In the intricate world of real estate finance, understanding key terminology is paramount for any aspiring homeowner or investor. Among the crucial concepts that frequently arise is the Loan-to-Value (LVR) ratio. While the title “What is an LVR Home Loan?” might initially suggest a specific type of loan product, it’s more accurate to view LVR as a fundamental metric that underpins a vast majority of home loan approvals and terms. LVR is not a standalone loan product but rather a ratio used by lenders to assess risk and determine lending criteria. This article will delve into the intricacies of LVR, explaining its calculation, its significant impact on mortgage rates and loan options, and how borrowers can strategically navigate its implications.

Understanding the Loan-to-Value (LVR) Ratio

At its core, the Loan-to-Value ratio is a simple yet powerful financial calculation that lenders use to gauge the risk associated with a mortgage. It directly compares the amount of money you are borrowing for a property against the property’s appraised value.

The Formula and Calculation

The calculation of LVR is straightforward:

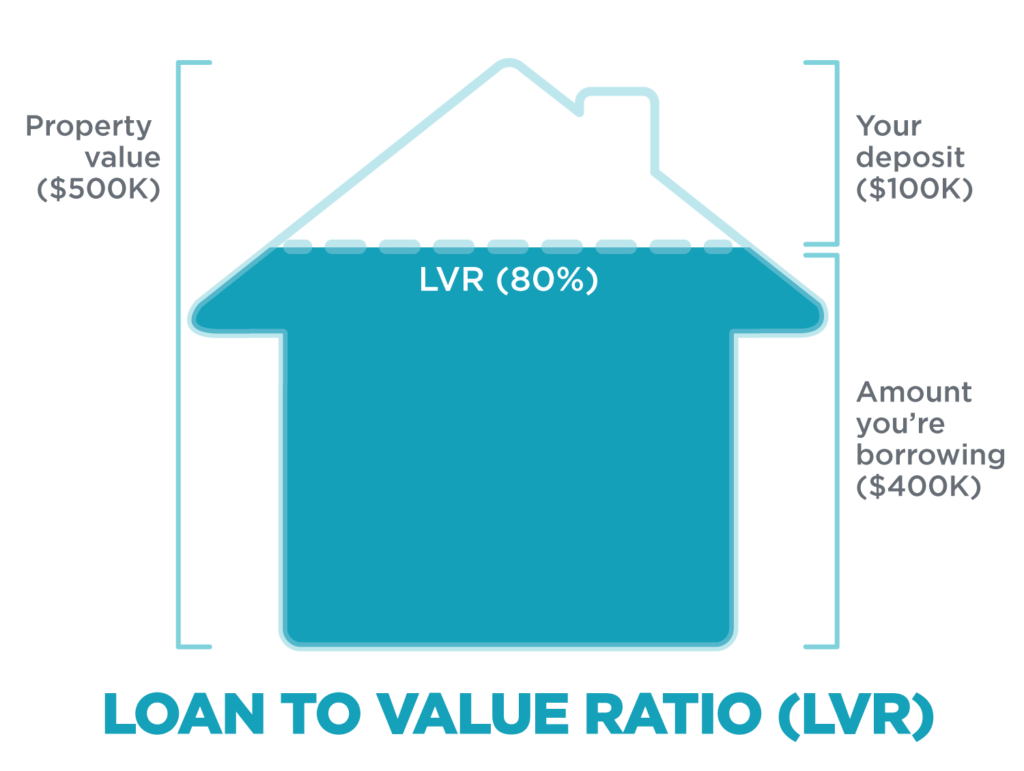

LVR = (Loan Amount / Property Value) * 100

- Loan Amount: This is the total sum of money you are requesting from the lender to purchase the property.

- Property Value: This is typically determined by a professional appraisal conducted by the lender. The appraisal assesses the property’s fair market value, taking into account factors such as its size, condition, location, recent sales of comparable properties, and current market trends. In some instances, especially with high-value properties or unique circumstances, multiple appraisals might be obtained. It’s important to note that the purchase price you agree to with the seller is not always the value the lender will use; the appraised value is the deciding figure for LVR calculation.

