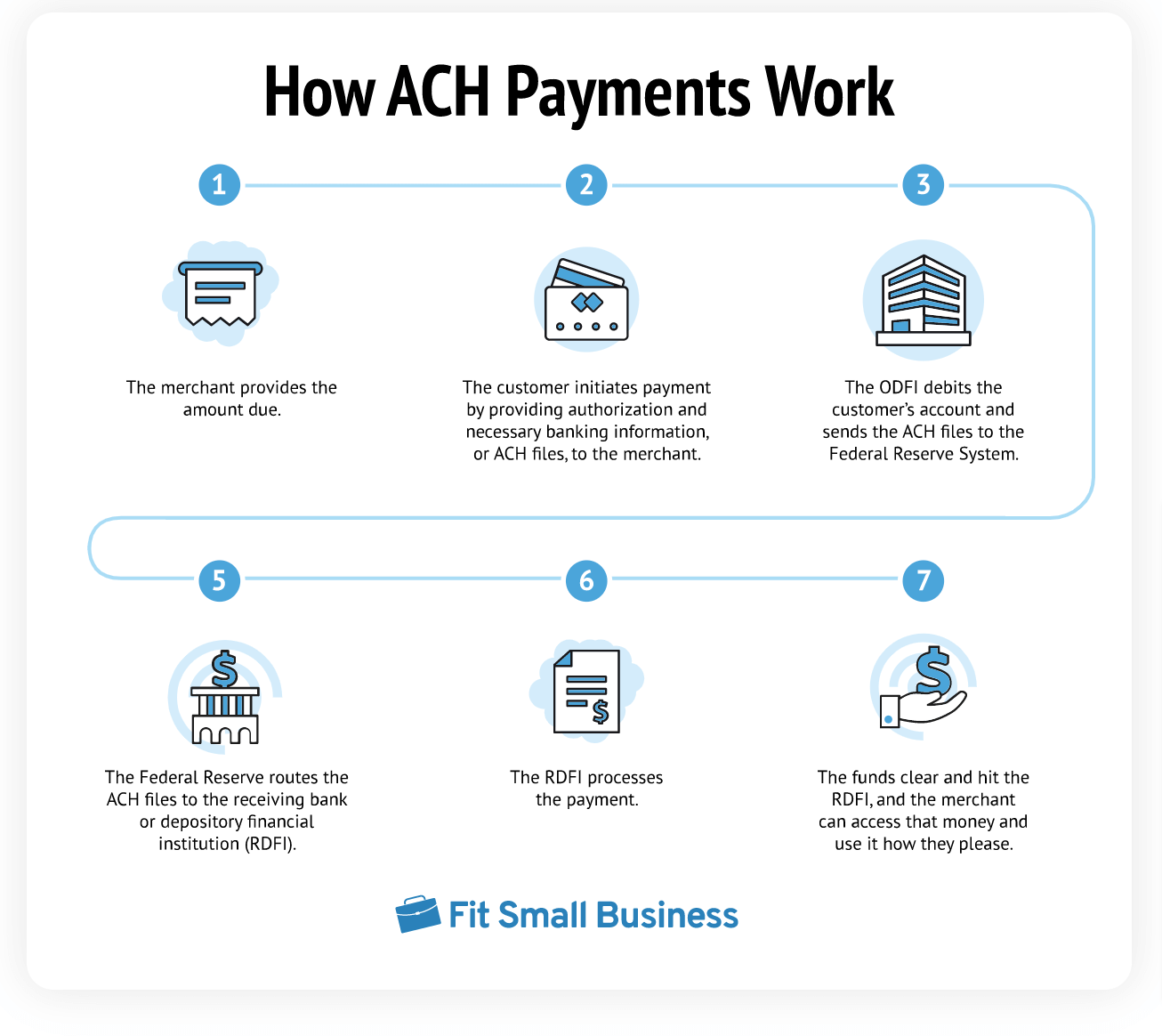

ACH (Automated Clearing House) payments are a cornerstone of modern electronic fund transfers in the United States. They facilitate direct deposits, bill payments, and business-to-business transactions efficiently and securely. Understanding the precise information required for a successful ACH payment is crucial for both individuals and businesses to avoid delays, rejections, and potential financial complications. This article will delve into the essential data points necessary to initiate and process an ACH payment, covering both originating and receiving parties.

