The world of financial planning and investment can often feel like a labyrinth, with an array of products and strategies designed to secure one’s future. Among these, annuities have long held a prominent position, offering a pathway to predictable income streams. While many are familiar with traditional annuity structures, newer, more specialized forms are emerging, catering to specific investor needs and market trends. One such product, the “Myga Annuity,” has begun to capture attention. But what exactly is a Myga Annuity, and how does it fit into the broader landscape of retirement planning? This exploration aims to demystify this specific financial instrument, outlining its core features, potential benefits, and considerations for investors.

Understanding the Foundation: What is an Annuity?

Before delving into the specifics of a Myga Annuity, it is crucial to establish a foundational understanding of what an annuity, in general, entails. An annuity is a contract between an individual and an insurance company. In exchange for a lump-sum payment or a series of payments, the insurance company promises to make periodic payments to the individual, either immediately or at some point in the future. These future payments are typically used to supplement retirement income.

The primary appeal of annuities lies in their ability to provide a guaranteed stream of income for a specified period or for the rest of an annuitant’s life, regardless of market fluctuations. This offers a sense of security, particularly for individuals approaching or in retirement, who may be concerned about outliving their savings or weathering economic downturns.

Types of Annuities

Annuities come in various forms, each with distinct characteristics and risk profiles:

- Immediate Annuities: These annuities begin paying out income shortly after the initial purchase. They are often favored by retirees who need immediate income supplementation.

- Deferred Annuities: These annuities allow contributions to grow over time, with payouts beginning at a future date chosen by the annuitant. This growth can be tax-deferred, meaning taxes are not paid until the income is withdrawn.

- Fixed Annuities: These offer a guaranteed rate of return on the principal invested. They are considered less risky but generally provide lower growth potential compared to variable annuities.

- Variable Annuities: These allow investors to allocate their premiums among various investment options, similar to mutual funds. The returns are tied to the performance of these underlying investments, offering higher growth potential but also greater risk.

- Indexed Annuities: These offer a hybrid approach, with returns linked to a specific market index (like the S&P 500), but with a floor that protects against losses. They aim to provide growth potential while offering some downside protection.

Introducing the Myga Annuity

The “Myga Annuity” is not a universally recognized, distinct financial product with a standardized definition across the entire insurance and investment industry. Instead, it is most likely a term that refers to a specific type or feature within existing annuity structures, or it might be a proprietary product name used by a particular financial institution. Given the typical nomenclature in financial services, “Myga” could potentially be an acronym or a descriptive term that highlights a key characteristic of the annuity.

