Understanding your mortgage credit score is a pivotal step for any aspiring homeowner. It’s the invisible gatekeeper to securing favorable loan terms and ultimately, your dream home. While the term “mortgage credit score” might sound like a specialized, niche calculation, it’s essentially a reflection of your overall creditworthiness, specifically tailored to the unique demands of mortgage lending. Lenders use this score to assess the risk associated with providing you with a significant amount of capital, and it directly influences the interest rate you’ll pay over the life of your loan. A higher score signifies lower risk, leading to better rates and potentially lower monthly payments. Conversely, a lower score can result in higher interest rates, stricter loan requirements, or even outright denial of a mortgage application.

The Pillars of Your Mortgage Credit Score

Your mortgage credit score isn’t a single, static number pulled from thin air. It’s a dynamic figure derived from an analysis of your credit history, meticulously compiled by the three major credit bureaus: Equifax, Experian, and TransUnion. While these bureaus may have slightly different data sets, the core factors influencing your mortgage credit score remain remarkably consistent. These factors are weighted differently, but each plays a crucial role in painting a comprehensive picture of your financial responsibility.

Payment History: The Foundation of Trust

By far the most significant factor in determining your credit score, payment history accounts for approximately 35% of the FICO Score, a widely used scoring model. This metric scrutinizes whether you’ve paid your bills on time, every time. Late payments, even by a few days, can have a detrimental impact. A single 30-day late payment can significantly lower your score, and the longer the delinquency (60, 90 days, or more), the more severe the damage. Missed payments, defaults, bankruptcies, and foreclosures are particularly damaging and can remain on your credit report for several years, impacting your ability to obtain a mortgage and other forms of credit.

Conversely, a consistent track record of on-time payments demonstrates reliability and reduces the perceived risk for lenders. This includes not just mortgage payments (if you have one currently), but also credit card payments, auto loans, student loans, and any other form of borrowed money.

Amounts Owed: Managing Your Debt Load

The second most influential factor, accounting for about 30% of your FICO Score, is the amount of debt you owe, often referred to as credit utilization. This metric examines how much credit you’re using compared to your total available credit. For credit cards, this is particularly important. Experts generally recommend keeping your credit utilization ratio below 30% for each card and across all your cards. For instance, if you have a credit card with a $10,000 limit and a balance of $5,000, your utilization is 50%. This is considered high and can negatively impact your score.

When it comes to mortgages, the amounts owed also consider the outstanding balances on other loans, such as auto loans and student loans. While having some debt is expected, an excessive amount of outstanding debt can signal to lenders that you might be overextended and at a higher risk of defaulting on a new mortgage. Paying down high balances on credit cards and other revolving credit accounts before applying for a mortgage is a strategic move that can boost your score.

Length of Credit History: The Wisdom of Time

The length of time you’ve been managing credit responsibly contributes about 15% to your FICO Score. Lenders like to see a long history of managing credit, as it provides more data points to assess your behavior. This includes the age of your oldest account, the age of your newest account, and the average age of all your accounts.

It’s important to note that you don’t need a decades-long credit history to get a mortgage. However, if your credit history is relatively short, lenders will place a greater emphasis on other factors. Closing old, unused credit accounts can sometimes be counterproductive, as it can shorten your average account age and potentially increase your credit utilization ratio if you have balances on other cards.

Credit Mix: Diversification and Responsibility

The variety of credit accounts you manage responsibly makes up about 10% of your FICO Score. Lenders like to see that you can handle different types of credit, such as installment loans (like mortgages and auto loans) and revolving credit (like credit cards). Having a mix of these demonstrates your ability to manage various financial obligations. However, this factor is less impactful than payment history or credit utilization. It’s generally not advisable to open new credit accounts solely to improve your credit mix, as this can negatively affect other aspects of your score, such as the length of your credit history and potentially increase your credit utilization if not managed carefully.

New Credit: A Signal of Caution

Opening multiple new credit accounts in a short period can make up the remaining 10% of your FICO Score. When you apply for credit, lenders often perform a “hard inquiry” on your credit report. Too many hard inquiries in a short timeframe can signal to lenders that you might be in financial distress or are taking on a significant amount of new debt, which can be a red flag.