Example:

If you are looking to purchase a home for $500,000 and you are making a down payment of $100,000, your loan amount will be $400,000 ($500,000 – $100,000).

Using the formula:

LVR = ($400,000 / $500,000) * 100 = 80%

This means that the loan represents 80% of the property’s value.

The Significance of the Appraised Value

The appraised value is a critical component of the LVR calculation. Lenders rely on appraisals to ensure they are not lending more than the property is worth. If the purchase price is higher than the appraised value, the lender will typically use the appraised value for the LVR calculation, meaning the borrower may need to increase their down payment to meet the lender’s LVR requirements. Conversely, if the appraised value is higher than the purchase price, the lender will usually use the purchase price for the LVR calculation. This is to protect the lender from overvaluing an asset.

Understanding Different LVR Tiers

LVR ratios are often categorized into different tiers, each carrying distinct implications for borrowers:

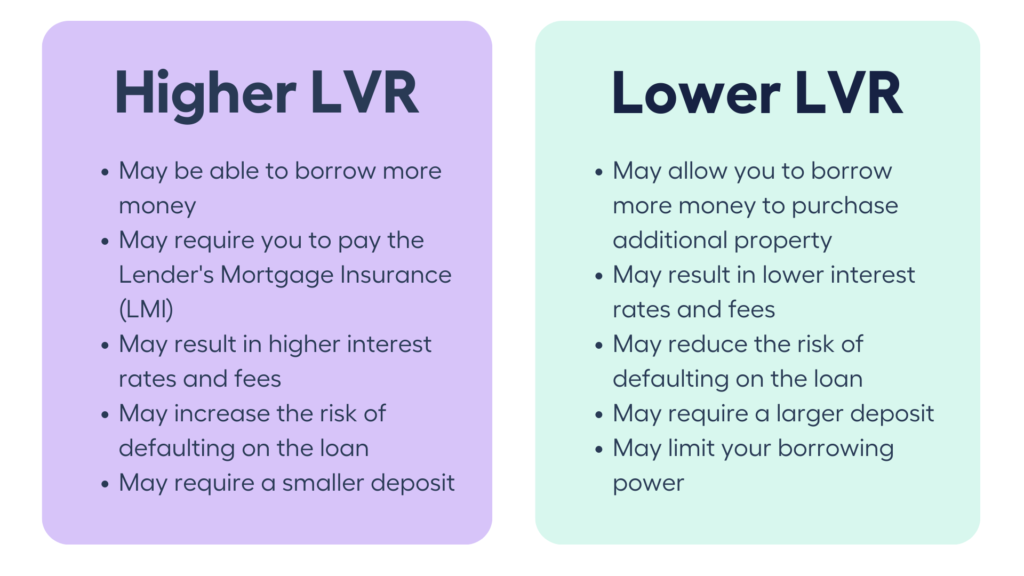

- Low LVR (e.g., below 80%): This signifies a lower risk for the lender. Borrowers with a low LVR typically benefit from more favorable loan terms, including lower interest rates and potentially a wider range of loan products. A lower LVR indicates a substantial equity stake for the borrower from the outset.

- High LVR (e.g., above 80%): This indicates a higher risk for the lender. Borrowers with a high LVR have a smaller equity stake in the property, meaning they are borrowing a larger portion of its value. This often translates to higher interest rates, stricter lending criteria, and potentially the requirement of Private Mortgage Insurance (PMI) or similar insurance policies.

The Impact of LVR on Home Loans

The LVR ratio is not merely a statistical figure; it is a primary determinant of your loan’s cost, accessibility, and the options available to you.

