New Jersey, a state renowned for its strategic location, diverse economy, and as a hub for innovation, implements a state sales tax that plays a crucial role in funding public services and infrastructure. For businesses, consumers, and especially the burgeoning technology and innovation sectors, understanding the nuances of the New Jersey state sales tax is not merely a matter of compliance; it is fundamental to financial planning, operational strategy, and competitive positioning. In an era where digital transformation is accelerating and new business models emerge daily, the application of traditional sales tax principles to modern technological offerings presents unique challenges and considerations.

This article delves into the specifics of New Jersey’s state sales tax, examining its foundational structure, current rates, and, critically, its intricate relationship with the state’s dynamic tech and innovation landscape. From software-as-a-service (SaaS) and digital products to cutting-edge research and development, we explore how New Jersey’s tax policies intersect with technological advancements, offering insights for businesses navigating this complex regulatory environment.

Understanding New Jersey’s Sales Tax Framework in a Digital Age

The New Jersey Sales and Use Tax Act imposes a tax on the retail sale of tangible personal property and certain services. While the basic premise seems straightforward, the digital economy introduces layers of complexity, requiring businesses to meticulously assess the taxability of their innovative products and services.

The Basics: What is Taxable and What is Not?

At its core, New Jersey sales tax applies to the sale of most tangible personal property, which includes physical goods like electronics, machinery, and consumer products. Beyond tangible goods, the tax also extends to specific enumerated services. These typically include charges for installation, maintenance, repair services of tangible personal property, and certain other services like information services, storage services, and telecommunications services.

However, the proliferation of digital products and services complicates this traditional definition. Is a software download tangible personal property? What about a cloud-based subscription service? New Jersey’s Division of Taxation has often grappled with these questions, issuing guidance that attempts to clarify the tax treatment of these modern offerings. Generally, software that is delivered electronically (i.e., not on a physical medium) may be considered a non-taxable service unless it falls under specific definitions of taxable information services or is integral to the sale of taxable tangible personal property. This distinction is paramount for tech companies offering SaaS, platform-as-a-service (PaaS), or infrastructure-as-a-service (IaaS) solutions.

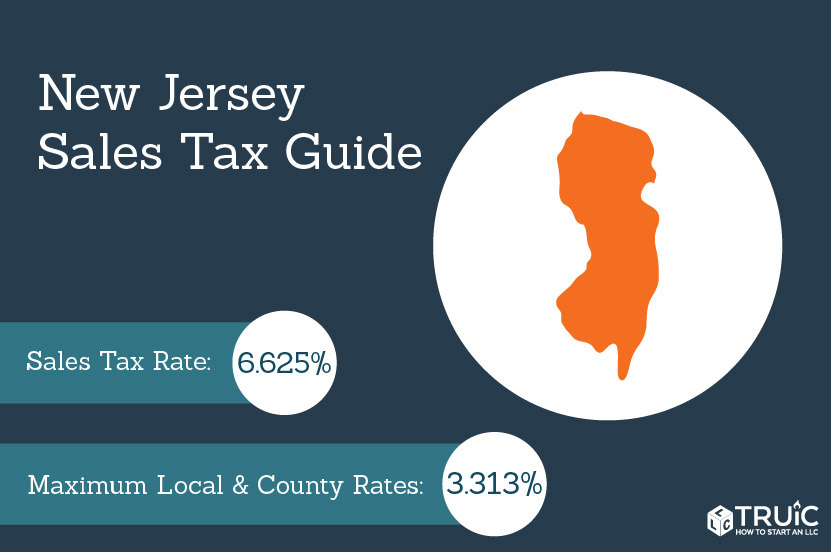

The Current Rate and Key Exemptions

As of the most recent updates, New Jersey’s state sales tax rate stands at 6.625%. This uniform rate applies across the state, with no local sales taxes adding to the complexity, unlike many other states. While this simplifies calculation, the array of exemptions further refines the scope of taxability.

Crucially for the tech and innovation sectors, certain exemptions can significantly impact operational costs and strategic decisions. For instance, the sale of certain equipment used directly and exclusively in research and development (R&D) activities may be exempt. This R&D exemption is a vital incentive for companies pushing the boundaries of technology, encouraging innovation within the state by reducing the cost burden on experimental and developmental stages. Additionally, sales for resale are exempt, which is important for tech distributors or integrators. Understanding these specific exemptions requires careful analysis of the business’s activities and the precise nature of the goods or services being bought or sold. This careful navigation of exemptions can provide a competitive edge and foster further investment in New Jersey’s tech ecosystem.