However, it’s important to distinguish between hard and soft inquiries. Soft inquiries, which occur when you check your own credit score or when a potential employer or insurance company reviews your credit report, do not affect your score. When shopping for a mortgage, it’s advisable to do so within a concentrated period (typically 14-45 days, depending on the scoring model) so that multiple mortgage inquiries are treated as a single event by the scoring system, minimizing their impact.

Decoding Mortgage-Specific Credit Scores

While the general principles of credit scoring apply across the board, mortgage lenders often utilize specialized credit scores that are tailored to the mortgage industry. The most common are FICO Score 2, FICO Score 5, and FICO Score 3, which are older versions of the FICO scoring model that are still widely used in mortgage lending. Lenders may also use VantageScore models, though FICO remains dominant in the mortgage space.

These mortgage-specific scores are essentially variations of the standard FICO Score, but they may have slightly different algorithms and weightings to better predict the likelihood of default on a mortgage loan. For example, some mortgage credit scores might place a slightly higher emphasis on your history of paying housing-related debts. It’s also worth noting that lenders often pull your credit report from all three major bureaus and may use the middle score or an average of the scores when making their lending decisions. This means it’s beneficial to have a good credit standing across all three bureaus.

The Impact of Credit Scores on Your Mortgage

Your mortgage credit score is not just a number; it’s a critical determinant of your borrowing power and the cost of your homeownership journey.

