The world of finance, particularly investment, is rife with acronyms and specialized terminology. For those venturing into this domain, understanding these terms is crucial for informed decision-making. Among these, the term “LP” frequently surfaces, especially within the context of private equity, venture capital, and hedge funds. But what exactly is an LP in investment? In essence, an LP refers to a Limited Partner. This designation is fundamental to the structure and operation of many investment vehicles, dictating roles, responsibilities, and risk profiles for those involved.

Understanding the Limited Partner (LP) Role

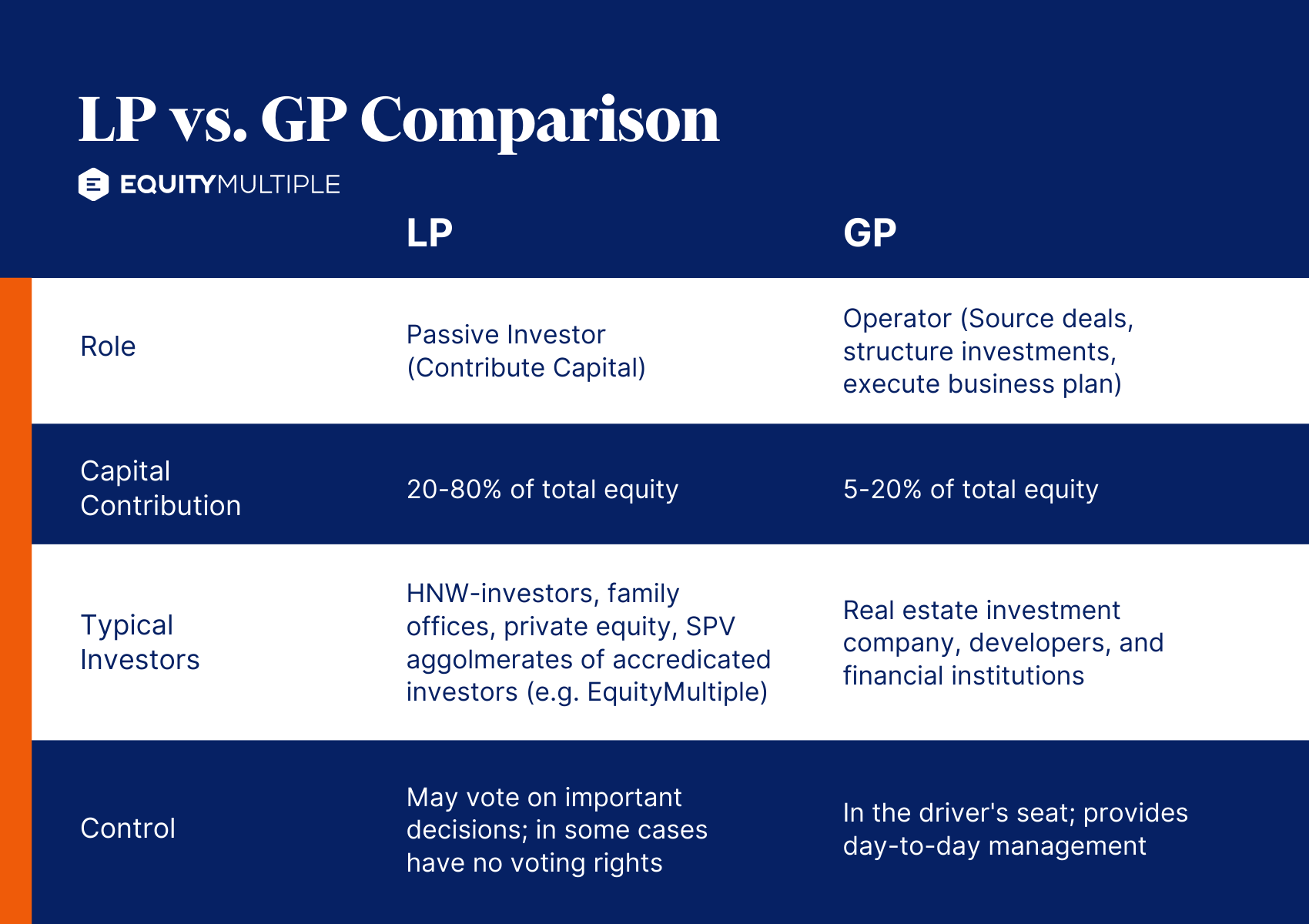

A Limited Partner is an individual or entity that invests capital into a fund managed by a General Partner (GP). Unlike the GP, the LP’s involvement in the day-to-day operations and strategic decision-making of the fund is intentionally limited. Their primary contribution is financial, providing the capital that the GP then deploys into various investments. This passive role is a defining characteristic, offering a distinct advantage to LPs seeking exposure to alternative asset classes without the burden of active management.

