The phrase “sell to close” is a fundamental concept within options trading, specifically referring to the act of closing out a previously established options position by taking the opposite action. For an options trader, understanding how to effectively “sell to close” is as crucial as understanding how to “buy to open.” This action allows traders to realize profits, limit losses, or adjust their overall portfolio strategy before an options contract expires. At its core, “sell to close” is the mechanism by which a trader exits a long position in an option contract.

Understanding Long and Short Options Positions

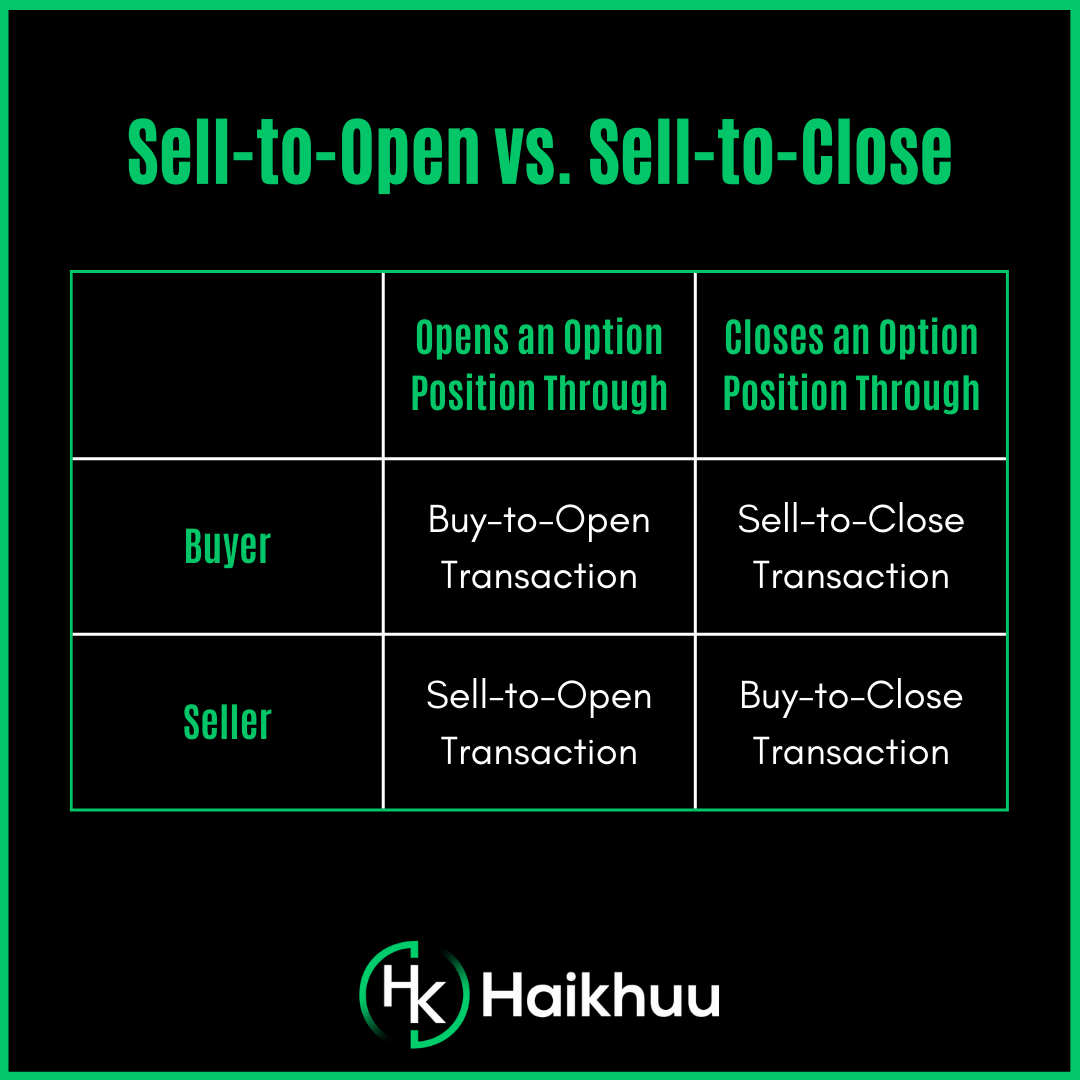

Before delving into the nuances of “sell to close,” it’s imperative to grasp the basic mechanics of being long or short an option. When a trader buys an option contract – whether it’s a call or a put – they are establishing a long position. This means they own the right, but not the obligation, to buy or sell the underlying asset at a specified price (the strike price) on or before a certain date (the expiration date).