Interest Rates: The Most Direct Impact

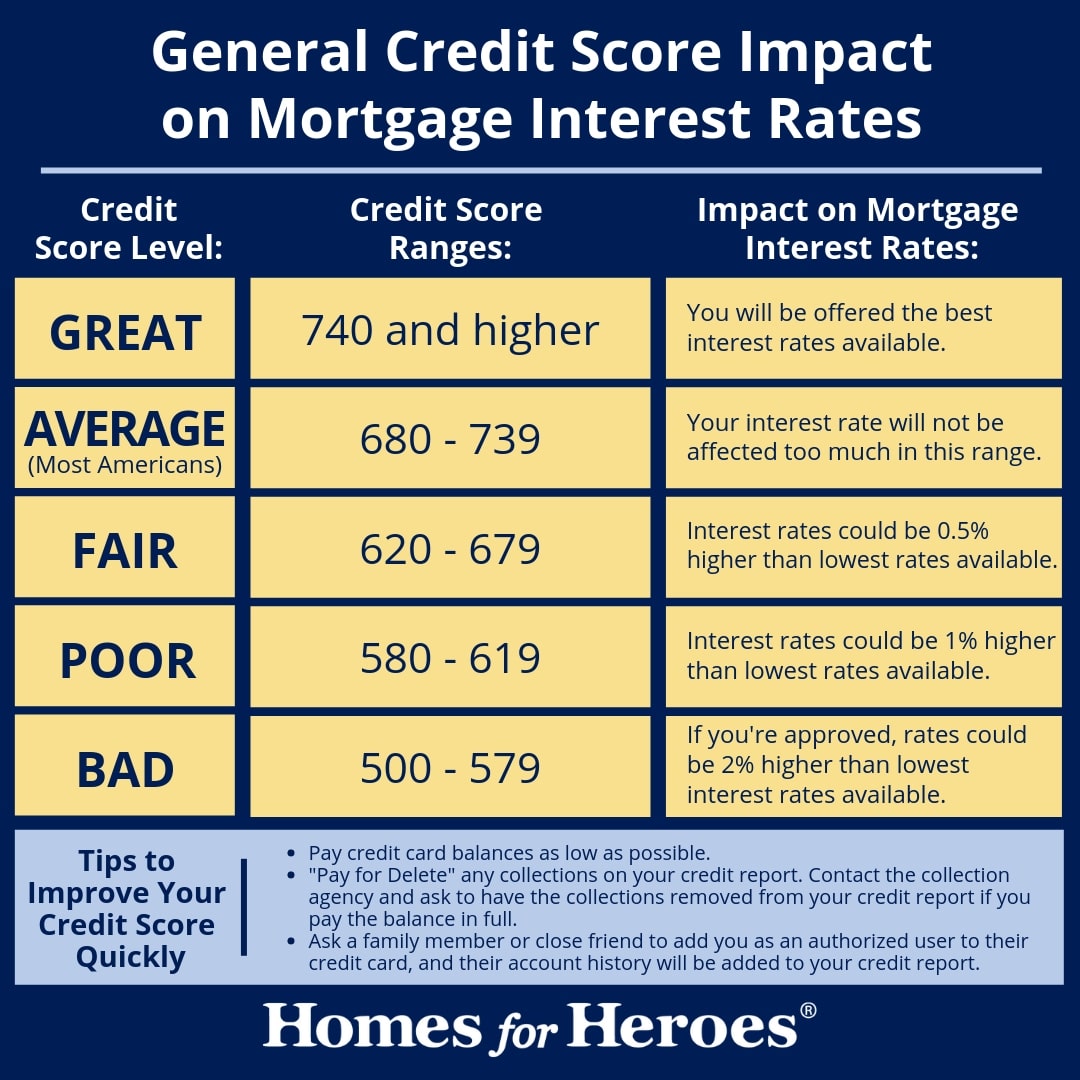

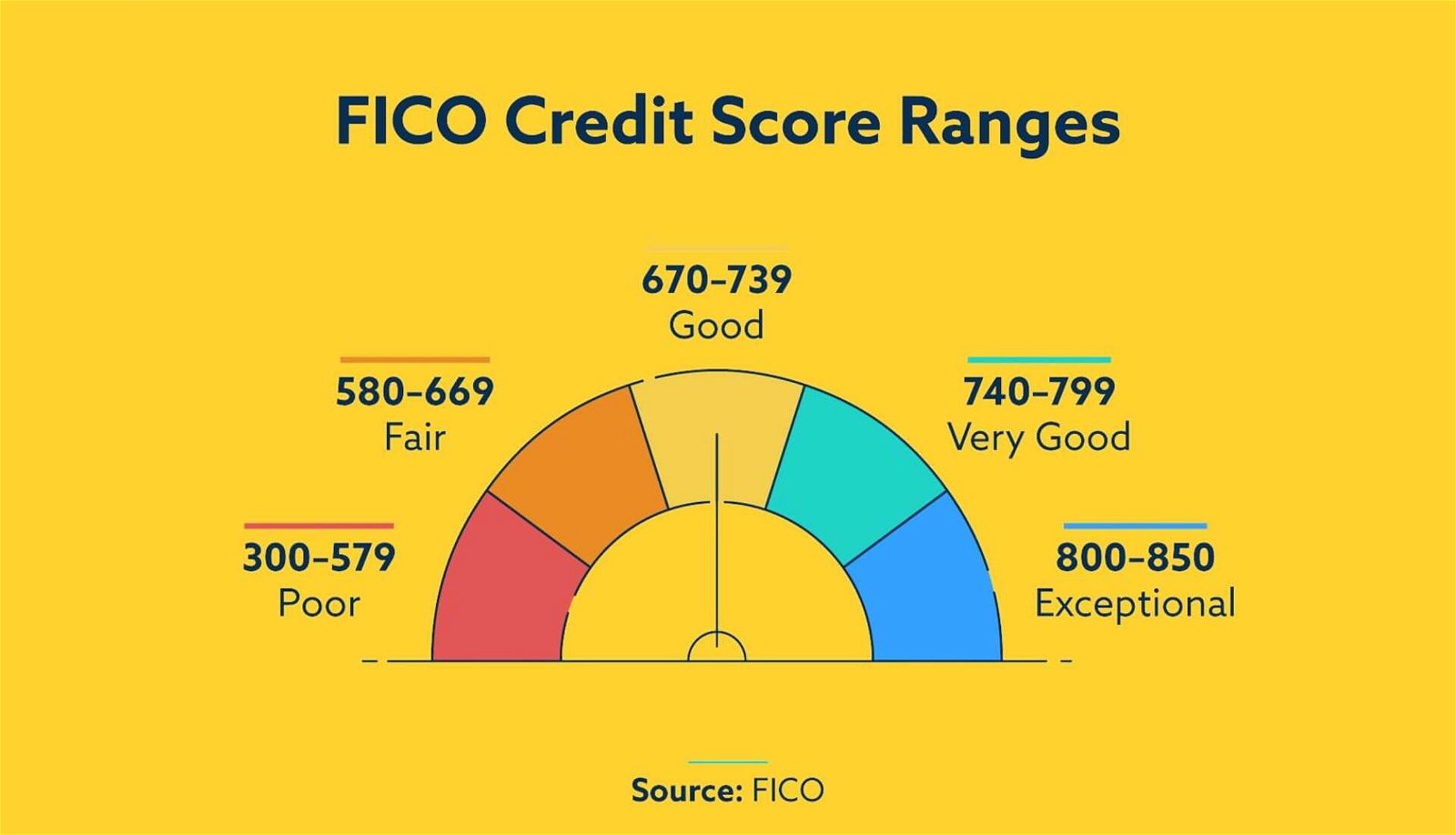

The most immediate and significant impact of your credit score is on the interest rate offered to you. Borrowers with excellent credit scores (typically 740 and above) will qualify for the lowest interest rates. Even a small difference in interest rate can translate into tens of thousands of dollars saved over the 15- to 30-year life of a mortgage. For instance, a 1% difference on a $300,000 loan can mean paying an extra $1,000 per month in interest over 30 years.

Loan Approval and Options

A strong credit score significantly increases your chances of loan approval. Lenders are more willing to approve mortgage applications from borrowers with a proven track record of responsible financial behavior. Furthermore, a good credit score opens the door to a wider range of loan products and programs. You might qualify for conventional loans, FHA loans, VA loans, and other specialized mortgage options that might not be available to borrowers with lower credit scores.

Down Payment Requirements

In some cases, a lower credit score might necessitate a larger down payment. Lenders may require a higher down payment from borrowers deemed to be at a higher risk, as this reduces the lender’s exposure to potential loss. A strong credit score, on the other hand, can sometimes allow for lower down payment options.

Private Mortgage Insurance (PMI)

If your down payment is less than 20% on a conventional loan, you’ll typically be required to pay Private Mortgage Insurance (PMI). The cost of PMI is influenced by your credit score. Borrowers with higher credit scores will generally pay lower PMI premiums, saving you money each month.

How to Check Your Mortgage Credit Score

Knowing your credit score is the first step to improving it. Fortunately, there are several ways to access your credit information.

Free Annual Credit Reports

Under federal law, you are entitled to one free credit report from each of the three major credit bureaus (Equifax, Experian, and TransUnion) every 12 months. You can request these reports from AnnualCreditReport.com. While these reports detail your credit history, they do not typically include your FICO Score.

Credit Monitoring Services and Apps

