When purchasing car insurance, particularly in states like Pennsylvania, you will encounter a crucial choice that significantly impacts your legal rights: Full Tort vs. Limited Tort.

While selecting an option might seem like a simple way to lower your monthly premium, the decision you make today could determine whether you can recover compensation for your pain and suffering after an accident tomorrow. Here is everything you need to know about what Full Tort means and why it matters.

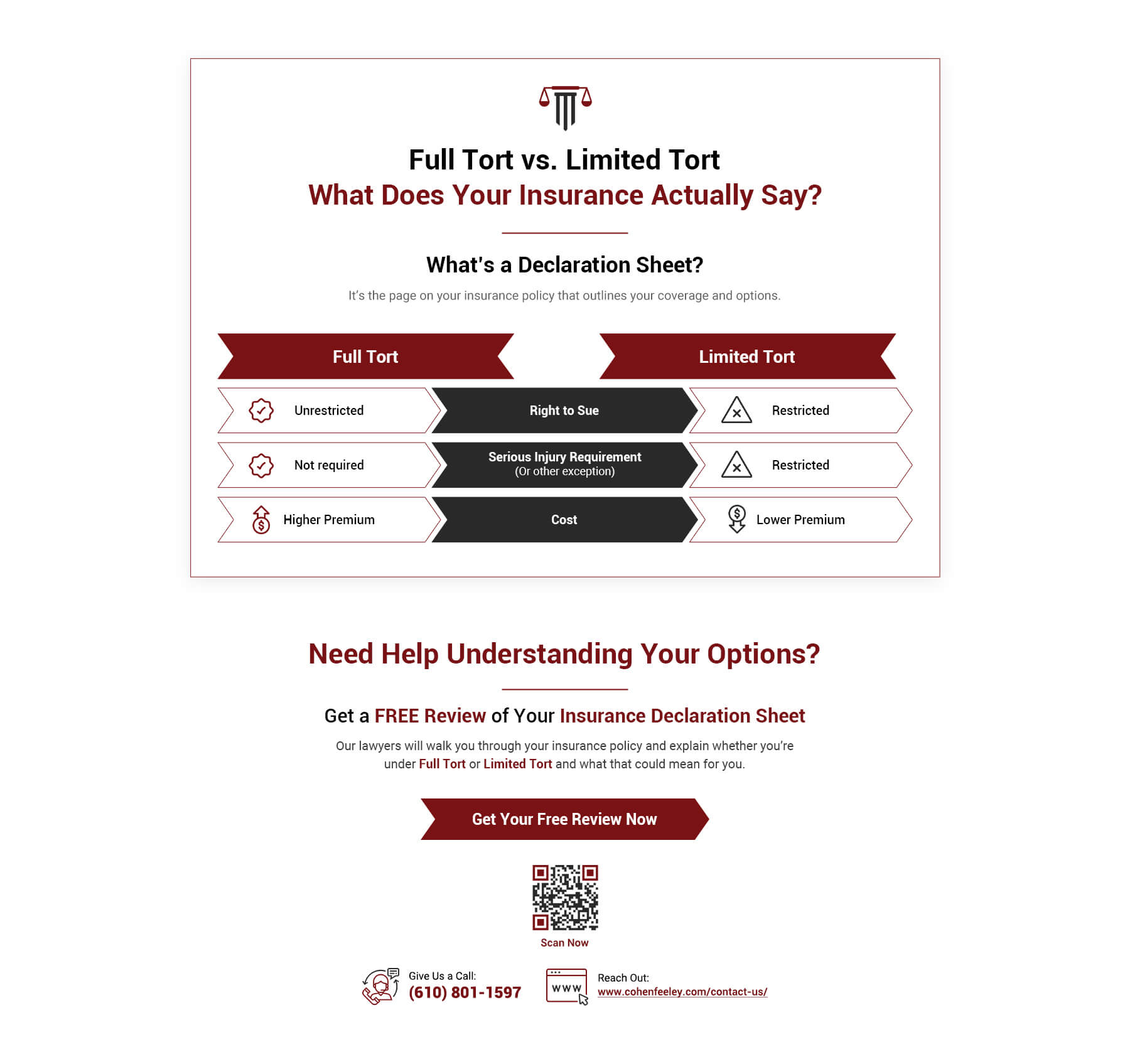

Defining Full Tort

Full Tort is an insurance terminology used in “choice no-fault” states. Selecting the Full Tort option on your motor vehicle insurance policy means that you maintain your unrestricted right to sue the at-fault driver for all damages resulting from a car accident.

Unlike “Limited Tort,” which restricts your ability to seek compensation for non-monetary losses, Full Tort allows you to seek recovery for both economic and non-economic damages, regardless of the severity of your injuries.

Full Tort vs. Limited Tort: What’s the Difference?

To understand Full Tort, you must understand what you give up if you choose Limited Tort.

1. Economic Damages (Covered by Both)

Both options allow you to recover “out-of-pocket” expenses. These include:

- Medical bills not covered by your own PIP (Personal Injury Protection).

- Lost wages.

- Property damage (repairing your car).

2. Non-Economic Damages (The Key Difference)

This is where Full Tort shines. Non-economic damages include:

- Pain and suffering.

- Emotional distress and trauma.

- Loss of enjoyment of life.

- Loss of consortium.

Under Limited Tort, you generally cannot sue for these damages unless your injuries meet a “serious injury” threshold (such as permanent impairment, significant disfigurement, or death). Under Full Tort, there is no threshold. Even if your injury is “minor” (like whiplash or soft tissue damage) but still causes significant pain, you have the right to seek compensation.

The Benefits of Choosing Full Tort

While Full Tort usually comes with a higher premium (typically 15% to 20% more than Limited Tort), the benefits are substantial:

- Total Legal Protection: You aren’t at the mercy of an insurance company’s definition of a “serious injury.” If someone hits you, you can hold them fully accountable for how the accident changed your life.

- Coverage for the Whole Family: In most cases, the tort option selected by the policyholder applies to everyone else covered under that policy, including children and spouses.

- Peace of Mind: You won’t have to worry about whether a chronic back injury or a persistent “minor” ache will be legally “important” enough to qualify for a settlement.

Is Full Tort Worth the Extra Cost?

Most legal experts and personal injury attorneys strongly recommend Full Tort.

The reason is simple: insurance companies often fight “Limited Tort” claims aggressively, arguing that the victim’s injuries aren’t “serious” enough to warrant a payout for pain and suffering. By paying a slightly higher premium now, you protect your future self from being left with thousands of dollars in “intangible” losses that a Limited Tort policy won’t cover.

Exceptions to Limited Tort

Even if you chose Limited Tort, you might be “upgraded” to Full Tort status in specific situations, such as:

- The at-fault driver was driving a vehicle registered in another state.

- The at-fault driver was convicted of DUI.

- The at-fault driver intended to injure themselves or others.

- You were a passenger in a commercial vehicle (like a taxi or bus) or a pedestrian.

Final Thoughts

“What does full tort mean?” It means unrestricted access to the civil justice system.

Choosing Full Tort is an investment in your legal rights. While the savings of Limited Tort may look attractive on a monthly statement, the true value of Full Tort becomes clear the moment you are involved in an accident that wasn’t your fault.

Disclaimer: Insurance laws vary by state. This article is for informational purposes and does not constitute legal advice. Always consult with a licensed insurance agent or a qualified attorney in your jurisdiction.