Conversely, when a trader sells an option contract without already owning it, they are establishing a short position. In this scenario, they have sold the right to someone else and, in doing so, have taken on the obligation to buy or sell the underlying asset if the option buyer decides to exercise their right.

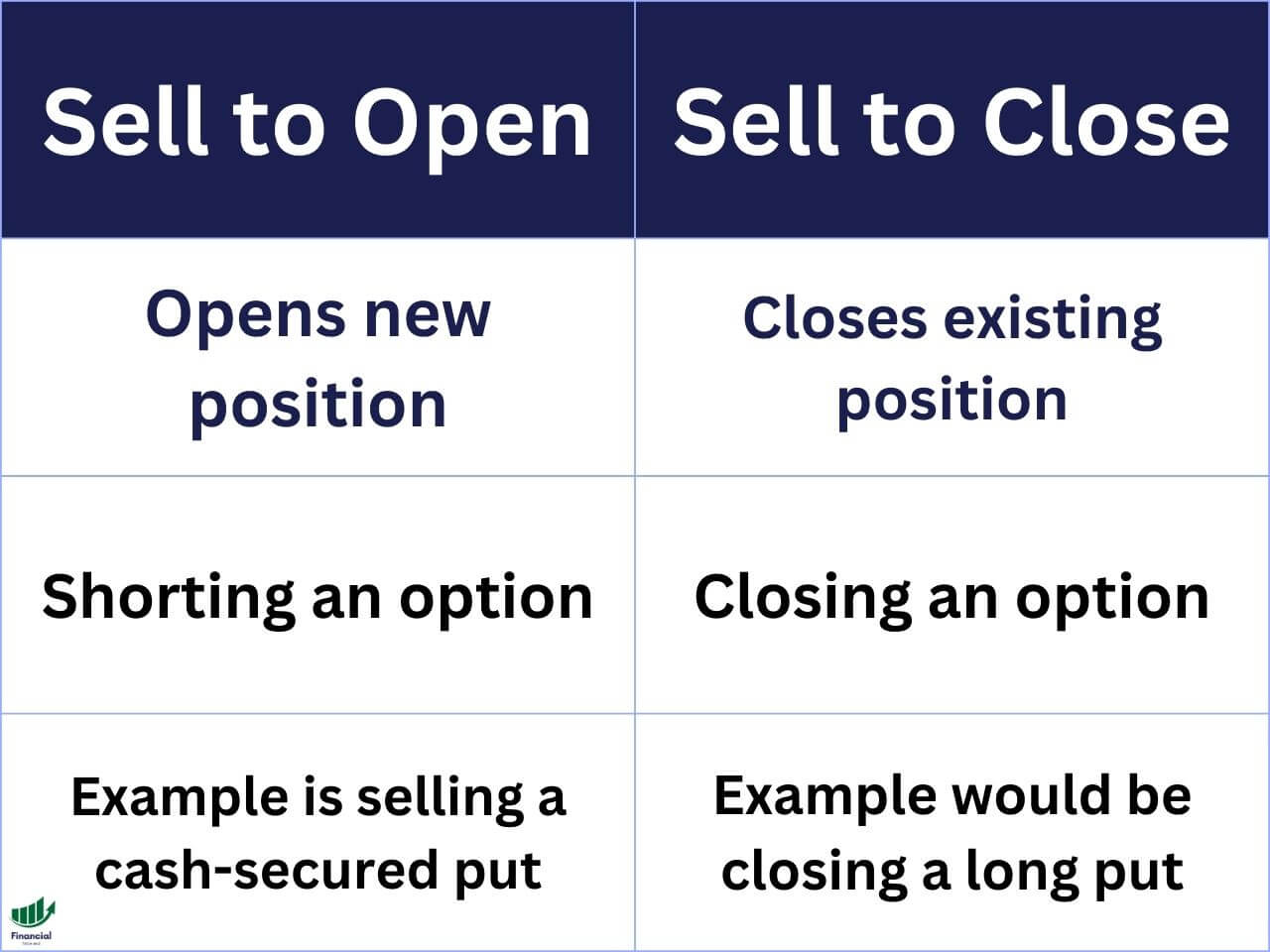

The “sell to close” action is specifically related to unwinding a long position. If you are long an option, you bought it initially. To exit this position, you must sell that same option contract.

Buying to Open vs. Selling to Close

The initial action of entering a long options position is referred to as “buying to open.” For example, if you believe the price of a stock will rise, you might “buy to open” a call option. This means you are purchasing the right to buy the stock at a certain price.

