If you’ve recently filed a home insurance claim for a damaged roof or property loss, you likely saw a confusing line item on your claim summary: Recoverable Depreciation.

Understanding this term is the difference between leaving thousands of dollars on the table and getting your home fully repaired. Here is everything you need to know about what it is, how it works, and how to claim it.

The Basic Definition

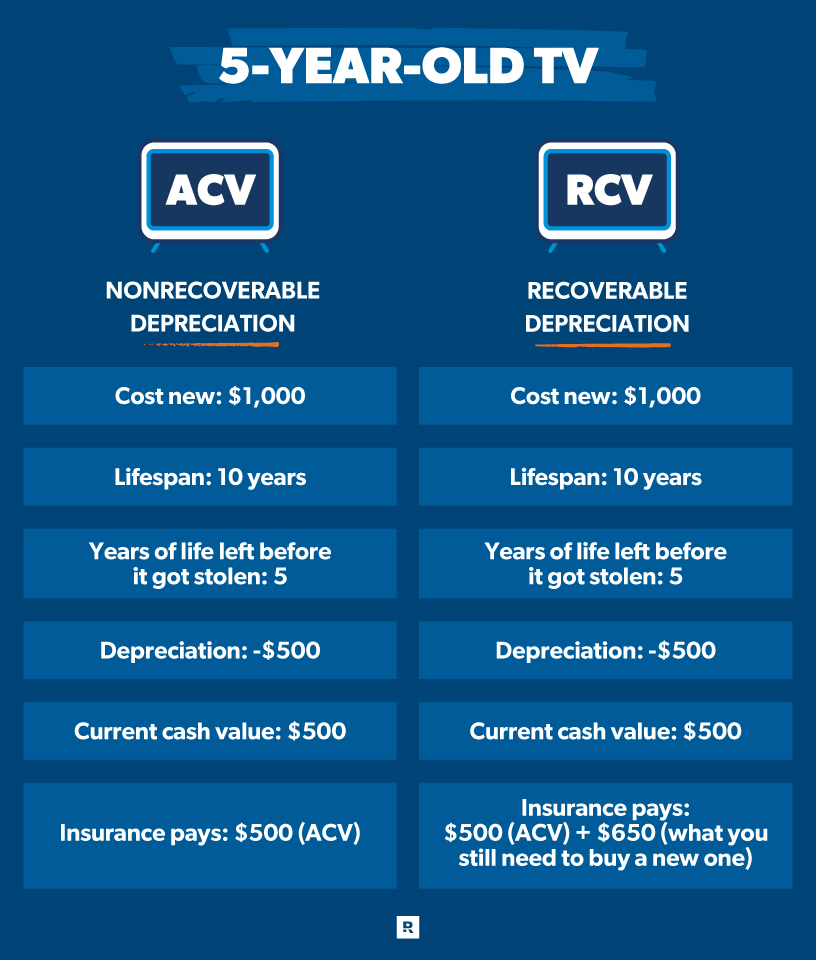

In the insurance world, recoverable depreciation is the difference between the Actual Cash Value (ACV) of an item and its Replacement Cost Value (RCV).

When you file a claim, insurance companies don’t usually give you the full amount to buy a brand-new version of your lost item right away. Instead, they “hold back” a portion of the money based on the item’s age and wear-and-tear. That “held-back” money is the recoverable depreciation.

The Three Key Terms You Must Know

To understand recoverable depreciation, you have to understand the math behind it:

- Replacement Cost Value (RCV): The total cost to buy a brand-new version of the item or repair the damage at today’s market prices.

- Actual Cash Value (ACV): The value of the item right now (RCV minus its age and condition). This is essentially the “garage sale” value.

- Recoverable Depreciation: The amount the insurance company subtracts from the RCV to account for the item’s age, which you can get back later.

The Formula:

ACV + Recoverable Depreciation = RCV

How the Process Works (Step-by-Step)

Most homeowners are surprised to learn they receive their insurance payout in two separate checks.

Step 1: The Initial Payment (ACV)

Once your claim is approved, the insurance company sends a check for the Actual Cash Value. They take the total cost of the repair, subtract your deductible, and subtract the depreciation.

- Example: Your 10-year-old roof costs $10,000 to replace. Because it’s old, they value it at $6,000. They send you a check for $6,000 (minus your deductible).

Step 2: The Repair Phase

You hire a contractor and have the work completed. You will likely have to pay the contractor using the first check plus your own out-of-pocket funds to cover the “depreciated” amount.

Step 3: Claiming the Depreciation

Once the work is finished, you submit the final invoice and photos to your insurance company. This proves that you actually spent the money to restore the property.

Step 4: The Second Payment

The insurance company then sends you a second check for the Recoverable Depreciation amount they withheld originally. This brings your total payout up to the full Replacement Cost Value.

Recoverable vs. Non-Recoverable Depreciation

Not all insurance policies are created equal.

- Recoverable: If you have an RCV Policy, you can get the depreciation back after repairs are done.

- Non-Recoverable: If you have an ACV Policy, you only get the value of the item in its used state. You cannot claim the depreciation, and you must pay the difference out of pocket to buy something new.

Important Deadlines

You cannot wait forever to claim your recoverable depreciation. Most policies have a strict time limit—often 180 days to one year from the date of the loss—to complete the repairs and request the remaining funds. If you miss this window, the depreciation becomes non-recoverable.

The Bottom Line

Recoverable depreciation is essentially a “reimbursement” system. It ensures that homeowners actually use the insurance money to repair their homes rather than pocketing the cash.

Pro Tip: Always keep every receipt, invoice, and contract related to your repair. Your insurance company will not release the depreciation check without proof that the work was completed and paid for.

Does this help?

If you have a specific article you want me to summarize or specific keywords you need included, please paste the content below!