The Nature of LP Investment

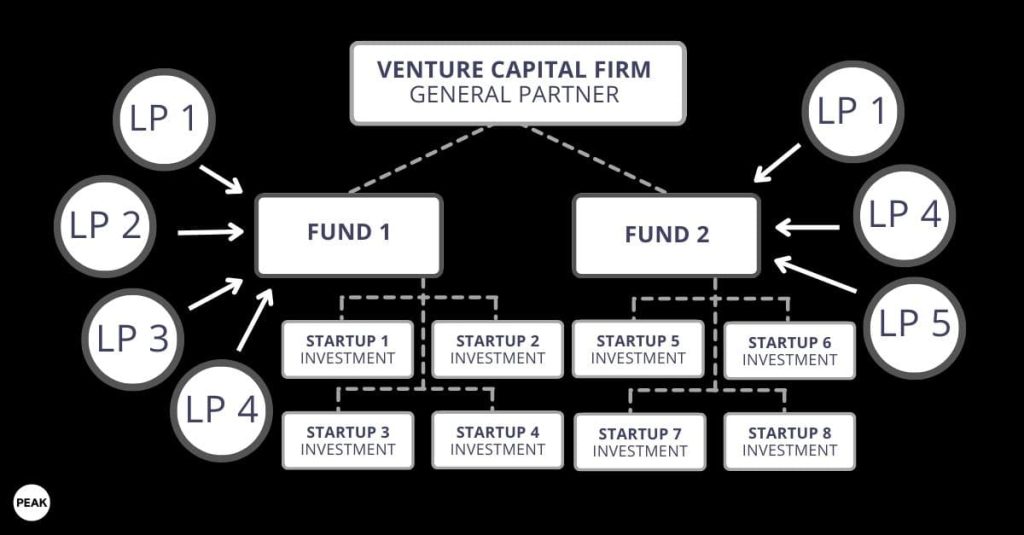

LPs typically invest in pooled investment vehicles such as private equity funds, venture capital funds, real estate funds, and hedge funds. These funds are structured as limited partnerships, where the GP acts as the general partner and the investors are the limited partners. The agreement between the GP and the LPs, known as the Limited Partnership Agreement (LPA), meticulously outlines the terms of the partnership, including investment strategies, fee structures, distribution waterfalls, and the rights and obligations of each party.

Capital Commitments and Drawdowns

One of the key mechanisms through which LPs contribute capital is via capital commitments. When an LP agrees to invest in a fund, they commit a certain amount of capital. This commitment is not disbursed all at once. Instead, the GP “calls” or “draws down” this committed capital over time as investment opportunities arise. This drawdown process allows the GP to manage cash flow and ensures that LPs only deploy their capital when it is needed for specific investments. The LPA specifies the notice period required for drawdowns and the maximum duration over which capital commitments can be called.

Investment Horizon and Liquidity

Investments in funds where LPs are involved are often characterized by long investment horizons. Private equity and venture capital, for instance, typically involve investments in companies that are not publicly traded and require several years for their value to mature and be realized. Consequently, LP investments are generally illiquid. This means that once capital is committed and invested, it is difficult, if not impossible, to redeem or withdraw it before the fund’s term concludes, which can be 10 years or more. LPs must therefore be prepared to tie up their capital for extended periods.

Who are Limited Partners?

The profile of a Limited Partner can be diverse, encompassing a wide range of sophisticated investors. These are generally individuals or institutions with substantial financial resources and a high tolerance for risk, given the illiquid and long-term nature of these investments.

Institutional Investors

A significant portion of LP capital comes from institutional investors. These include:

- Pension Funds: Both public and private pension funds seek long-term, diversified returns to meet their retirement obligations. Alternative investments, like those managed by GPs, often form a part of their strategic asset allocation.

- Endowments: University endowments, foundations, and charitable trusts invest for perpetual growth, aiming to generate income to support their respective missions.

- Sovereign Wealth Funds: Government-owned investment funds, often managing a nation’s surplus revenues, are major players in global private markets.

