Incremental budgeting, a widely adopted financial planning methodology, represents a practical and often straightforward approach to allocating resources for the upcoming fiscal period. At its core, it’s a process where the budget of the previous period serves as the baseline, and adjustments are made incrementally to account for anticipated changes. This method is characterized by its reliance on historical data, making it a familiar and relatively easy process for many organizations to implement. However, like any budgeting technique, it comes with its own set of advantages and disadvantages, influencing its suitability for different organizational contexts and objectives. Understanding the nuances of incremental budgeting is crucial for effective financial management and strategic planning.

The Mechanics of Incremental Budgeting

Incremental budgeting operates on a simple premise: what was spent last year, with minor modifications, will be spent next year. This “from-the-ground-up” or “top-down” approach, depending on the specific implementation, involves taking the previous period’s budget figures and applying a percentage increase or decrease. These adjustments are typically driven by expected inflation, anticipated changes in costs, planned increases in operational capacity, or foreseen reductions in demand.

Establishing the Baseline: The Prior Period’s Budget

The foundational element of incremental budgeting is the prior period’s financial performance and established budget. This historical data provides a concrete starting point, avoiding the need to justify every single expenditure from scratch. For instance, if a department spent $100,000 on salaries in the previous year, and the organization anticipates a 3% cost-of-living increase, the new salary budget would start at $103,000 before any other considerations. This continuity simplifies the process, especially in organizations with stable operations and predictable expenditure patterns.

Calculating Incremental Adjustments

The core of the incremental process lies in calculating the adjustments to this baseline. These adjustments are often expressed as a percentage or a fixed amount. Common drivers for these increments include:

- Inflation: A general increase in prices necessitates a corresponding increase in budget to maintain purchasing power. This is often calculated based on an external economic index.

- Volume Changes: If an organization anticipates an increase in production, sales, or service delivery, its budget will need to accommodate the associated rise in material, labor, or operational costs. Conversely, a projected decrease in volume would lead to a budget reduction.

- New Initiatives or Projects: While incremental budgeting primarily focuses on existing operations, provisions may be made for new, approved projects or initiatives. These are usually added as separate line items or as specific increases to relevant departmental budgets.

- Cost-Saving Measures: In some instances, budget adjustments might reflect anticipated savings from efficiency improvements or cost-reduction programs. This could lead to a negative increment.

- Policy Changes: Shifts in organizational policy, such as changes in compensation structures or investment strategies, can also necessitate budget adjustments.

Approval and Implementation

Once the incremental adjustments are calculated and documented, the proposed budget is typically submitted to higher management or a finance committee for review and approval. This stage often involves discussions and potential revisions, but the fundamental structure derived from the previous budget remains largely intact. Upon approval, the new budget is implemented for the upcoming fiscal period.