Sales Tax Implications for Tech Companies and Innovation in NJ

The rapid evolution of technology has profoundly reshaped traditional commerce, leading to a continuous reevaluation of sales tax laws to encompass digital transactions. For New Jersey’s tech companies, adapting to these evolving regulations is critical for sustainable growth.

Software and Digital Products: A Complex Landscape

The taxability of software and digital products in New Jersey is arguably one of the most challenging areas for tech companies. As noted, electronically delivered software is generally not considered tangible personal property and thus may not be subject to sales tax, unless it is classified as a taxable information service or is part of a transaction involving taxable tangible property. This creates a nuanced environment for various software offerings:

- SaaS (Software-as-a-Service): Often delivered remotely via the internet without a physical download, many SaaS offerings are treated as non-taxable services in New Jersey. However, if a SaaS offering predominantly provides access to databases, information reports, or specific data, it might fall under the definition of a taxable “information service.”

- Digital Downloads: E-books, music, movies, and other digital content downloaded by consumers generally remain non-taxable unless they constitute an information service.

- Cloud Computing: Services like IaaS and PaaS, which provide computing resources and platforms over the internet, typically follow the same logic as SaaS – generally non-taxable unless they fit the “information service” criteria.

- Custom Software Development: Charges for custom-designed and developed software services are generally exempt from sales tax, as they are considered professional services rather than the sale of a pre-existing tangible product.

The specific terms of service, the nature of what is being provided (access vs. data vs. tangible output), and how it’s delivered are all crucial in determining taxability.

Research & Development and Manufacturing Exemptions

New Jersey offers targeted exemptions designed to foster innovation and bolster its manufacturing sector, which often intertwines with high-tech operations.

- R&D Exemptions: Equipment, apparatus, and supplies used directly and exclusively in research and development are generally exempt from sales tax. This exemption is pivotal for biotech firms, pharmaceutical companies, advanced materials manufacturers, and any entity heavily invested in developing new technologies or improving existing ones. The “direct and exclusive” criteria require careful documentation and understanding of the scope of R&D activities.

- Manufacturing Exemptions: Purchases of machinery, apparatus, and equipment used directly and primarily in the production of tangible personal property for sale, as well as certain raw materials and components that become part of the finished product, are also exempt. For tech companies involved in producing hardware, robotics, or other tangible innovative products, these exemptions significantly reduce the cost of capital investment and operational expenses.

These exemptions underscore New Jersey’s commitment to supporting the growth of its innovation economy, providing tangible benefits that can influence business location and expansion decisions.

E-commerce and Remote Sellers: Nexus in the Digital Economy

The advent of e-commerce revolutionized retail, and with it, the landscape of sales tax. The landmark South Dakota v. Wayfair, Inc. Supreme Court decision in 2018 drastically altered the concept of “nexus,” allowing states to require out-of-state sellers without a physical presence to collect and remit sales tax if they meet certain economic thresholds.

New Jersey swiftly adopted economic nexus provisions. As of November 1, 2018, out-of-state sellers of tangible personal property or taxable services must collect and remit New Jersey sales tax if, in the current or preceding calendar year, their gross revenue from sales of tangible personal property or services delivered into New Jersey exceeded $100,000, or if they made 200 or more separate transactions for delivery into New Jersey.

This impacts tech companies significantly:

- Online Retailers: Any tech company selling hardware, software on physical media, or other taxable items online to New Jersey customers must monitor their sales volume and transaction count.

- Marketplace Facilitators: Platforms like app stores or e-commerce marketplaces are often responsible for collecting and remitting sales tax on behalf of third-party sellers using their platform, further complicating compliance for individual tech entrepreneurs.

- Digital Product Sellers: While many digital products might be non-taxable, companies selling mixed baskets of goods (e.g., physical tech gadgets alongside digital subscriptions) must diligently track and apply the rules.

Navigating Sales Tax for Innovative Services and Emerging Technologies

The pace of technological change often outstrips the legislative process, leaving a gap in clear tax guidance for novel services and emerging technologies. Businesses in these frontier areas face unique challenges.

AI, IoT, and Custom Software Development

Emerging technologies like Artificial Intelligence (AI), the Internet of Things (IoT), and highly customized software solutions often blur the lines between product and service.