Initiating an ACH Payment: The Payer’s Perspective

When you, as the payer, decide to send money via ACH, you are essentially authorizing a direct debit from your bank account or initiating a direct credit to another account. The accuracy and completeness of the information you provide are paramount.

Essential Account and Routing Details

At the heart of any ACH transaction lies the routing and account information of both the payer and the payee. Without these fundamental details, the payment simply cannot be directed to the correct financial institutions and accounts.

Bank Routing Number (ABA Routing Transit Number)

The Bank Routing Number, often referred to as the ABA Routing Transit Number (RTN), is a nine-digit code that identifies a specific financial institution within the United States. It’s akin to a postal code for banks.

- Purpose: This number allows the ACH network to determine which bank the funds should be transferred from or to.

- Format: Always nine digits.

- Acquisition: You can typically find your bank’s routing number on your checks (usually the first set of nine digits at the bottom left), on your bank statement, or by contacting your bank directly. For business accounts, especially those that might be part of a larger holding company, it’s crucial to ensure you have the correct routing number associated with the specific account intended for the transaction.

Bank Account Number

This is the unique identifier for your specific deposit or withdrawal account at a given financial institution.

- Purpose: This number pinpoints the exact account where funds will be debited or credited.

- Format: The length and format of account numbers vary significantly between financial institutions.

- Acquisition: Similar to the routing number, you can find your account number on your checks (usually the second set of numbers at the bottom, between the routing and check numbers), on your bank statements, or by logging into your online banking portal. Double-checking this number is critically important, as a single digit error can lead to the payment being sent to the wrong account, potentially causing significant reconciliation issues.

Payer Authorization and Transaction Details

Beyond account specifics, the payer must also provide explicit authorization and details about the transaction itself.

Payer’s Name and Address

While not always strictly required for every ACH transaction, including the payer’s full legal name and current address can significantly enhance security and aid in dispute resolution.

- Purpose: Verifies the identity of the individual or entity initiating the payment and can be used for record-keeping and compliance purposes.

- Importance: Some financial institutions or third-party processors may require this information to further validate the transaction and prevent fraud.

Transaction Type (Debit vs. Credit)

It’s vital to specify whether the ACH payment is a debit (money coming out of your account) or a credit (money going into your account).

- ACH Debit: This is when you authorize a company or individual to pull funds directly from your account to pay for a service, product, or bill.

- ACH Credit: This is when you initiate a payment to send funds to another account, such as direct deposit of payroll or a payment to a vendor.

Transaction Amount

The precise monetary value of the transaction must be clearly stated.

- Accuracy is Key: Any discrepancy between the authorized amount and the amount processed can lead to disputes.

- Format: Specify currency (USD in the U.S. context) and ensure correct decimal placement.

Transaction Reference or Memo

This field allows for a brief description of the payment.

- Purpose: Aids in record-keeping and reconciliation for both the payer and the payee. It helps identify what the payment is for (e.g., “Invoice #12345,” “Rent – May 2024,” “Payroll – Week of June 1st”).

- Best Practice: Be specific and consistent with your referencing to simplify tracking.

Authorization (Verbal or Written)

For ACH debits, the payer must provide explicit authorization to the payee. This is a legal requirement.

- Written Authorization: This is the most common and recommended form, often obtained through a signed authorization form, online agreement, or via an electronic checkbox during a checkout process. It should clearly state the terms of the debit, including the amount (or how it will be determined), frequency, and the authorization to debit the specified account.

- Verbal Authorization: While permissible in some contexts, it’s generally less secure and harder to prove. If verbal authorization is given, it’s best practice for the payee to follow up with written confirmation.

- Revocation: Payer should be aware of their right to revoke authorization, usually with advance notice as stipulated in the authorization agreement.

