In the rapidly evolving landscape of Tech & Innovation—where drone startups, AI researchers, and remote sensing pioneers operate on the cutting edge—financial agility is as critical as technical prowess. For entrepreneurs and engineers developing autonomous flight systems or high-resolution mapping payloads, understanding the nuances of capital liquidity is essential. One of the most misunderstood and potentially costly aspects of corporate and personal finance in this sector is the credit card cash advance fee. While often viewed as a simple convenience, for a tech-driven enterprise, it represents a high-stakes financial maneuver that can significantly impact the “burn rate” and the overall health of an innovation-focused project.

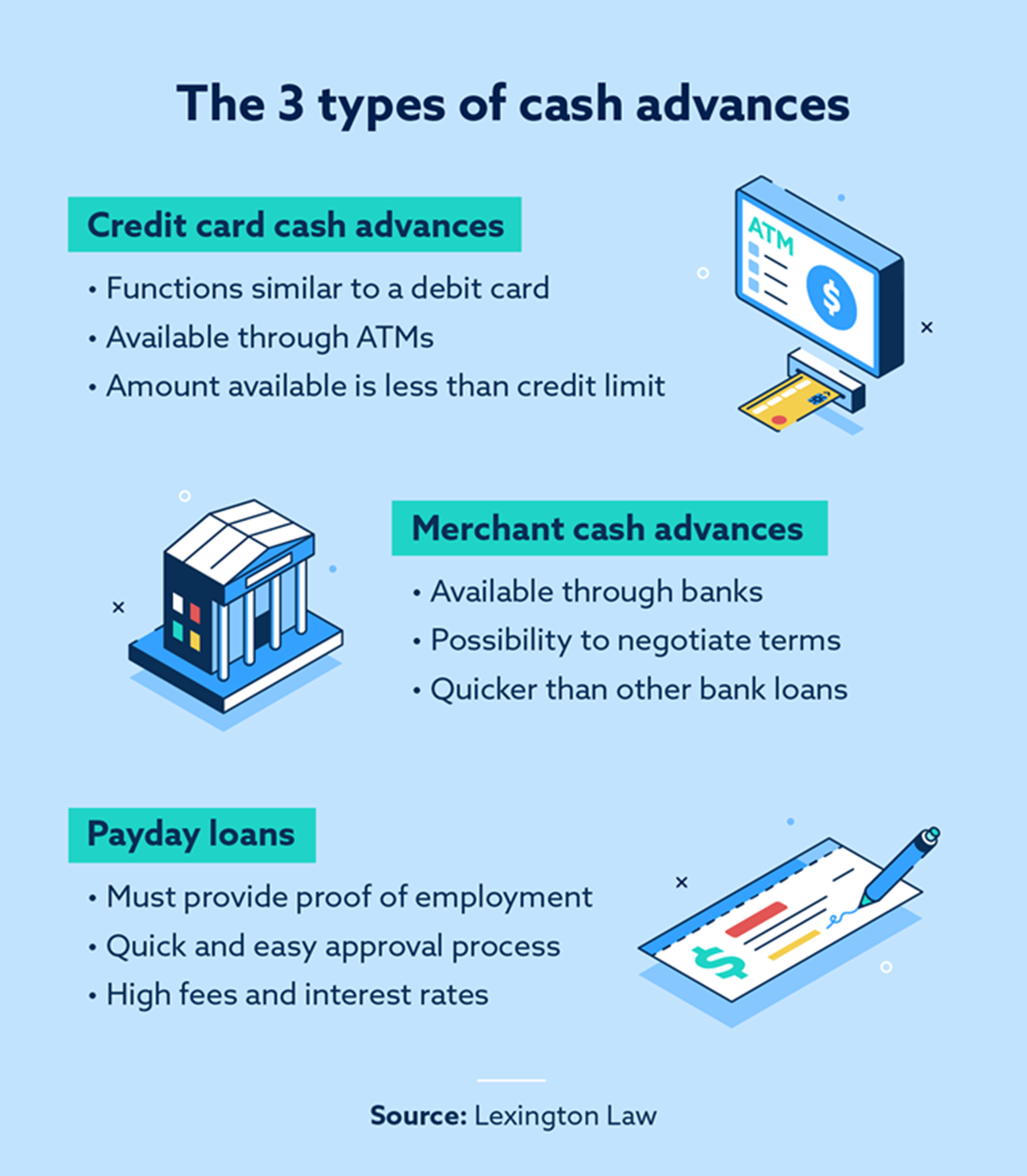

A cash advance is essentially a short-term loan provided by a credit card issuer, allowing the cardholder to withdraw physical cash through an ATM, a bank teller, or via “convenience checks.” In the world of tech development, where sudden hardware failures or urgent field-testing requirements can arise in remote locations, the temptation to access immediate cash is high. However, the fees associated with this service are distinct from standard purchase interest and can quickly accumulate, creating a “technical debt” of a financial nature.

The Financial Mechanics of Tech Innovation: Why Liquidity Matters

In the niche of Tech & Innovation, particularly within the UAV (Unmanned Aerial Vehicle) and remote sensing sectors, the lifecycle of a project often dictates the need for immediate, liquid capital. Whether it is securing a specialized LiDAR sensor from a vendor that does not accept traditional credit payments or covering emergency logistics for an autonomous flight trial in a foreign jurisdiction, cash remains a vital tool. However, the cost of accessing that cash through a credit card is governed by a complex set of rules that every tech professional must master.

Defining the Cash Advance Fee in a High-Growth Context

A cash advance fee is a service charge imposed by the credit card issuer for the act of providing liquid currency. Unlike a standard purchase—where you might buy a 4K gimbal camera and have a 21-to-25-day grace period to pay the balance before interest accrues—a cash advance typically begins accruing interest the moment the money is in your hand. There is no grace period.