- AI and IoT Solutions: Many AI and IoT applications manifest as data processing services, analytics platforms, or managed services rather than the sale of a tangible product. If these services primarily provide analysis or manipulation of data without directly selling access to vast databases of general information, they may often be classified as non-taxable professional services. However, if an IoT device itself is sold, the device would be taxable tangible personal property. The service component would then need to be carefully distinguished.

- Custom Software Development: As previously mentioned, services for designing, writing, installing, or modifying custom software generally remain exempt as professional services. This distinction is crucial for many tech startups and consultancies in New Jersey specializing in bespoke digital solutions for clients.

The key lies in clearly defining the “essence of the transaction”—is it the transfer of a physical good or specific pre-existing data, or the provision of expertise, labor, and a custom solution?

The Gig Economy and Digital Platforms

The rise of the gig economy and digital platforms has introduced new complexities. Sales tax generally applies to the final sale to the consumer, but who is the “seller” in a platform-mediated transaction?

- Marketplace Facilitators: New Jersey’s laws largely place the burden of sales tax collection on marketplace facilitators, which are platforms that enable sales by third-party sellers. This means that if a tech company operates a platform where independent contractors offer services or sell products, the platform itself might be responsible for sales tax, depending on the nature of the transaction.

- Services Rendered: If the gig economy services facilitated are inherently non-taxable services (e.g., custom coding, graphic design advice), then sales tax would generally not apply to the service itself. However, if the platform facilitates the rental of taxable tangible property (e.g., equipment) or the sale of taxable products, then sales tax would be applicable.

Understanding the role of the platform versus the individual seller is paramount for compliance in this rapidly evolving segment of the tech economy.

Compliance Strategies and Future Outlook for Tech Businesses

Effective sales tax compliance for tech companies in New Jersey is not a static task; it requires vigilance, adaptability, and strategic planning, especially given the dynamic nature of both technology and tax legislation.

Best Practices for Tech Startups and Established Firms

To ensure compliance and mitigate risks, tech businesses should adopt several best practices:

- Accurate Categorization: Meticulously classify every product and service offered. Is it tangible personal property, an information service, a custom service, or an exempt R&D activity? Document these classifications thoroughly.

- Nexus Review: Regularly assess nexus obligations, particularly for remote sellers. The $100,000 revenue or 200-transaction threshold can be met quickly in a digital-first economy.

- Stay Informed: Tax laws, especially those pertaining to digital goods and services, are frequently updated. Subscribing to regulatory alerts from the New Jersey Division of Taxation and consulting with tax professionals is essential.

- Clear Documentation: Maintain detailed records of all sales, exemptions claimed, and tax collected and remitted. In the event of an audit, robust documentation is invaluable.

- Customer Location Tracking: Ensure systems accurately capture the customer’s shipping address or billing address to correctly apply the New Jersey sales tax rate.

Leveraging Technology for Tax Compliance

Ironically, technology itself offers powerful solutions for navigating sales tax complexities.

- Sales Tax Automation Software: Specialized software can automate nexus detection, tax rate calculation, exemption management, and even filing processes across multiple jurisdictions. These tools are particularly beneficial for e-commerce tech companies with a broad customer base.

- ERP/Accounting System Integrations: Integrating sales tax solutions directly into Enterprise Resource Planning (ERP) or accounting systems streamlines operations, reduces manual errors, and provides real-time visibility into tax obligations.

- Data Analytics: Utilizing data analytics can help companies identify patterns in sales data, predict nexus triggers, and optimize their tax strategy.

By leveraging these technological tools, tech companies can transform sales tax compliance from a burdensome chore into an efficient, data-driven process.

The Future of Sales Tax in a Technologically Advanced New Jersey

The interplay between sales tax and technology in New Jersey is a continually evolving narrative. As AI becomes more sophisticated, virtual and augmented reality gain traction, and blockchain technology reshapes transactions, tax authorities will continue to adapt their frameworks. New Jersey’s commitment to fostering a vibrant innovation economy suggests a proactive approach to these changes, potentially offering new incentives or clarifications that benefit tech businesses. However, the fiscal needs of the state will also drive efforts to ensure that new economic activities contribute their fair share.

For tech companies, the future demands agility. Engagement with industry associations, participation in policy discussions, and maintaining open lines of communication with tax advisors will be crucial. By staying ahead of the curve, New Jersey’s tech innovators can continue to thrive, contributing to the state’s economy while navigating the ever-present landscape of state sales tax.