Interest Rates and Mortgage Premiums

One of the most direct impacts of LVR is on your mortgage interest rate. Lenders view higher LVRs as indicative of increased risk because if a borrower defaults, the lender has a smaller buffer (equity) to recover their losses from selling the property. To compensate for this elevated risk, lenders typically charge higher interest rates to borrowers with higher LVRs.

Conversely, a lower LVR demonstrates a greater financial commitment from the borrower and less risk for the lender, often resulting in access to lower interest rates. This can lead to significant savings over the life of the loan, especially on large mortgage amounts.

Private Mortgage Insurance (PMI)

For loans with an LVR above 80% (or 78% in some cases), lenders often require borrowers to take out Private Mortgage Insurance (PMI). PMI protects the lender, not the borrower, in the event of a default. The cost of PMI is typically paid by the borrower, either as a lump sum or, more commonly, as a monthly premium added to the mortgage payment. This additional cost further increases the overall expense of owning a home when your down payment is low. Once the LVR falls below a certain threshold (usually 80%, and eventually 78% with automatic termination rules), PMI can often be removed, reducing your monthly housing costs.

Loan Approval and Eligibility

Your LVR can significantly influence your eligibility for a mortgage in the first place. Some lenders have stricter LVR thresholds for certain loan products or for borrowers with less-than-perfect credit scores. A high LVR, combined with other risk factors, might lead to loan denial or require you to explore alternative lending options, which could come with higher costs.

Access to Different Loan Products

The LVR also dictates the types of mortgage products you can access. For instance, certain government-backed loan programs or specialized mortgages designed for first-time homebuyers might have specific LVR requirements or offer more flexible terms for those with lower down payments. Conversely, if you have a substantial down payment and a low LVR, you might qualify for premium mortgage products with more competitive rates and features.

Strategies for Managing LVR

Understanding LVR empowers borrowers to make informed decisions and adopt strategies that can lead to more favorable loan terms and reduced borrowing costs.

Maximizing Your Down Payment

The most direct way to lower your LVR is to increase your down payment. A larger down payment directly reduces the loan amount relative to the property’s value. Even a few extra percentage points on your down payment can make a significant difference in your LVR, potentially moving you from an 85% LVR to an 80% LVR, which can unlock lower interest rates and avoid PMI. This might involve saving for longer, utilizing down payment assistance programs, or exploring options like gifted funds from family members.

Understanding Property Valuation Nuances

While the appraisal is the lender’s primary tool, understanding its nuances can be beneficial. If you believe a property has been undervalued by the appraiser, you may have grounds to request a reconsideration or a second appraisal. However, this is typically only successful if there is clear evidence of an error or overlooked comparable sales. Be aware that lenders generally have the final say on the appraised value they will accept.

Exploring Loan Options with Different Lenders

Different lenders may have varying risk appetites and different calculations for LVR. Shopping around and comparing offers from multiple financial institutions is crucial. One lender might have a slightly more favorable LVR policy or a different approach to assessing borrower risk, potentially leading to a better outcome for you. Mortgage brokers can be particularly helpful in this regard, as they have access to a wide network of lenders and can help you find the best-suited loan for your situation.

Considering Different Property Types

The type of property you intend to purchase can also influence LVR requirements. For example, some lenders might have stricter LVR limits for investment properties compared to primary residences, due to the perceived higher risk of rental income fluctuations. Similarly, properties with unique characteristics or in less conventional locations might face more scrutiny.

Conclusion: LVR as a Cornerstone of Mortgage Lending

In essence, an “LVR home loan” isn’t a distinct product but rather a loan structured around a specific Loan-to-Value ratio. This ratio is a fundamental pillar of mortgage lending, serving as a critical risk assessment tool for lenders and a significant factor influencing borrowing costs and accessibility for consumers. By thoroughly understanding how LVR is calculated, its profound impact on interest rates, insurance requirements, and loan eligibility, and by proactively employing strategies to manage it, borrowers can navigate the mortgage landscape with greater confidence and secure more advantageous home financing. A well-understood LVR is a powerful ally in the journey toward homeownership.