The burgeoning drone industry, a nexus of cutting-edge technology and innovative application, presents a unique landscape for businesses and hobbyists alike. As the skies become increasingly populated with unmanned aerial vehicles (UAVs) for everything from recreational flying to advanced aerial mapping and delivery services, the economic activities surrounding these devices naturally fall under the purview of state and local taxation. Understanding the intricacies of sales tax in Illinois is not just a regulatory hurdle but a crucial component of financial planning and compliance for anyone involved in the drone ecosystem.

This comprehensive guide will demystify what Illinois (IL) sales tax entails, specifically through the lens of drone-related transactions. From the initial purchase of a quadcopter to the provision of sophisticated aerial services, we will explore the fundamental principles, varying rates, taxable items, and essential compliance considerations that impact the drone community in the Prairie State.

Understanding Illinois Sales Tax Fundamentals for Drone Enthusiasts and Businesses

Illinois sales tax is a transactional tax imposed on the retail sale of tangible personal property and certain services. For the drone industry, this means that most purchases and, in some cases, the provision of services related to drones, are subject to this tax. The system is multifaceted, incorporating both state-level rates and additional local taxes that can vary significantly depending on the specific location of the sale or service.

At its core, sales tax is collected by the seller at the point of sale and subsequently remitted to the Illinois Department of Revenue (IDOR). This mechanism ensures that the state and local municipalities receive revenue to fund public services. For a sector as dynamic as drones, characterized by rapid technological advancements and evolving business models, a clear understanding of these fundamentals is paramount to avoiding costly compliance errors and ensuring sustainable operation.

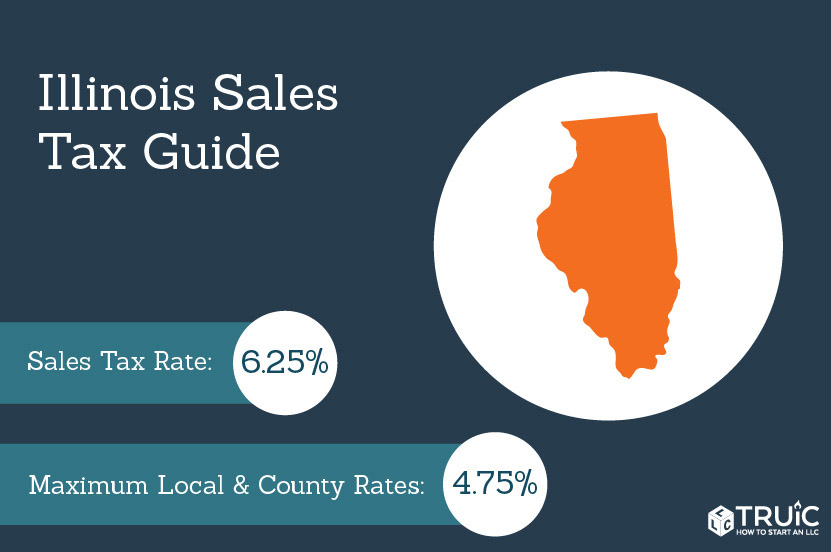

The State Sales Tax Rate and Its Local Variations

The state of Illinois imposes a baseline sales tax rate that applies uniformly across the state. However, this is just the starting point. Local jurisdictions – including counties, municipalities, and various special taxing districts – have the authority to levy their own sales taxes, which are then added to the state rate. This layered approach means that the effective sales tax rate can differ dramatically from one town or county to another.

For individuals purchasing a new racing drone or a commercial entity acquiring a fleet of sophisticated UAVs, the final sales tax amount will depend heavily on the location of the retailer. Similarly, a drone service provider operating in multiple locations within Illinois must be diligent in applying the correct composite rate for each transaction based on the point of sale or service delivery. This complexity necessitates robust sales tax management systems, especially for businesses with a statewide presence or e-commerce operations that ship drones and accessories across different Illinois locales. The difference between a state rate and a combined local rate can significantly impact the overall cost of drone investments or the profitability of drone-related services.