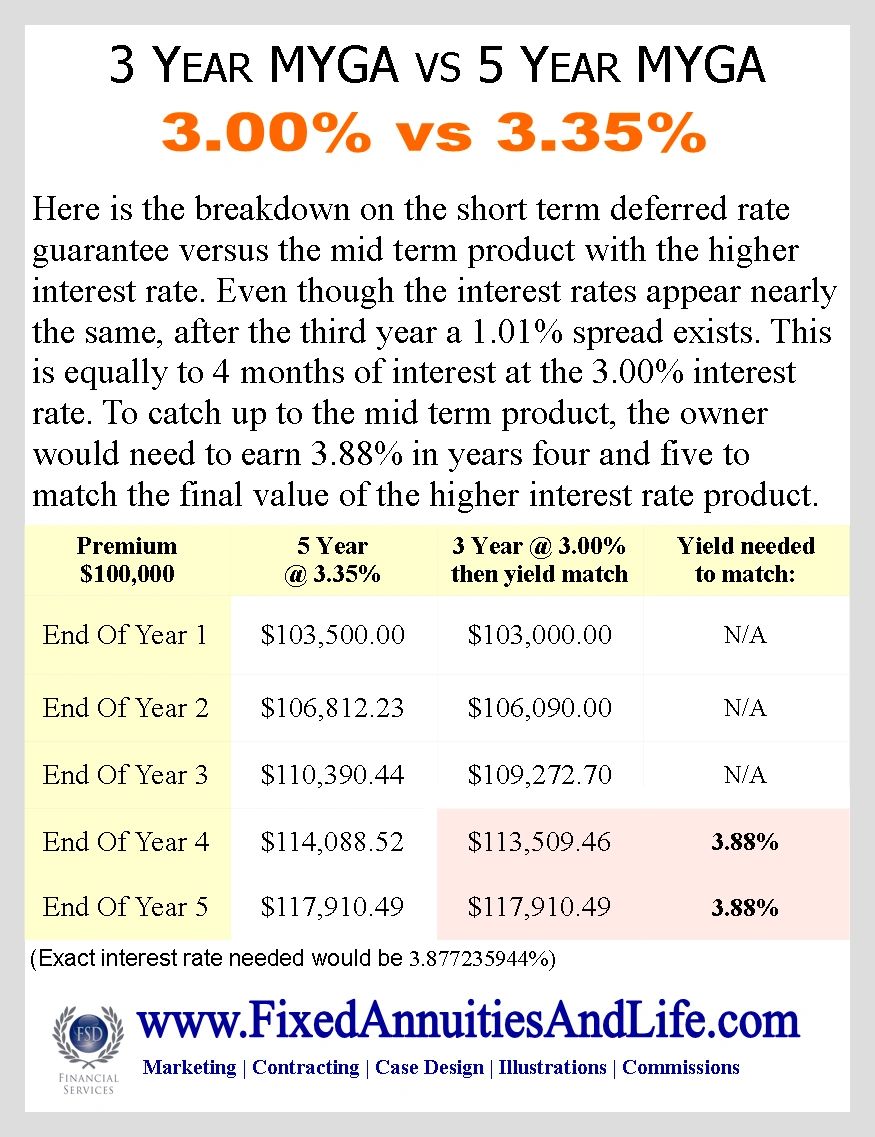

One of the most probable interpretations of “Myga Annuity” points to a Multi-Year Guaranteed Annuity (MYGA). This is a widely accepted and well-defined category of fixed annuity that has gained significant traction in recent years, particularly in low-interest-rate environments where investors seek stable, predictable returns.

The Core of a Multi-Year Guaranteed Annuity (MYGA)

A Multi-Year Guaranteed Annuity (MYGA) is a type of fixed annuity where the insurance company guarantees a specific interest rate on the principal for a predetermined period, typically ranging from three to ten years. During this guarantee period, the annuitant’s money grows at a fixed, predictable rate, offering a solid alternative to traditional savings accounts or Certificates of Deposit (CDs) that may offer lower rates or less security.

Key Features of a MYGA:

- Guaranteed Interest Rate: This is the hallmark of a MYGA. The insurance company locks in an interest rate for the duration of the contract. This rate is typically higher than what might be found in standard savings accounts or short-term CDs, especially when market interest rates are low.

- Fixed Term: The guarantee period is explicitly defined at the outset of the contract. For example, a 5-year MYGA will offer a set interest rate for five years.

- Tax-Deferred Growth: Like other deferred annuities, earnings within a MYGA grow on a tax-deferred basis. This means that taxes are not due on the interest earned until the money is withdrawn. This allows for greater compounding over time.

- Safety and Security: MYGAs are backed by the financial strength of the issuing insurance company. As long as the insurer remains solvent, the principal and the guaranteed interest are protected. This makes them a relatively safe investment option for individuals concerned about capital preservation.

- Liquidity and Surrender Charges: While MYGAs offer a fixed rate for a set term, accessing funds before the end of that term usually incurs surrender charges. These charges are designed to compensate the insurance company for the loss of predictable investment. Most MYGAs offer a penalty-free withdrawal window each year, often allowing access to a certain percentage of the contract’s value.

Benefits of a Myga Annuity (MYGA)

The appeal of a MYGA lies in its ability to address several common financial objectives, particularly for those seeking a reliable and secure place to grow their savings.

Predictable Growth and Income Potential

The primary benefit of a MYGA is the certainty of its returns. In an environment where interest rates can be volatile, knowing that your principal will grow at a specific, guaranteed rate for several years provides immense peace of mind. This predictability is especially valuable for individuals approaching retirement who want to avoid the risk of market downturns impacting their nest egg.

Furthermore, after the accumulation phase (the period during which the annuity grows), the accumulated value can be converted into a stream of income through annuitization. This can provide a stable, lifelong income source, ensuring financial security throughout retirement.

Capital Preservation

For conservative investors, capital preservation is paramount. MYGAs excel in this area. The principal invested is protected by the insurance company, and the guaranteed interest rate ensures that the value will not decrease due to market fluctuations. This makes them an attractive alternative to investments that carry higher risk, such as stocks or variable annuities, for a portion of an investor’s portfolio.