The complementary action to “sell to close” for a long position is “buying to close” for a short position. If you initially sold a call option (a short call), you would then “buy to close” that same call option to exit your obligation. This article, however, focuses solely on the act of “selling to close” a long option position.

The Mechanics of Selling to Close

When you “sell to close” an option, you are selling an option contract that you previously purchased. The primary reasons for doing so include:

- Realizing Profits: If the underlying asset’s price has moved favorably, the value of your long option will have increased. Selling to close allows you to capture this profit before expiration.

- Limiting Losses: If the underlying asset’s price has moved unfavorably, the value of your long option will have decreased. Selling to close can help cut your losses by exiting the position before it loses all its remaining value.

- Adjusting Strategy: Market conditions can change, or your investment thesis might evolve. Selling to close allows you to reallocate capital or adjust your overall portfolio strategy.

- Avoiding Assignment (for Long Calls): If you are long a call option and the option is in-the-money near expiration, you might choose to sell to close to avoid the obligation of buying the underlying stock.

Consider an example: Suppose you bought one call option contract for XYZ stock at a strike price of $100, expiring in one month, for a premium of $5 per share (total cost $500, as one contract represents 100 shares).

- Scenario 1: Profit Taking. If XYZ stock rises to $115 before expiration, the call option’s value will likely increase significantly. You could then “sell to close” this call option for, say, $12 per share (total sale proceeds $1200). Your net profit would be $1200 (proceeds) – $500 (initial cost) = $700, minus commissions and fees.

- Scenario 2: Loss Limitation. If XYZ stock drops to $90 before expiration, the call option will likely have lost value. You might decide to “sell to close” the option for $1 per share (total sale proceeds $100) to prevent further losses. Your net loss would be $500 (initial cost) – $100 (proceeds) = $400, minus commissions and fees, rather than the full $500 if you held until expiration.

Strategies Employing “Sell to Close”

The decision to “sell to close” is not arbitrary. It’s often driven by specific trading strategies aimed at maximizing returns or managing risk effectively. These strategies involve understanding the time decay (theta), volatility changes (vega), and directional movements of the underlying asset.

Profit-Taking Strategies

A common goal for many options traders is to capture profits as they accrue. “Sell to close” is the direct mechanism for this. Traders often set profit targets, either as a percentage of their initial investment or a specific dollar amount. Once the option reaches this target value, they execute the “sell to close” order.

- Percentage-Based Targets: A trader might aim to sell a call option to close once its value has doubled from the purchase price. For instance, if they bought a call for $5, they might set a target to sell it for $10.

- Dollar-Amount Targets: Alternatively, a trader might have a fixed profit goal for the entire trade, considering the total capital invested.

- Trailing Stop Orders: For more automated profit-taking, traders can use trailing stop orders. A trailing stop order to “sell to close” would automatically trigger a market or limit order if the option’s price moves favorably by a specified amount or percentage but then reverses. This allows traders to lock in profits as the price moves up without having to manually monitor the market constantly.

Loss-Limitation Strategies (Stop-Loss)

Conversely, “sell to close” is also critical for risk management. Many traders implement stop-loss orders to limit potential downside. A stop-loss order is an order placed with a broker to buy or sell a security when it reaches a certain price. When applied to a long option position, a stop-loss order to “sell to close” will trigger if the option’s price falls to a predetermined level, thereby cutting the loss.

- Fixed Percentage Stop: A trader might decide they are willing to lose no more than 20% of their initial investment on any given options trade. If they bought an option for $5, a 20% loss would be $1. A stop-loss order to “sell to close” would be placed at $4.

- Fixed Dollar Amount Stop: Similar to percentage-based stops, a trader might set a maximum dollar amount they are willing to lose per contract.

- Time-Based Exits: Sometimes, even if an option is not yet at its stop-loss price, a trader might decide to “sell to close” if the underlying asset is not moving as expected or if expiration is approaching and the option is losing value rapidly due to time decay.

Adjusting Positions and Hedging

“Sell to close” is also an integral part of more complex options strategies, such as spreads, and can be used for hedging purposes.

- Spread Strategies: In strategies like a vertical spread (bull call spread, bear put spread), traders simultaneously buy one option and sell another. If the trader wants to exit the entire spread position before expiration, they would “sell to close” the option they initially bought and “buy to close” the option they initially sold.

- Hedging: A trader might hold a long position in a stock and buy put options to protect against a potential price decline. If the stock price begins to fall, they might “sell to close” their put options to realize profits from the hedge, offsetting some of the losses in their stock position. Conversely, if the stock price rises significantly and the need for the hedge diminishes, they might “sell to close” the put options to avoid potential losses due to time decay or volatility changes.