Advantages of Incremental Budgeting

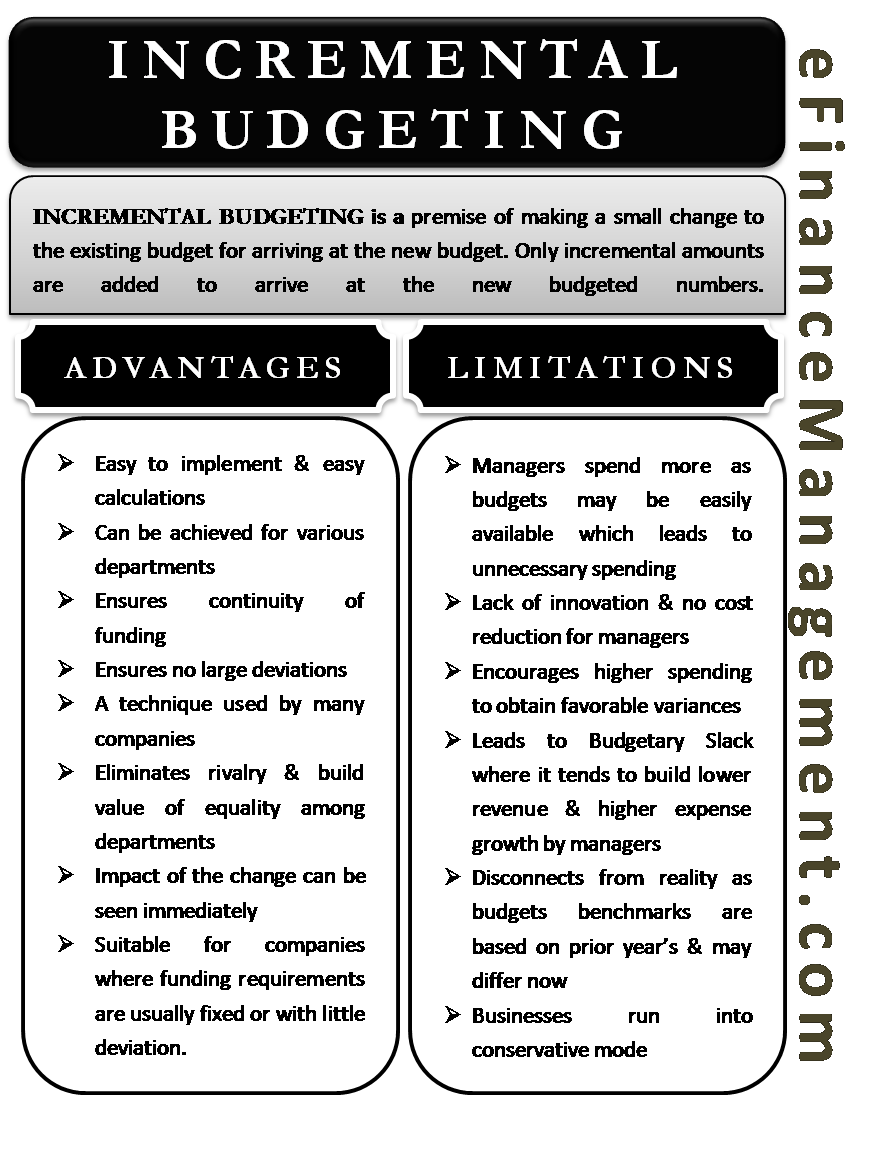

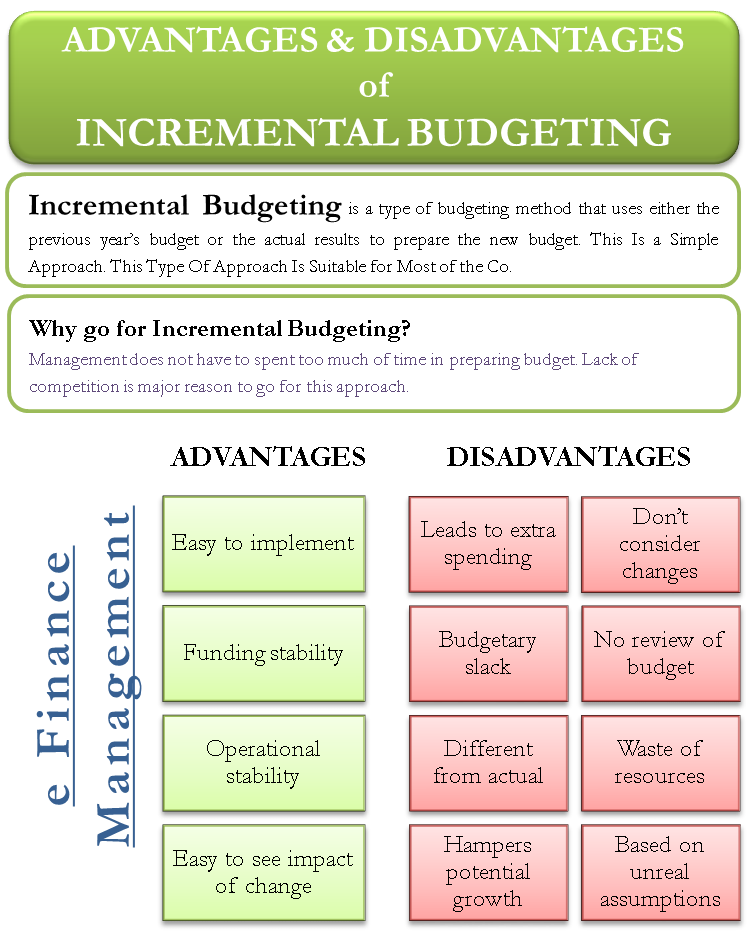

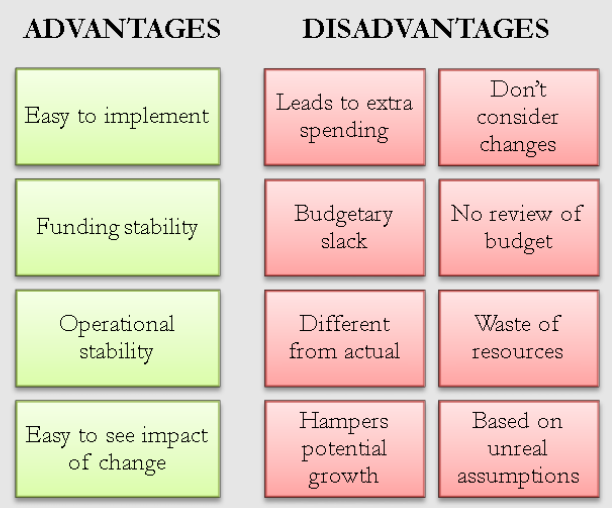

The enduring popularity of incremental budgeting stems from several key advantages that make it an attractive option for many organizations. Its simplicity and reliance on historical data contribute to its ease of use and efficiency.

Simplicity and Ease of Use

Perhaps the most significant advantage of incremental budgeting is its inherent simplicity. The process of adjusting a previous budget is far less complex and time-consuming than developing an entirely new budget from scratch each year. This makes it accessible to organizations with limited financial expertise or resources. For managers who are not finance professionals, understanding and contributing to an incremental budget is generally more straightforward.

Stability and Predictability

Incremental budgeting fosters stability and predictability in financial planning. By using historical data as a foundation, it provides a clear expectation of resource allocation. This can be particularly beneficial for departments or projects that have consistent operational needs. Managers can rely on a familiar baseline, reducing uncertainty and allowing for more focused planning of operational activities.

Reduced Time and Cost

The streamlined nature of incremental budgeting translates into significant savings in terms of time and cost. Developing a zero-based budget, for instance, requires extensive analysis and justification for every line item, which can be a resource-intensive undertaking. Incremental budgeting, by contrast, bypasses much of this exhaustive review, making the budgeting cycle shorter and less expensive.

Managerial Acceptance