- Insurance Companies: These companies invest premiums to cover future claims and often seek yield-enhancing investments with longer durations.

- Fund of Funds: These are specialized investment funds that themselves invest in other funds. They act as LPs in multiple underlying funds, offering diversification and professional selection expertise to their own investors.

High-Net-Worth Individuals (HNWIs) and Family Offices

While institutional investors dominate the LP landscape, sophisticated individual investors and their associated family offices also participate. These investors typically have extensive wealth and a deep understanding of complex financial instruments. They may invest directly in funds or through specialized wealth management structures.

The General Partner (GP) vs. Limited Partner (LP) Distinction

The relationship between the GP and the LP is symbiotic, yet distinctly delineated. Understanding this dichotomy is crucial to grasping the mechanics of pooled investment vehicles.

General Partner (GP): The Active Manager

The General Partner is the entity or individual responsible for the management and operation of the investment fund. Their responsibilities are extensive and include:

- Fundraising: Identifying and securing capital commitments from LPs.

- Investment Sourcing and Due Diligence: Finding promising investment opportunities, conducting thorough research, and performing due diligence.

- Portfolio Management: Making investment decisions, structuring deals, and actively managing the portfolio companies or assets.

- Operational Management: Handling the legal, administrative, and financial operations of the fund.

- Exits: Strategizing and executing the sale or IPO of portfolio investments to realize returns.

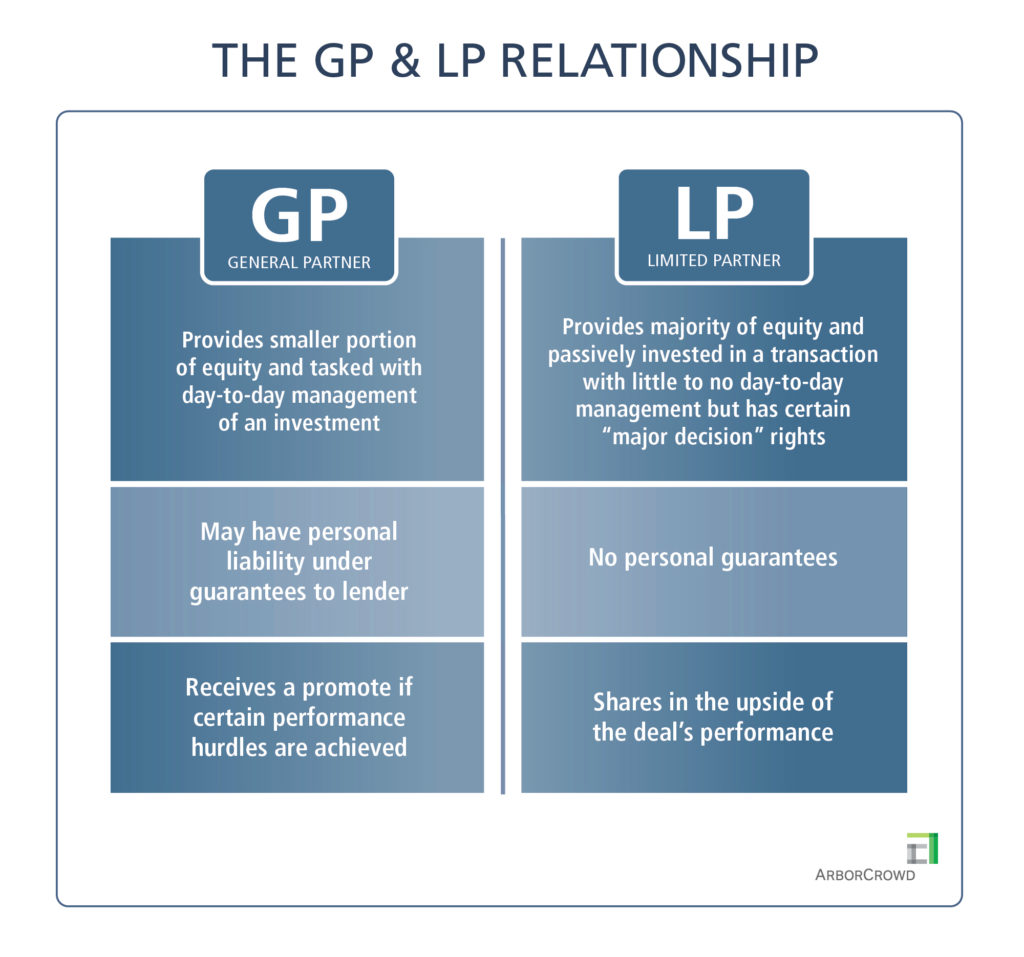

The GP assumes unlimited liability for the fund’s debts and obligations, a stark contrast to the LPs’ limited liability. This significant risk undertaken by the GP is compensated through management fees and carried interest (a share of the profits).