Receiving an ACH Payment: The Payee’s Requirements

For a payee to successfully receive an ACH payment, they must provide the necessary details to the originating party or their bank. The information required is largely mirrored from the payer’s side but pertains to the payee’s account.

Essential Account and Routing Details for the Payee

Just as the payer needs to provide their bank’s routing number and their account number, the payee must furnish these details to the payer or the payment processor.

Payee’s Bank Routing Number

The payee must provide the correct nine-digit routing number of the financial institution where they wish to receive the funds.

- Importance: Ensures the funds are directed to the correct bank.

- Verification: Payees should confirm their routing number through their bank statements or by contacting their bank.

Payee’s Bank Account Number

The payee’s unique account number at their financial institution is essential for the funds to be deposited.

- Accuracy is Critical: An incorrect account number will lead to the payment failing or being misdirected.

- Confidentiality: Payees should only share this information with trusted parties who require it for legitimate transactions.

Payee Information for Transaction Processing

In addition to banking details, the payee may need to provide other information, especially in business contexts.

Payee’s Full Legal Name and Address

For business transactions, the payee’s full legal business name and registered address are often required.

- Purpose: Used for verification, compliance, and official record-keeping, especially for businesses.

- Consistency: Ensure this information matches the details registered with their financial institution.

Company Identification (if applicable)

For business-to-business transactions, the payee might need to provide their Employer Identification Number (EIN) or Taxpayer Identification Number (TIN).

- Purpose: Essential for tax reporting and compliance, especially for payments that might be considered income.

- Security: This is sensitive information that should be handled with extreme care.

Type of Transaction Expected

While the payer typically specifies debit or credit, the payee needs to be aware of what type of transaction they are expecting.

- Receiving a Direct Deposit: This is an ACH Credit.

- Being Billed via ACH: This is an ACH Debit, and the payee would have provided their authorization details previously.

Considerations for Different ACH Transaction Types

The specific information required can also depend on the nature and purpose of the ACH transaction.

Direct Deposit (Payroll, Government Benefits)

For receiving direct deposits, the employee or beneficiary needs to provide their employer or the disbursing agency with:

- Their full legal name.

- Their bank routing number.

- Their bank account number.

- Often, a voided check or bank direct deposit form is required as verification.

Bill Payments (Utilities, Loans, Subscriptions)

When setting up recurring or one-time bill payments via ACH debit, the consumer typically provides:

- The biller’s name and the specific service/account number being paid.

- Their bank routing number.

- Their bank account number.

- Authorization details, which may be an electronic signature on a web form or a physical signed document.

Business-to-Business (B2B) Payments

B2B ACH transactions often involve more comprehensive data to facilitate accounting and reconciliation. This can include:

- Payer and Payee full legal names, addresses, and contact information.

- Bank routing numbers and account numbers for both parties.

- Detailed invoice numbers, purchase order numbers, or other transaction identifiers.

- Specific authorization details for debits.

- Information for tax reporting (EIN/TIN) may be exchanged.

Ensuring a Smooth ACH Transaction

To maximize the chances of a successful ACH payment and minimize issues, always adhere to these best practices:

- Double-Check All Information: Before submitting any payment details, meticulously review the routing number, account number, and amount for accuracy.

- Use Official Sources: Obtain routing and account numbers directly from your bank statements, checks, or by contacting your bank. Avoid relying on third-party lists that might be outdated or incorrect.

- Understand Authorization: For ACH debits, ensure you fully understand the terms and conditions of the authorization you are providing. Keep copies of any authorization agreements.

- Maintain Records: Keep detailed records of all ACH transactions, including dates, amounts, and any reference numbers. This is invaluable for financial management and dispute resolution.

- Communicate Clearly: If you are an originator of a payment, communicate clearly with the payee about the information you require. If you are the payee, ensure you provide all necessary details accurately and promptly.

- Consult Your Bank: If you have any doubts or questions about ACH payment requirements, your financial institution is the best resource for accurate and up-to-date information. They can guide you on specific formats, security protocols, and potential limitations.

By understanding and diligently providing the correct information, both payers and payees can leverage the efficiency and security of ACH payments, ensuring seamless financial transactions for a wide range of purposes.