Managers often find incremental budgeting more palatable than other methods. They are familiar with the existing expenditure patterns and are comfortable defending incremental changes to their budgets. The process doesn’t challenge their existing operational frameworks as drastically as some alternative methods, leading to less resistance.

Disadvantages of Incremental Budgeting

Despite its advantages, incremental budgeting is not without its drawbacks. Its reliance on historical data and its tendency to perpetuate past spending patterns can lead to inefficiencies and hinder strategic growth.

Perpetuation of Inefficiencies

A primary criticism of incremental budgeting is its tendency to carry forward any inefficiencies or outdated practices from previous budgets. If a particular expenditure was excessive or unnecessary in the past, incremental budgeting will likely continue to fund it, albeit with minor adjustments. It does not inherently question whether the current level of spending is optimal or justified in the current environment.

Lack of Strategic Alignment

Incremental budgeting can sometimes lead to a disconnect between departmental budgets and the overall strategic objectives of the organization. Because it focuses on incremental changes to existing line items, it may not adequately support new strategic initiatives or reallocate resources from less critical areas to those that are gaining strategic importance. This can result in a budget that is operationally sound but strategically misaligned.

Resistance to Change and Innovation

The “what we did last year, plus a bit more” mentality can stifle innovation and discourage a critical review of operational methods. Departments may become accustomed to their allocated budgets and resist exploring more efficient or innovative ways of operating if it means fundamentally challenging their historical spending.