Tax Advantages

The tax-deferred growth offered by MYGAs is a significant advantage. This means that any interest earned is not taxed annually. Instead, taxes are deferred until the funds are withdrawn. This allows earnings to compound more effectively over time, potentially leading to a larger accumulation of wealth compared to taxable accounts where interest is taxed each year. When the annuitant begins receiving payouts, the taxation is typically on the earnings portion, and the tax rate may be lower in retirement.

Alternative to Traditional Savings

In times of low interest rates on savings accounts and CDs, MYGAs often present a more competitive option for earning a modest, guaranteed return. While they come with the commitment of a fixed term and potential surrender charges, the enhanced interest rates can make them a compelling choice for short-to-medium term savings goals or for funds that the investor does not anticipate needing access to immediately.

Considerations and Potential Drawbacks

While MYGAs offer attractive benefits, it is essential to be aware of their limitations and potential downsides before making an investment decision.

Liquidity Limitations and Surrender Charges

The most significant consideration for MYGAs is their illiquidity. The guaranteed interest rate is contingent on keeping the funds with the insurance company for the entire duration of the contract. If an annuitant needs to withdraw more than the penalty-free allowance before the guarantee period ends, they will typically be subject to surrender charges. These charges can be substantial, especially in the early years of the contract, and can erode the principal or all of the accumulated interest. Therefore, it is crucial to only invest funds in a MYGA that you are certain you will not need access to during the surrender period.

Inflation Risk

While MYGAs provide a guaranteed nominal return, they do not inherently protect against inflation. If the rate of inflation rises significantly above the guaranteed interest rate, the real return (the return after accounting for inflation) can be diminished, or even negative. This means that the purchasing power of the money may decrease over time. Investors in MYGAs should consider how this might impact their long-term financial goals.

Opportunity Cost

By locking funds into a fixed rate for a set term, investors may miss out on potentially higher returns if market interest rates or investment performance surges during that period. If interest rates rise significantly after an investor has purchased a MYGA, they may be “stuck” with a lower guaranteed rate for the remainder of the term.

Insurance Company Solvency

Although MYGAs are backed by the financial strength of the issuing insurance company, the ultimate guarantee of payments relies on the insurer’s solvency. While insurance companies are generally well-regulated and financially sound, there is always a theoretical risk of default. It is prudent to choose reputable insurance companies with strong financial ratings from independent agencies like A.M. Best, Moody’s, or Standard & Poor’s.

Complexity and Fees

While MYGAs are generally simpler than variable annuities, some products may have riders or optional features that can add complexity and costs. It is essential to understand all fees, charges, and contract terms before signing. The insurance agent or financial advisor should provide clear explanations of these aspects.

Who is a Myga Annuity (MYGA) For?

A MYGA is best suited for a specific type of investor with particular financial goals:

- Conservative Investors: Individuals who prioritize safety of principal and guaranteed returns over potentially higher, but riskier, growth opportunities.

- Retirees or Near-Retirees: Those who need a predictable income stream or want to ensure their retirement savings are not subject to market volatility.

- Individuals Seeking Alternatives to CDs or Savings Accounts: Investors looking for a slightly higher, guaranteed return on their savings, with the added benefit of tax deferral, for funds they don’t need immediate access to.

- Those with a Medium-Term Savings Horizon: Investors who have funds they plan to use in 3-10 years and are comfortable locking them away for that period to secure a guaranteed rate.

- Investors Seeking Tax-Deferred Growth: Individuals who want to maximize their compounding potential by deferring taxes on their investment earnings.

It is crucial to remember that a MYGA is a long-term commitment. It is not an investment for funds that may be needed unexpectedly or for individuals who are comfortable with market risk in exchange for potentially higher returns.

Conclusion: A Reliable Option for Stability

The “Myga Annuity,” most commonly understood as a Multi-Year Guaranteed Annuity (MYGA), represents a valuable financial tool for individuals seeking stability, predictable growth, and capital preservation. In an unpredictable economic landscape, the assurance of a fixed, guaranteed interest rate for a defined period offers a welcome sense of security. While not a one-size-fits-all solution, and with its own set of considerations, particularly regarding liquidity and inflation, a MYGA can be an effective component of a well-diversified financial plan, especially for those nearing or in retirement who prioritize the safety and steady accumulation of their hard-earned savings. As with any financial product, thorough research, careful consideration of individual circumstances, and consultation with a qualified financial advisor are essential steps before investing in a MYGA.