The Impact of Time Decay (Theta) and Volatility (Vega)

When deciding whether to “sell to close,” traders must consider external factors that influence an option’s price, most notably time decay (theta) and implied volatility (vega).

Time Decay (Theta)

Theta measures the rate at which an option’s value erodes as it approaches its expiration date. For long option holders, theta is a negative factor – it represents a cost. As time passes, the probability of the option expiring in-the-money decreases, and therefore, its extrinsic value diminishes.

- Early Exits for Long Calls/Puts: If a long call or put option is not moving favorably and is losing value rapidly due to time decay, a trader might choose to “sell to close” to salvage any remaining premium, even if it means taking a loss. This is particularly important as expiration nears.

- Maximizing Theta Decay: Conversely, traders who are short options benefit from theta decay. If they are short an option and it’s nearing expiration with little movement, they might hold on to collect the full premium. However, if they are long and theta is working against them, selling to close becomes a pressing consideration.

Implied Volatility (Vega)

Vega measures an option’s sensitivity to changes in implied volatility. Implied volatility reflects the market’s expectation of future price swings in the underlying asset. For long option holders, an increase in implied volatility is generally beneficial, as it increases the option’s price. A decrease in implied volatility has the opposite effect.

- Selling to Close During High Volatility: If a trader buys an option and implied volatility subsequently rises, the option’s price will increase. This presents an opportunity to “sell to close” and lock in profits that are partly driven by increased uncertainty.

- Holding Through Volatility Declines: If a trader buys an option and implied volatility decreases, the option’s price will fall, even if the underlying asset’s price remains unchanged. In such a scenario, a trader might choose to hold their position and wait for volatility to potentially rebound or for the underlying asset to move favorably, rather than “sell to close” at a depressed price. However, if the decline in volatility is significant and the option’s value is substantially reduced, selling to close might be the prudent choice to limit further erosion.

Order Types for “Sell to Close” Transactions

Just as there are different ways to open an options position, there are various order types that can be used when executing a “sell to close” transaction. The choice of order type can significantly impact the execution price and the certainty of the trade being filled.

Market Orders

A market order to “sell to close” is an instruction to sell the option at the best available price in the current market. This order type prioritizes speed of execution over price. It will almost always be filled, but the execution price might be less favorable than anticipated, especially in volatile markets or for thinly traded options where the bid-ask spread is wide.

- Pros: Guarantees execution.

- Cons: Price uncertainty; potential for slippage (execution at a worse price than expected).

- When to Use: When exiting a position quickly is more important than achieving a specific price, such as when exiting a losing trade to prevent further damage or when a rapid market move necessitates an immediate exit.

Limit Orders

A limit order to “sell to close” allows the trader to specify the minimum price at which they are willing to sell the option. The order will only be executed if the market reaches or exceeds that specified price.

- Pros: Price control; protection against unfavorable execution prices.

- Cons: No guarantee of execution; the order may not be filled if the market price does not reach the limit price.

- When to Use: When profit targets are in place, or when exiting a profitable trade at a desired price is paramount. It’s also useful for avoiding slippage in less liquid options.

Stop Orders and Stop-Limit Orders

As discussed in the context of loss limitation, stop orders are used to trigger a market or limit order once a certain price level is reached.

- Stop Order to Sell to Close: When the option price falls to the stop price, it converts into a market order to sell. This is a risk-management tool to exit a losing position.

- Stop-Limit Order to Sell to Close: When the option price falls to the stop price, it converts into a limit order to sell at the specified limit price. This offers price control after the stop level is breached but, like a regular limit order, carries the risk of not being filled if the price moves rapidly past the limit.

Understanding these order types and their implications is crucial for effectively managing options trades and executing “sell to close” orders at opportune moments.

Conclusion: The Strategic Importance of “Sell to Close”

The act of “selling to close” is far more than a simple transactional step in options trading; it is a strategic maneuver that empowers traders to realize profits, mitigate risk, and adapt to dynamic market conditions. Whether it’s capturing gains from a favorable price movement, cutting losses before they become substantial, or adjusting a complex options strategy, the ability to effectively “sell to close” is a cornerstone of successful options portfolio management. Mastery of this concept, coupled with an understanding of underlying factors like time decay and volatility, and the judicious use of order types, allows traders to navigate the intricate world of options with greater confidence and precision. It transforms a passive holding into an active management process, where timely decisions to exit a position can be as critical as the initial decision to enter it.