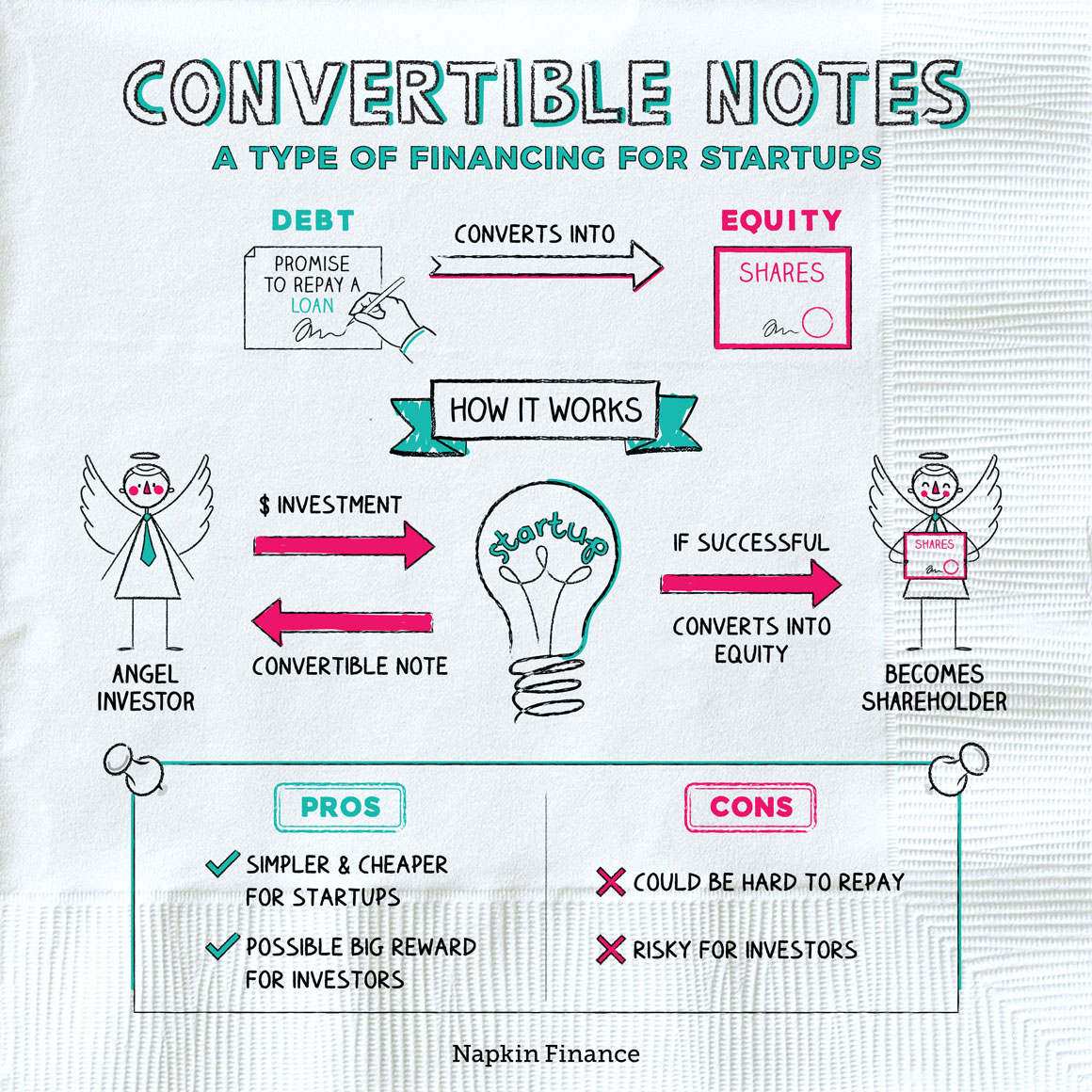

At its core, a convertible loan is a debt instrument that has the option to convert into equity at a later date, typically during a future priced equity financing round. This dual nature – debt with an equity conversion feature – is what makes it so attractive.

Debt Provisions

Like any loan, a convertible loan comes with specific debt provisions:

- Principal Amount: This is the initial sum of money lent to the company.

- Interest Rate: Convertible loans accrue interest, which can be paid in cash periodically, compounded and added to the principal, or sometimes waived upon conversion. The interest rate is typically set at a market rate for debt.

- Maturity Date: This is the date by which the loan must be repaid or converted. If neither occurs, the terms of the loan agreement dictate the consequences, which could include repayment of the principal and accrued interest in cash, or potentially a default scenario.

- Security/Collateral: While many convertible notes for startups are unsecured, more significant loans might require collateral, similar to traditional debt.

Equity Conversion Feature

The “convertible” aspect is where the magic happens. This feature allows the loan, and any accrued interest, to transform into shares of the company’s stock under specific conditions:

- Trigger Event: The most common trigger event is a “Qualified Financing Round” or “Equity Financing Round.” This is typically defined as the company raising a certain minimum amount of capital through the sale of preferred stock. This minimum threshold is important to ensure that the valuation is established by a significant funding event, not a minor one.

- Conversion Price: This is the price per share at which the loan converts into equity. There are two primary mechanisms for determining this conversion price, which are key negotiation points:

- Discount: The loan converts at a discount to the price per share paid by the new investors in the qualified financing round. For example, a 20% discount means the loan converts at 80% of the Series A price. This is an incentive for the early lenders, rewarding them for taking on earlier risk.

- Valuation Cap: This sets a maximum valuation at which the loan will convert, regardless of how high the valuation is in the subsequent priced round. For instance, a $10 million valuation cap means that even if the company raises its Series A at a $20 million pre-money valuation, the convertible loan will convert as if the valuation were only $10 million. This protects the early investors from dilution in a very successful, high-valuation round.