Taxable Drone Products and Services

The primary focus of Illinois sales tax lies on the retail sale of “tangible personal property.” In the context of drones, this broadly includes:

- Drones themselves: Quadcopters, UAVs, FPV drones, micro drones, racing drones, agricultural drones, industrial inspection drones, and any other type of unmanned aircraft.

- Drone accessories: Batteries, propellers, remote controllers, carrying cases, landing pads, FPV goggles, charging stations, spare parts, and upgrade kits.

- Drone components: Gimbal cameras, thermal cameras, optical zoom lenses, specialized sensors, GPS modules, flight controllers, and other integral parts sold separately.

- Software sold with drones or as tangible media: While many drone apps are digital, physical software media or software bundled with a drone purchase is generally taxable.

Beyond physical goods, certain services are also subject to IL sales tax. This can be particularly relevant for commercial drone operators. While Illinois generally does not tax services, specific enumerated services are taxable. For drone businesses, this might include:

- Repair and maintenance services: If a drone repair service involves the installation of new taxable parts, the entire charge (labor and parts) may be subject to sales tax.

- Photography and videography services: While the service itself (flying the drone and capturing footage) might not be directly taxed, if the service involves the transfer of tangible personal property (e.g., a physical hard drive with footage, printed photos), or if it’s considered part of a larger taxable transaction, it could trigger sales tax implications.

- Drone rentals: Short-term rentals of drones or related equipment are typically subject to sales tax.

Understanding the distinction between taxable and non-taxable services is crucial for drone service providers to accurately calculate and collect sales tax, ensuring compliance and transparent pricing for their clients.

Key Compliance Considerations for Drone Businesses in Illinois

For businesses engaged in selling, repairing, or providing services with drones in Illinois, effective sales tax compliance extends beyond merely knowing the rates. It involves a systematic approach to registration, collection, reporting, and remittance. The IDOR scrutinizes these activities closely, and non-compliance can lead to significant penalties, interest, and even legal repercussions. As the drone industry continues its exponential growth, staying abreast of evolving regulations and establishing robust internal processes are non-negotiable for operational integrity.

Sales Tax Registration and Collection Requirements

Before engaging in any taxable sales or services within Illinois, drone businesses must first register with the Illinois Department of Revenue. This involves obtaining a Certificate of Registration (also known as a sales tax permit or reseller’s permit). Operating without proper registration is a serious offense that can lead to severe penalties. The registration process typically requires businesses to provide basic information about their operations, legal structure, and anticipated sales volume.

Once registered, businesses are legally obligated to collect sales tax from their customers on all taxable transactions. This collection must be transparent, with the sales tax clearly itemized on invoices or receipts. The funds collected are not considered business income but rather trust funds held on behalf of the state. Therefore, accurate record-keeping of all sales tax collected is paramount.

For out-of-state drone sellers, the concept of “economic nexus” is particularly relevant. Illinois, like many states, has adopted economic nexus laws that require remote sellers to collect and remit sales tax if their sales into the state exceed a certain threshold (e.g., $100,000 in gross receipts or 200 separate transactions in the preceding 12 months). This means that an online retailer selling drones from California to customers in Illinois, even without a physical presence, might still be required to register and collect IL sales tax. This significantly broadens the scope of compliance for many drone e-commerce businesses.

Use Tax: When Sales Tax Isn’t Collected

Illinois Use Tax is a complement to sales tax, designed to level the playing field and prevent consumers from avoiding sales tax by purchasing items from out-of-state retailers who do not collect IL sales tax. If an Illinois resident or business purchases a drone, drone components, or related services from an out-of-state vendor who does not collect Illinois sales tax, the buyer is responsible for remitting use tax directly to the IDOR.

This is highly relevant for drone hobbyists and businesses that frequently purchase equipment online from non-Illinois-registered sellers. For example, if a drone racing enthusiast buys a specialized FPV camera from an online store based in Oregon (which has no sales tax), and that store does not collect Illinois sales tax, the Illinois buyer is legally obligated to self-assess and pay the Illinois use tax. Businesses generally track and remit use tax as part of their regular tax filings, while individuals can report it on their annual income tax returns. Failing to account for use tax can result in audits and penalties.