Limited Partner (LP): The Passive Investor

In contrast, the Limited Partner’s role is largely passive. Their primary contribution is capital, and their liability is limited to the amount of their investment. They do not participate in the day-to-day management of the fund or its underlying investments. However, LPs do have certain rights, which are typically outlined in the LPA, such as:

- Receiving information: Regular reports on fund performance, portfolio updates, and financial statements.

- Voting on specific matters: In some cases, LPs may have the right to vote on significant changes to the fund’s strategy or management.

- Access to auditors: The ability to review the fund’s financial records.

This division of labor allows GPs to specialize in investment management, while LPs can gain exposure to potentially high-return, albeit illiquid, asset classes without needing the expertise or time commitment required for active management.

The Structure of a Limited Partnership

The legal framework of a limited partnership is the bedrock upon which the LP-GP relationship is built. This structure offers distinct advantages for both parties, facilitating the pooling of capital for investment purposes.

The Limited Partnership Agreement (LPA)

The LPA is the cornerstone document of any limited partnership. It is a legally binding contract that governs the relationship between the GP and the LPs. Key provisions within the LPA include:

- Investment Objective and Strategy: Defines the types of investments the fund will pursue, geographical focus, and industry sectors.

- Fund Term: Specifies the lifespan of the fund, typically 10-12 years, with potential for extensions.

- Capital Commitments and Drawdowns: Details the total capital committed by LPs and the process by which the GP will call these funds.

- Management Fees: The annual fee charged by the GP, usually a percentage of committed capital or invested capital.

- Carried Interest (Carry): The GP’s share of the fund’s profits, typically 20%, realized after LPs have received their initial investment back and a preferred return (hurdle rate).

- Distribution Waterfall: Outlines the order in which profits are distributed between LPs and the GP.

- Governance and Reporting: Defines the rights of LPs to information and any voting powers they may possess.

- Key Person Clause: Provisions related to the departure or incapacitation of key individuals within the GP.

The LPA is a complex document negotiated between sophisticated parties, and its terms are crucial for aligning the interests of the GP and LPs.

Alignment of Interests

A well-structured LPA aims to align the interests of the GP and LPs. The GP’s compensation is heavily tied to the fund’s performance, particularly through carried interest. This incentive structure encourages GPs to make sound investment decisions that maximize returns for all partners. LPs, in turn, benefit from the GP’s expertise and diligent management, aiming for significant capital appreciation over the long term.

The Importance of LPs in the Investment Ecosystem

Limited Partners are not merely passive capital providers; they are indispensable components of the modern investment landscape, particularly in alternative asset classes. Their capital fuels innovation, growth, and economic development across various sectors.

Driving Private Equity and Venture Capital

Without the substantial capital provided by LPs, the private equity and venture capital industries, which are critical for funding startups and mature companies undergoing transformation, would not exist in their current form. LPs provide the fuel for GPs to invest in companies that may not be suitable for public markets or require patient capital for growth and restructuring. This funding can lead to job creation, technological advancements, and overall economic expansion.

Access to Specialized Expertise

LPs often choose to invest with GPs because of their specialized knowledge and established networks within specific industries or investment strategies. While LPs may have substantial capital, they may lack the focused expertise, deal flow, and operational experience that a dedicated GP possesses. This delegation of management allows LPs to diversify their portfolios into areas they might otherwise find inaccessible or too complex to manage directly.

Contribution to Market Liquidity and Efficiency

The capital provided by LPs, though deployed over long periods, eventually flows back into the broader economy upon the successful exit of investments. This can manifest as acquisitions by larger corporations, initial public offerings (IPOs), or distributions to other investors. This cycle of investment and divestment contributes to market liquidity and can enhance the efficiency of capital allocation across the economy.

In conclusion, understanding the role of the Limited Partner (LP) is fundamental to navigating the complexities of private investment markets. LPs are the capital providers, entrusting their funds to General Partners who manage and deploy these resources with the goal of generating attractive returns. Their passive, yet vital, participation underpins a significant portion of the global investment ecosystem, driving growth and innovation across a myriad of industries.