- Interest Conversion: Often, accrued interest on the loan can also be converted into equity, either at the same conversion price as the principal or at a different, pre-agreed rate. This further incentivizes early investment.

Key Terms and Considerations

Beyond the fundamental debt and conversion mechanics, several other terms are critical in a convertible loan agreement:

- Seniority: The position of the convertible loan relative to other debt or equity in the company’s capital structure.

- Covenants: Promises made by the company to the lender, such as maintaining certain financial ratios or refraining from specific actions.

- Default Provisions: What happens if the company breaches the terms of the loan.

- Liquidation Preference: While a loan, in the event of a liquidation event (e.g., sale of the company, bankruptcy), the loan principal and interest would typically be repaid before equity holders receive anything, but after secured creditors. However, the specific liquidation preference might be negotiated.

- Protective Provisions: Rights granted to the noteholders to approve certain corporate actions, even before conversion.

Why Use Convertible Loans?

Convertible loans offer compelling advantages for both companies and investors, making them a popular choice for early-stage financing.

For the Company

- Deferring Valuation: This is arguably the biggest advantage. In the early days, a company’s valuation is highly speculative. A convertible loan allows the company to raise capital without needing to agree on a precise valuation, which can be a protracted and contentious process. This speeds up fundraising and allows management to focus on building the business.

- Speed and Simplicity: Compared to a full equity round, convertible notes can often be documented and closed more quickly, with less legal complexity and fewer parties involved.

- Flexibility: They provide a financial runway to achieve key milestones, prove the business model, and increase the company’s valuation before a formal equity round.

- Lower Dilution (Initially): While conversion does lead to dilution, the immediate dilution from a debt instrument is zero. Dilution is deferred until the equity round.

- Signaling: Raising capital through convertible notes can signal to future equity investors that the company has already attracted early-stage financial support.

For the Investor

- Downside Protection: As a debt instrument, investors have a higher claim on assets than equity holders. If the company fails before conversion, the debt must be repaid (though in a distressed scenario, recovery may be minimal).

- Upside Potential: The conversion feature allows investors to participate in the company’s future success. If the company performs well and achieves a high valuation in the subsequent equity round, the investor can benefit from a potentially lower effective purchase price of equity due to the discount and/or valuation cap.

- Lower Risk (Compared to Equity): By having a debt component and often a valuation cap, investors can mitigate some of the risks associated with early-stage equity investments.

- Simplicity: Convertible notes are often easier to negotiate and document than complex preferred equity rounds.

When Are Convertible Loans Most Effective?

Convertible loans are particularly well-suited for specific stages and circumstances:

- Seed and Pre-Seed Funding: This is the most common application. Companies with an idea, a prototype, or early traction but lacking a fully developed business plan and predictable revenue streams often use convertible notes to get off the ground.

- Bridging Rounds: A company might use a convertible note to raise capital between priced equity rounds to fund operations or a specific strategic initiative while preparing for a larger, more significant funding round.

- Uncertain Valuations: When founders and investors cannot agree on a fair valuation for the company due to market conditions, early-stage uncertainty, or differing perspectives on future potential.

- Speedy Capital Needs: When a company needs capital quickly to seize an opportunity or to avoid running out of cash, a convertible note can be a faster route than a full equity raise.

Alternatives to Convertible Loans

While convertible loans are popular, they are not the only option for early-stage financing. Other common alternatives include:

- Priced Equity Rounds (e.g., Seed Preferred Stock): This involves a direct sale of equity at a determined valuation. It is more complex and takes longer but provides clarity on ownership and valuation from the outset.

- SAFEs (Simple Agreement for Future Equity): Developed by Y Combinator, SAFEs are similar to convertible notes but are not debt. They are a contract to receive future equity in a company upon certain trigger events. They do not accrue interest and do not have maturity dates, making them simpler and more founder-friendly in some aspects.

- Revenue-Share Agreements: Investors provide capital in exchange for a percentage of the company’s future revenues, up to a certain multiple of the initial investment.

- Venture Debt (for more mature companies): This is traditional debt provided to venture-backed companies, often with warrants for equity. It’s typically for companies that have already raised significant equity capital.

Potential Drawbacks and Risks

Despite their advantages, convertible loans are not without their complexities and potential downsides:

- Future Valuation Uncertainty: While the immediate valuation is deferred, the ultimate conversion price and the resulting dilution can still be uncertain and may not be favorable to founders if the company performs exceptionally well in the next round.

- Potential for Conflict: Disagreements can arise regarding the definition of a “qualified financing round,” the valuation cap, or other conversion terms, especially if the company’s performance is significantly different from initial expectations.

- Complexity in Later Rounds: If a company raises multiple convertible notes with different terms, managing the conversion of all these notes in a subsequent equity round can become administratively complex.

- Interest Accrual: If the company struggles and cannot raise a priced round before the maturity date, it might face a significant cash repayment obligation for the principal and accrued interest, potentially leading to insolvency.

- Misalignment of Incentives: If the valuation cap is too low, it can create a significant misalignment of incentives where early investors gain a disproportionately large equity stake in a highly successful company, potentially at the expense of founders and later-stage investors.

Conclusion

Convertible loans are a powerful and versatile financial tool that has become a staple in the startup funding landscape. They offer a pragmatic solution for early-stage companies needing capital to grow while deferring the often-difficult task of valuation. For investors, they provide a blend of downside protection and the potential for substantial upside. However, like any financial instrument, a thorough understanding of their terms, potential implications, and comparison to alternative financing methods is essential for both founders and investors to make informed decisions and navigate the exciting, yet challenging, journey of building a successful enterprise. The skillful negotiation and structuring of a convertible loan can set a company on a strong path for future growth and development.