Exemptions and Specialized Considerations for Drone Operations

While a wide array of drone-related transactions are subject to sales tax, Illinois tax law does provide for specific exemptions that can benefit certain businesses or types of purchases. Navigating these exemptions requires careful attention to detail and understanding of their specific criteria. Additionally, certain operational aspects within the drone industry might warrant specialized tax treatment.

Common Exemptions Applicable to Drones

Several exemptions may apply to drone transactions, though their applicability often depends on the buyer’s status and the intended use of the drone or service:

- Resale Exemption: A fundamental exemption allows businesses to purchase drones, parts, or accessories without paying sales tax if they intend to resell those items to their customers. For example, a drone repair shop purchasing spare propellers to install on a customer’s drone would use a resale certificate to avoid paying sales tax on the propellers. The sales tax is then collected from the end-consumer.

- Manufacturing Exemption: Businesses primarily engaged in manufacturing drones or drone components may qualify for an exemption on purchases of machinery, equipment, and raw materials used directly in the manufacturing process. This can significantly reduce the cost of production for Illinois-based drone manufacturers.

- Graphic Arts Exemption: If a drone is used primarily in the graphic arts (e.g., for aerial photography by a professional photographer where the output is directly used in graphic arts production), the drone itself and related equipment might be eligible for an exemption. This requires strict adherence to IDOR guidelines regarding the primary use of the equipment.

- Out-of-State Use: If a drone is purchased in Illinois but immediately and primarily used outside of Illinois, it may, under certain conditions, be exempt from Illinois sales tax.

Understanding and correctly applying these exemptions requires careful documentation and adherence to IDOR guidelines. Misclaiming an exemption can lead to back taxes, interest, and penalties.

Accounting for Drone Service Contracts and Bundled Sales

For commercial drone service providers, sales tax can become complex when dealing with service contracts or bundled sales. A service contract for recurring drone inspections, mapping, or security patrols often involves a mix of taxable tangible personal property (e.g., replacement parts, detailed reports on physical media) and non-taxable services (e.g., the labor of flying the drone and data acquisition).

When sales involve both taxable and non-taxable elements, businesses must properly allocate the charges. If the taxable tangible personal property is incidental to the non-taxable service, the entire transaction might be exempt. However, if the tangible personal property is a significant component, or if it is separately stated, then the taxable portion must be subjected to sales tax. For example, a contract that includes drone flight services and the provision of a specialized, custom-built drone that remains the client’s property after the service would likely require careful sales tax allocation.

Bundled sales, where a drone, accessories, and perhaps a service plan are sold together for a single price, also require attention. Illinois law often dictates how to allocate the sales price among the various components to determine the correct sales tax liability. This complexity underscores the importance of consulting with tax professionals or utilizing robust accounting software tailored to handle mixed transactions within the drone industry.

Conclusion: Staying Ahead in Illinois Drone Taxation

The landscape of Illinois sales tax for the drone industry is a dynamic one, reflecting the rapid evolution of technology and commerce. From the hobbyist purchasing their first FPV drone to the enterprise operating a sophisticated fleet for commercial applications, understanding and complying with IL sales tax regulations is a critical aspect of participation in this exciting sector.

Navigating the state and local sales tax rates, identifying taxable drone products and services, diligently managing registration and collection, and accurately applying exemptions are all vital components of financial health and regulatory adherence. The nuances of use tax for out-of-state purchases and the complexities of bundled sales or service contracts further highlight the need for precision.

By proactively addressing these tax considerations, drone businesses and enthusiasts in Illinois can ensure compliance, avoid costly pitfalls, and contribute to the sustainable growth of an industry that continues to reshape how we interact with the world from above. Staying informed, maintaining meticulous records, and seeking expert advice when needed will be key to successfully navigating the intricacies of Illinois sales tax in the drone era.