The fee itself is usually calculated in one of two ways: a flat rate (e.g., $10 to $20 per transaction) or a percentage of the total amount withdrawn (typically 3% to 5%). For a drone mapping startup requiring $5,000 for emergency onsite repairs and data processing hardware, a 5% fee represents an immediate $250 loss before a single cent of interest is calculated. In the context of lean innovation, where every dollar is allocated toward R&D or AI optimization, these “hidden” costs can derail a monthly budget.

Why Drone and AI Startups Often Fall into the Cash Advance Trap

Innovation is rarely a linear process. For companies working on AI follow modes or obstacle avoidance sensors, the “testing phase” is fraught with unexpected costs. Consider a scenario where a team is conducting remote sensing in a high-altitude environment. If a critical propulsion component fails and the only local supplier requires cash or wire transfer, the project lead might resort to a credit card cash advance to keep the mission on track.

The urgency of “Tech & Innovation” often justifies the high cost of capital in the mind of the innovator. When an autonomous flight window is limited by weather or regulatory permits, the priority shifts from “cost-saving” to “mission success.” However, failing to account for the secondary costs—the cash advance interest rate (APR)—can lead to a compounding financial burden.

The Innovation Penalty: How High-Interest Fees Stifle R&D

Beyond the initial transaction fee, the true cost of a cash advance is found in the interest rate. Most credit card issuers set the APR for cash advances significantly higher than the APR for standard purchases. It is not uncommon to see purchase rates at 15-18% while cash advance rates soar to 25-29%. For a tech firm operating on venture capital or tight grants, this discrepancy represents a direct drain on the resources available for actual innovation.

Impact on Prototyping and Hardware Procurement

In the development of sophisticated hardware, such as drones equipped with thermal imaging or optical zoom capabilities, prototyping requires frequent, small-scale purchases. Often, these are done through traditional supply chains. However, when dealing with niche innovators, custom workshops, or international “maker spaces,” the need for cash or debit-based transactions increases.