Many financial institutions, credit card companies, and dedicated credit monitoring services offer free access to your credit score, often updated monthly. These services are invaluable for tracking your progress and understanding how specific financial actions might impact your score. Some popular options include Credit Karma, Experian Boost, and services offered directly by your bank or credit card issuer. While these often provide VantageScore or a specific FICO Score version, it’s important to remember that your mortgage lender might use a slightly different, industry-specific score. However, these readily available scores offer a strong general indication of your credit health.

Purchasing Your FICO Score

If you want to see the specific FICO Score that mortgage lenders are likely to use, you can often purchase these scores directly from myFICO.com. This provides a more precise insight into your standing within the mortgage lending landscape.

Strategies to Improve Your Mortgage Credit Score

Improving your mortgage credit score is an achievable goal with consistent effort and strategic financial management.

Consistently Pay Bills on Time

As mentioned, this is the most critical factor. Set up automatic payments or calendar reminders to ensure you never miss a due date. If you have a past-due account, address it immediately.

Reduce Credit Utilization

Focus on paying down balances on your credit cards. Aim to keep your utilization ratio below 30% for each card and overall. Prioritize paying down high-balance cards first.

Avoid Opening New Credit Unnecessarily

Resist the urge to open new credit accounts unless absolutely necessary. If you do need to open a new account, do so strategically and avoid opening multiple accounts in a short period before applying for a mortgage.

Address Errors on Your Credit Report

Review your credit reports carefully for any inaccuracies. If you find any errors, dispute them with the credit bureau immediately. Errors can unfairly lower your score.

Maintain Older Accounts

Avoid closing older credit accounts, especially if they have a zero balance. This can help maintain a longer credit history and potentially lower your overall credit utilization.

By understanding the components of your mortgage credit score and actively managing your credit, you can significantly improve your chances of securing favorable mortgage terms and make your journey to homeownership a smoother and more affordable one.