Inflexibility in Dynamic Environments

In rapidly changing markets or industries, incremental budgeting can prove to be too rigid. If a business experiences sudden shifts in demand, technology, or competitive landscape, an incremental budget based on past performance may not provide the necessary flexibility to adapt quickly. Significant, unforeseen changes may require budget revisions that are disruptive to the incremental process.

Potential for Budgetary Slack

Managers may consciously or unconsciously build “slack” into their budgets by overestimating needs, knowing that their requests will likely be adjusted downwards. This can lead to the accumulation of unspent funds or inefficient resource utilization, as there is less incentive to operate leanly if excess funds are expected to be rolled over or maintained.

When is Incremental Budgeting Most Effective?

Incremental budgeting is most effective in specific organizational contexts and under certain conditions. Its strengths are best leveraged when the operating environment is relatively stable and predictability is a key concern.

Stable Operating Environments

Organizations operating in mature industries with predictable revenue streams and stable cost structures often find incremental budgeting to be a highly effective tool. For example, government agencies with well-defined mandates or established manufacturing firms with long-term contracts may benefit from the continuity and predictability it offers.

Small to Medium-Sized Enterprises (SMEs)

SMEs, particularly those with limited financial resources or less complex operations, can benefit from the simplicity and lower implementation cost of incremental budgeting. It allows them to engage in financial planning without requiring specialized expertise or extensive analytical resources.

Departments with Consistent Needs

For departments whose operational needs remain largely unchanged from year to year, incremental budgeting can be a perfectly adequate approach. This might include administrative functions or maintenance departments where the core activities and resource requirements are consistent.

When Efficiency is Not the Primary Driver

In situations where the primary focus is on maintaining existing service levels or operational continuity, and radical efficiency improvements are not an immediate priority, incremental budgeting can suffice. It ensures that essential functions are funded without the disruption of a complete budget overhaul.

Alternatives to Incremental Budgeting

While incremental budgeting has its place, organizations seeking greater efficiency, strategic alignment, or a more critical review of expenditures often consider alternative budgeting methods.

Zero-Based Budgeting (ZBB)

In contrast to incremental budgeting, ZBB requires every line item in the budget to be justified from scratch, regardless of whether it was funded in the previous period. This method forces a thorough review of all expenses, encouraging cost-saving and the reallocation of resources to areas of higher priority. While more time-consuming, ZBB can lead to significant cost reductions and improved strategic alignment.

Activity-Based Budgeting (ABB)

ABB links budget allocations to specific activities performed by an organization. It identifies the costs associated with each activity and then sums these costs to arrive at the total budget. This approach provides a clearer understanding of cost drivers and can help identify areas where process improvements can lead to cost savings.

Performance-Based Budgeting (PBB)

PBB, also known as outcome-based budgeting, focuses on linking budget allocations to the achievement of specific performance targets or outcomes. Departments must demonstrate how their proposed expenditures will contribute to the organization’s strategic goals and measurable results. This method fosters accountability and a focus on results.

Rolling Budgets

Rolling budgets, or continuous budgets, are updated on a regular basis, typically monthly or quarterly, to reflect the latest information and projections. This dynamic approach allows for greater flexibility and responsiveness to changing conditions, unlike static annual budgets that may become outdated quickly.

Conclusion

Incremental budgeting, with its reliance on historical data and its focus on minor adjustments, offers a straightforward and familiar path to financial planning. It provides stability, predictability, and is relatively easy to implement, making it a practical choice for many organizations, particularly those operating in stable environments or with consistent needs. However, its inherent limitations, such as the perpetuation of inefficiencies and potential misalignment with strategic goals, necessitate careful consideration. Organizations that prioritize cost optimization, strategic agility, and a rigorous review of expenditures may find greater value in alternative budgeting methods. The choice of budgeting technique ultimately depends on an organization’s specific circumstances, strategic objectives, and the dynamics of its operating environment.