If a company uses cash advances to fund these iterations, they are effectively paying a premium for their own R&D. This “innovation penalty” means that for every ten prototypes funded via cash advance, the cost of the eleventh is consumed entirely by fees and interest. In the competitive field of AI and autonomous systems, where being first to market is everything, this loss of capital efficiency can be the difference between scaling a product and stalling in the lab.

Calculating the Long-Term Cost of Immediate Capital

To truly understand the impact of a cash advance fee in the tech sector, one must look at the math over a fiscal quarter.

- Transaction Amount: $2,000 (for urgent sensor calibration equipment).

- Cash Advance Fee (5%): $100.

- Interest Rate (29.99% APR): Accruing daily.

- Total Cost after 30 Days: Approximately $2,150.

In this example, the developer has spent $150—roughly 7.5% of the total amount—just to access their own credit line for 30 days. In a field like mapping or remote sensing, where profit margins on early-stage contracts can be thin, these fees eat directly into the technical budget, potentially forcing compromises on the quality of sensors or the depth of the AI training data.

Technological Solutions to Financial Bottlenecks

As we move further into the era of autonomous flight and AI-driven logistics, the financial systems supporting these technologies are also evolving. The “Tech & Innovation” sector is beginning to develop its own solutions to the problem of high-cost liquidity, moving away from traditional credit card cash advances and toward more integrated, tech-forward financial tools.

Digital Wallets and Integrated Payment Systems in the UAV Market

The rise of FinTech has introduced new ways for drone operators and tech developers to manage field expenses without resorting to expensive cash advances. Integrated payment platforms now allow for instant peer-to-peer transfers and digital “burner” cards that can be loaded with specific amounts for field teams. This innovation reduces the reliance on physical cash, thereby bypassing the cash advance fee entirely.

Furthermore, some specialized drone insurance and service providers are integrating “smart contracts” into their operations. These systems can automatically trigger payments based on telemetry data or mission completion, ensuring that funds are available when and where they are needed, reducing the likelihood of a “cash-strapped” emergency during a critical remote sensing mission.

Moving Beyond Credit: Sustainable Funding for Remote Sensing Projects

For established firms in the mapping and AI sectors, the move toward “innovation-specific” credit lines is a major trend. These financial products are designed with the understanding of hardware lifecycles and the specific needs of tech R&D. Unlike a standard consumer credit card, these business lines of credit often offer lower interest rates for cash-like withdrawals and eliminate the predatory structure of the standard cash advance fee.

By leveraging these sophisticated financial tools, innovators can ensure that their capital is focused on enhancing AI follow modes, improving obstacle avoidance algorithms, and pushing the boundaries of what autonomous flight can achieve, rather than servicing high-interest debt.

Strategies for Managing Tech Operations Without High-Cost Debt

To maintain a competitive edge in Tech & Innovation, leaders must implement rigorous financial protocols that treat credit card cash advances as a last resort. The following strategies are becoming standard practice among successful UAV and AI firms:

- Establishing Emergency “Field Funds”: Instead of relying on individual credit cards, companies are setting up dedicated, low-interest liquidity accounts specifically for field testing and remote sensing deployments.

- Vendor Diversification: By working with suppliers who accept a wider range of digital and credit payments, tech firms can avoid the need for cash in the procurement of sensors, propellers, and specialized cases.

- Real-Time Expense Tracking: Utilizing AI-driven accounting software that flags high-interest transactions allows tech managers to see the immediate impact of a cash advance on their project’s ROI.

The world of drones, AI, and remote sensing is built on the premise of efficiency—doing more with less through the power of intelligent design. Applying that same philosophy to financial management means recognizing that a “cash advance fee” is not just a line item on a bank statement; it is a hurdle to innovation. By understanding these fees and seeking out more advanced financial technologies, the creators of tomorrow’s autonomous systems can ensure that their resources are always flying high, rather than being grounded by the weight of unnecessary debt.